| https://www.next-finance.net/en | |

|

Opinion

|

Chinese GDP, a myth?

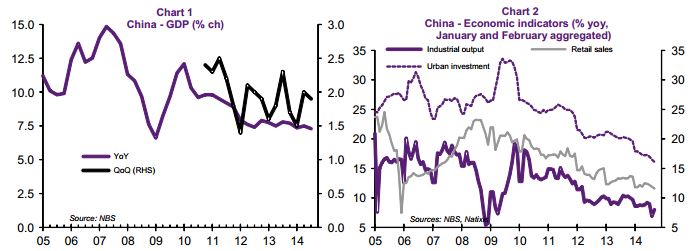

The slowdown of the Chinese economy, as reflected by GDP growth in Q3 2014, is not particularly serious. While there was a slight deceleration, GDP nonetheless increased by 7.3% year-on-year and by 1.9% quarter-on-quarter.

Article also available in :

English ![]() |

français

|

français ![]()

Compared with Q2 2014, when growth reached 7.5% year-on-year and 2.0% quarter-on-quarter (see Chart 1), the extent of the slowdown is far less serious than suggested by other economic indicators.

Although industrial output did accelerate slightly in September compared with August, the increase in Q3 2014 remains very slight by past standards, while urban investment has declined to an all-time low (see Chart 2 above).

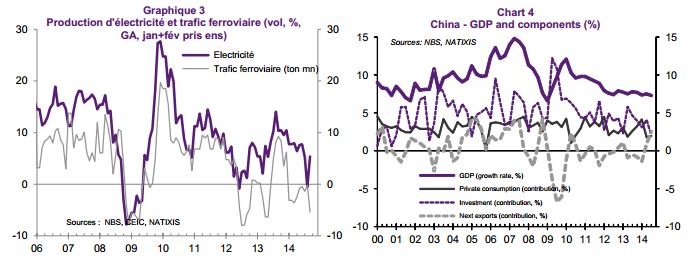

Similarly the consumption of energy such as electricity and rail traffic are increasing much more slowly than in the past (see chart 3). Retail sales are the one indicator to be putting up a fair resistance, with growth remaining stable in real terms.

This lag can in fact be explained by an analysis of the contribution made by the different demand components towards GDP growth. Domestic demand is indeed weak. Investment increased by only 3.8% year-on-year, when this component accounts for half of China’s GDP. Consumption (households and public administrations) is not decelerating, but growth for this component remains below 6% year-on-year. Considering GDP growth reached 7.3% over this period, domestic demand is visibly very weak. The explanation of this myth comes from the strong contribution by net exports, as exports increased by 13% and imports by only 6% (Natixis estimates). The 7.3% GDP growth therefore owed much to performances on the export front, whereas domestic demand (hence imports) was weak, as highlighted above (see Chart 4).

Given the weak domestic demand, Chinese growth remains exposed to some downside risk, this risk being more serious than is suggested by the slight slowdown in GDP growth. With the Chinese economy transitioning to a new growth model, former engines of growth such as investment are stalling, while the new engines of growth are still stuttering. The current air pocket therefore exposes the country to the risk of a slowdown, with the authorities keen to limit the extent of this dip. That is why the authorities are taking targeted measures to support the economy, at both monetary and fiscal levels.

The transition being a work-in-progress, the downside risk could be present for some time. We do not see there being an economic recovery in the short term and our estimates therefore remain for GDP growth of 7.3% in 2013 and 7% in 2015. As and when structural reforms are pushed through, China’s economic cycle will enter an upward leg characterised by more stable medium- to long-term growth. For more details see the special report.

This change in growth model from investment (industrial sector) to consumption (services sector) implies not only a secular slowdown in Chinese growth but also a lasting slowdown in Chinese demand for commodities, especially those used massively in the construction and heavy industrial sectors. Other import categories are less affected, especially those meeting the needs of Chinese household consumption. The breakdown of imports by region of origin supports this analysis: in nominal terms, imports from the US increased by 12.5%, those from Europe by 9.1%, whereas imports from Latin America increased by only 1.2% and imports from Africa in fact decreased by 0.5% year-on-year in September.

Next Finance , October 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |