| https://www.next-finance.net/en | |

|

Opinion

|

Brexit’s impact for equity investors

For someone living, moving to or doing business with the United Kingdom in the last year, the “Brexit Question” has been an important consideration. During the beginning of 2019 there have been several dates, votes and occasions when we expected to get a detailed picture of what Brexit will mean. Yet we were then left staring at each other, still wondering what the outcome might be.

Sometimes the most important questions are also the toughest to answer.

For someone living, moving to or doing business with the United Kingdom in the last year, the “Brexit Question” has been an important consideration. During the beginning of 2019 there have been several dates, votes and occasions when we expected to get a detailed picture of what Brexit will mean. Yet we were then left staring at each other, still wondering what the outcome might be.

While we might not be able to solve the question as to what Brexit will look like in this blog, we might be able to provide greater context for European equity investors.

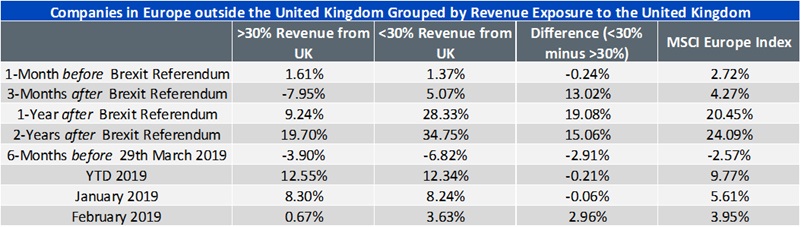

Question 1: Have European companies that aren’t in the United Kingdom seen their performance impacted thus far by the Brexit Process?

Our approach:

- Start with the MSCI Europe Investable Market Index (IMI) universe, excluding United Kingdom companies.

- Group companies into two groups with those that derive more than 30% of their revenue from the United Kingdom, and those that derive less than 30%.

- We compare the median returns of these groups, and note the return of the MSCI Europe Index, to give an idea of the market environment during these periods.

Our conclusions:

- Whether looking at 3-months, 1-year or 2-years after the Brexit referendum on 23 June 2016, there was a significant difference in median returns for companies based on the amount of revenue received from within the UK. Over each period, having less revenue from the UK led to higher median returns.

- More recently in 2019, there is less differentiation in the median returns for the groupings in Figure 1 based on revenues from within the UK.

While it’s logical to think that Brexit and the process that we have been undergoing does matter, it may not be the sole factor influencing the returns of these companies. We’d therefore caution investors against oversimplifying a complex issue based on a single table.

Figure 1: Sensitivity of European companies to revenues from the United Kingdom

- Sources: Factset, Bloomberg. Returns are measured in local currencies and are not impacted by changes in exchange rates. Companies for which Factset had no geographic revenue data were excluded from the analysis. Returns for the >30% and <30% groupings are measured as the median of the returns of the respective stocks so as to mitigate the impact of outliers. Periods are as follows: 23 May 2016 to 23 June 2016; 23 June 2016 to 23 September 2016; 23 June 2016 to 23 June 2017; 23 June 2016 to 23 June 2018; 29 September 2018 to 26 February 2019; 31 December 2018 to 26 February 2019; 31 December 2018 to 31 January 2019; 31 January 2019 to 26 February 2019. Historical performance is not an indication of future performance and any investments may go down in value.

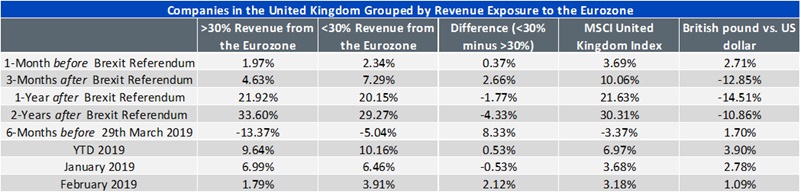

Question 2: Have companies in the United Kingdom that do more business with the Eurozone seen returns impacted during the Brexit process?

Our approach:

- Start with the MSCI United Kingdom Investable Market Index (IMI) universe.

- Group companies into two groups where there are those that derive more than 30% of their revenue from the Eurozone and those that derive less than 30%.

- We compare the median returns of these group and note the return of the MSCI United Kingdom Index, to give an idea of the market environment during these periods.

Our conclusions:

It’s important to consider the behaviour of the British pound during this period. For example, the companies that derived greater than 30% of their revenues from the Eurozone could be more globally oriented with respect to revenue distribution. This would indicate a potential to perform strongly during periods where the British pound is tending toward depreciation. Notably:

- 3 months after the Brexit referendum, the British pound dropped nearly 13%. Companies deriving less revenue from within the Eurozone outperformed those that derived more revenue from within the Eurozone.

- 1 and 2 years after the vote, the UK equity market generally performed well, and the companies deriving more revenues from the Eurozone performed better than those that derived less revenues from the Eurozone. This wouldn’t necessarily mean investors were ignoring potential Brexit concerns—we tend to think that the depreciation of the British pound in these periods would have been the bigger factor.

The differences between returns narrowed in the 2019 period shown. But the median returns in February indicate that companies with less revenues from the Eurozone outperformed.

Figure 2: Sensitivity of United Kingdom companies to revenues from the Eurozone

- Sources: Factset, Bloomberg. Returns are measured in local currencies and are not impacted by changes in exchange rates. Companies for which Factset had no geographic revenue data were excluded from the analysis. Returns for the >30% and <30% groupings are measured as the median of the returns of the respective stocks so as to mitigate the impact of outliers. Periods are as follows: 23 May 2016 to 23 June 2016; 23 June 2016 to 23 September 2016; 23 June 2016 to 23 June 2017; 23 June 2016 to 23 June 2018; 29 September 2018 to 26 February 2019; 31 December 2018 to 26 February 2019; 31 December 2018 to 31 January 2019; 31 January 2019 to 26 February 2019. Historical performance is not an indication of future performance and any investments may go down in value.

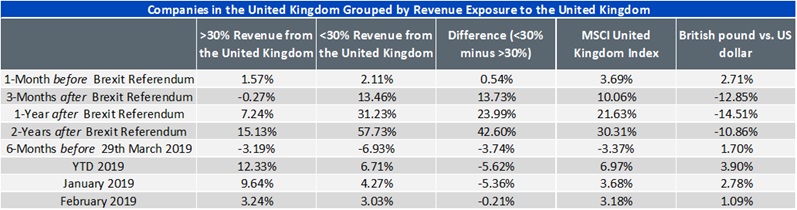

Question 3: How different were the returns of those companies that derived more revenue from within the United Kingdom versus those that derived less revenues from within the United Kingdom? If the United Kingdom economy is perceived to be at risk of slowing down due to the Brexit process, companies that are more domestic in their revenue distributions could be at greater risk.

Our approach:

- Start with the MSCI United Kingdom IMI Index universe.

- Group companies into two groups where there are those that derive more than 30% of their revenue from the United Kingdom, and those that derive less than 30%.

- We compare the median returns of these groups and note the return of the MSCI United Kingdom Index, to give an idea of the market environment during these periods.

Our conclusions:

- It’s important to consider the behaviour of the British pound during this period. For example, companies that derived less than 30% of their revenues from the United Kingdom would be more globally oriented with respect to their revenue distribution. This would indicate a potential to perform more strongly during periods where the British pound is tending toward depreciation. The results in Figure 3 show 3 significant periods of British pound depreciation after the Brexit referendum. The median returns of the stocks with less than 30% of revenues from the United Kingdom outperformed in each of these periods.

- During the periods of British pound strength in Figure 3 after the Brexit referendum, the most domestically oriented companies in the United Kingdom saw median returns outperform.

Figure 3: Sensitivity of United Kingdom companies to revenues from the United Kingdom

- Sources: Factset, Bloomberg. Returns are measured in local currencies and are not impacted by changes in exchange rates. Companies for which Factset had no geographic revenue data were excluded from the analysis. Returns for the >30% and <30% groupings are measured as the median of the returns of the respective stocks so as to mitigate the impact of outliers. Periods are as follows: 23 May 2016 to 23 June 2016; 23 June 2016 to 23 September 2016; 23 June 2016 to 23 June 2017; 23 June 2016 to 23 June 2018; 29 September 2018 to 26 February 2019; 31 December 2018 to 26 February 2019; 31 December 2018 to 31 January 2019; 31 January 2019 to 26 February 2019. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

While we think these summary statistics are interesting and worth thinking about, they don’t represent the full story on the Brexit impact.

As of this writing, we still don’t know exactly what Brexit will mean. And underlying companies have different cost structures and exposures, which might impact the picture differently once the Brexit situation contains greater and more certain details.

Geographic revenue is an important measure, but we’d indicate that it isn’t the sole measure to consider.

Christopher Gannatti , March 2019

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |