| https://www.next-finance.net/en | |

|

Opinion

|

Bond Pain trade for global macro

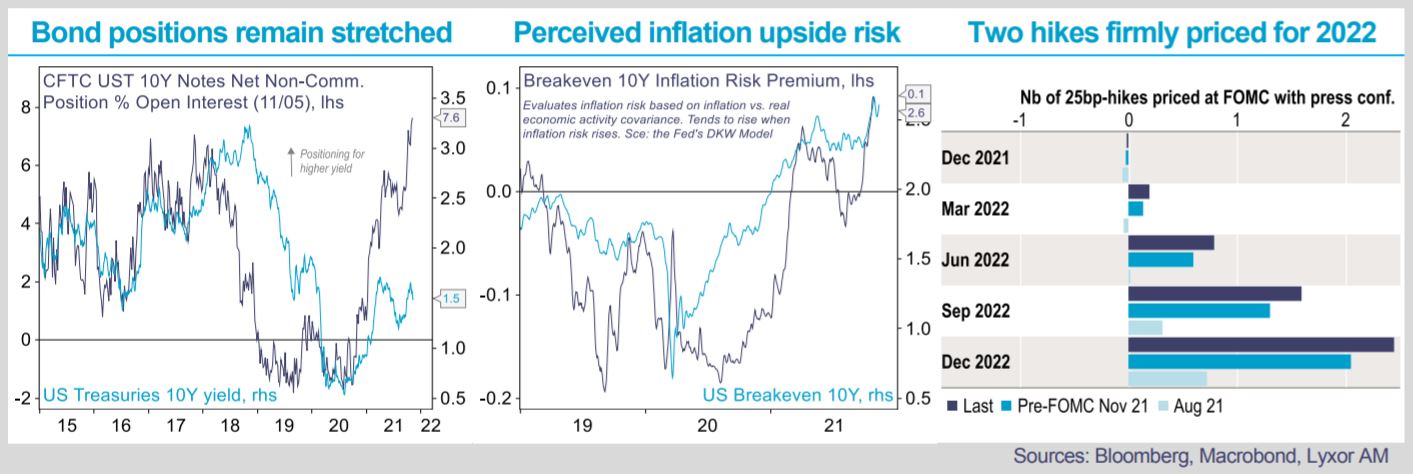

Gyrations in U.S. rates were highly challenging to navigate. Bond volatility surged in October as the Fed prepared to withdraw monetary accommodation and as investors struggled to assess the medium-term path of inflation.

Article also available in :

English ![]() |

français

|

français ![]()

Improving U.S. economic prospects, a delay negotiated regarding the debt-ceiling until year-end and progress on the infrastructure spending plan helped long-term yields head North until late October. However, short-term yields rose even faster ahead of the November FOMC, seen leaning on the hawkish side, which flattened the yield curve.

The FOMC turned out more dovish than expected. The Fed announced the start of tapering but signaled no rush to tighten rates, still seeing inflation as transitory, although some doubt was trickled in the statement. It led investors to dial back their rate hike expectations for 2022. Market reaction a few days later, after the strong payroll number, was feverish and counter intuitive. In contrast, trends were finally more decisive following the above-expectation inflation data published this week.

Markets are pricing a faster tapering pace, as well as a faster rate tightening cycle (with 2 hikes firmly priced for H2 2022), not convinced by the Fed that inflation will start to peak as soon as mid-next year. Even though they see inflation staying ’transitory’ for longer, they still anticipate moderation in the end, with a soft overall rate tightening cycle.

Various inconsistencies across markets, a surging inflation risk-premium and stretched investors’ bond positioning continue to reflect high uncertainty regarding the longer-term inflation path, while short-term inflation is clearly seen firming still.

Pain trade for Global Macro managers. These moves were costly for Global Macro managers, a majority of which remained short bonds, especially in the U.S., and positioned for a steepening of the yield curve. Dispersion across the strategy was elevated. Some offshore managers, highly leveraged and concentrated on fixed income markets, severely underperformed. In contrast, more liquid and UCITS macro strategies were more resilient thanks to higher diversification.

Most managers reduced their exposures throughout October, either hitting stop-losses or cutting risk amid high uncertainty in bond markets. Yet, they stick to their view that firming inflation and a benign macro environment will lead to a steepening of the curve and a rise in long-term yields. They are also long dollar, expressing higher relative U.S. inflation and growth.

Global Macro managers’ exposures are likely to be softer until year-end. The bond market might be less volatile with fewer remaining catalysts, including the job report and debt-ceiling issue in early December, and the FOMC mid-December.

Managers that underperformed have reduced dry powder, while those that outperformed would seek to lock their gains.

CTAs were resilient. CTAs endured much smaller losses in bonds. Initially long bonds in early October, they gradually cut their

exposures and are now short. They also made gains through their long equity, dollar and commodity futures.

Jean-Baptiste Berthon , November 2021

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |