| https://www.next-finance.net/en | |

|

Opinion

|

BoE to proceed very cautiously following its first rate hike in a decade

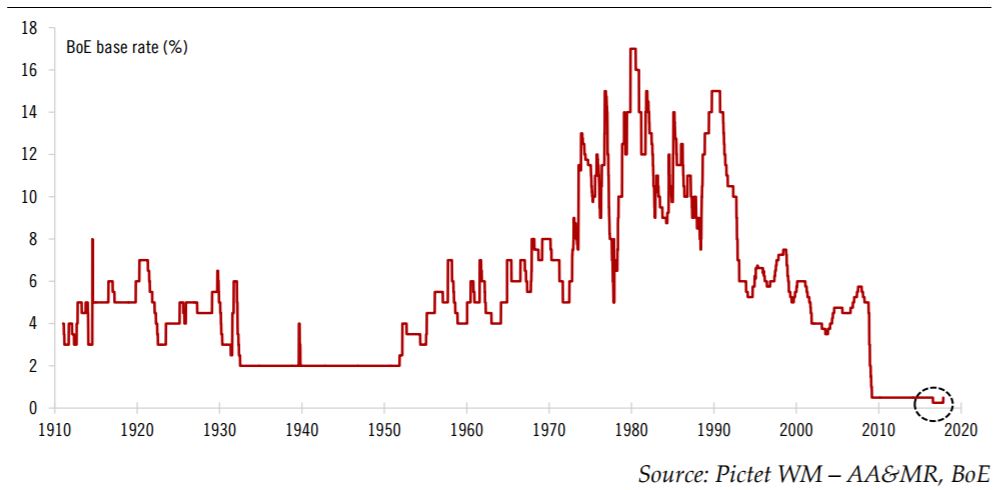

The Bank of England (BoE) has delivered a much-anticipated 25bp rate hike, tightening its monetary stance for the first time in over 10 years (or 3,773 days to be precise). The Monetary Policy Committee (MPC) 7-2 vote on rates was at the hawkish end of market expectations...

The Bank of England (BoE) has delivered a much-anticipated 25bp rate hike, tightening its monetary stance for the first time in over 10 years (or 3,773 days to be precise). The Monetary Policy Committee (MPC) 7-2 vote on rates was at the hawkish end of market expectations. Moreover, the hike was not described as ‘one and done’, a strategy which could have backfired. Instead, the BoE hinted at “gradual and limited” future rates hikes.

However, the BoE removed a key sentence from previous statements, that monetary policy might need to be tightened “by a somewhat greater extent than market expectations”. This prompted a dovish market reaction, along with further comments on the “considerable risks” to the outlook. Despite marginally better economic news, the BoE downgraded its assessment of the supply-side once again. A key argument remains that weak productivity will translate into even lower potential growth, ‘limited’ economic slack and, ultimately, rising price pressure when full capacity is approached. Meanwhile the BoE sees CPI inflation slightly above target, at 2.1% by end- 2020, based on the assumption of two further rate hikes over the next 3 years.

We remain of the view that a Brexit transitional deal will be a necessary condition for the BoE to hike rates again (in May 2018, as per our baseline), although it may not be a sufficient one.

In particular, wage growth needs to pick up to at least partially compensate for the loss in households’ disposable income. Looking further ahead, the BoE would be in a position to normalise policy further only in the event of a soft Brexit maintaining the UK’s access to EU markets, in our opinion, hiking rates every 6 to 9 months, up to a terminal rate which we estimate at around 1.5%.

Chart 1: a first BoE rate hike in more than a decade

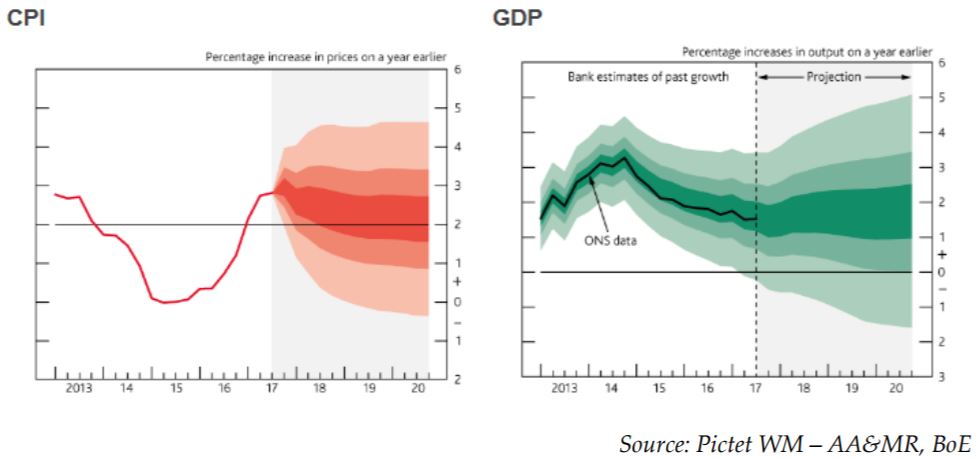

The UK political and macroeconomic outlook has not changed dramatically since we last updated our baseline scenario. Cyclical indicators were marginally stronger than expected in recent months, and real GDP growth came in 0.1pp above expectations, at 0.4% quarter-on-quarter (q-o-q) in Q3. But, if anything, forward-leading indicators continue to point to a moderate slowdown in activity despite stronger global growth. In the end, the BoE made only small downward revisions to its growth forecasts, with GDP expanding by 1.6% in 2017-18, and by 1.7% in 2019-20.

Households and enterprises still face the same headwinds capping spending, including a large fall in real incomes and a close-to-record-low household savings ratio. A sustained increase in nominal wage growth would be needed to boost disposable incomes and prevent the slowdown in GDP growth we are forecasting in 2018, to 1.0% on average. That is what the BoE is expecting via a “sustained rise” in wage growth based on labour market developments (including a somewhat faster-than-expected reduction in slack as unemployment fell to a 42-year low) and high vacancies.

In the end, the revisions to CPI inflation forecasts were also modest. The 18% past decline in sterling is still blamed for the bulk of the inflation overshoot, and the BoE continues to forecast inflation to ease back toward its 2% target over the forecast horizon, with the end-2020 point at 2.1%: “with little slack remaining and diminished growth in potential supply, modest demand growth is sufficient to restore domestic inflationary pressure”.

Chart 2: November 2017 BoE projections for CPI inflation and real GDP growth

To be sure, a 25bp rate hike is unlikely to trigger a meaningful economic slowdown, let alone a recession. The interest rate burden remains manageable, and the effect of higher rates could easily be offset by a small rise in nominal wages. Ultimately, the medium-term outlook remains dominated by the outcome of Brexit negotiations, hence a binary outcome. We stick with the view that a compromise will be reached at the December EU Council on several key issues. Importantly, the focus seems to have shifted to a more comprehensive settlement of financial liabilities, as well as the first contours of a post-Brexit trade framework. A December deal would move negotiations to the next stage and, ultimately, lay the ground for a transitional deal. The latter is a necessary condition for the BoE to continue normalising rates at a gradual pace, in our view, as we forecast a second 25bp hike in May 2018. Only in the event of a soft Brexit maintaining the UK’s access to EU markets would the BoE be in a position to tighten further.

Frederik Ducrozet , November 2017

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |