| https://www.next-finance.net/en | |

|

Opinion

|

UK Equities: Resurrection of the deplorable asset class!

If the UK equity market was out of favour at the beginning of 2020, it’s even more so now. Until the arrival of three vaccines prompted a wave of market exuberance towards the end of the year, UK equities had fallen approximately 20%. The only two worse-performing equity markets were Russia and Brazil...

Article also available in :

English ![]() |

français

|

français ![]()

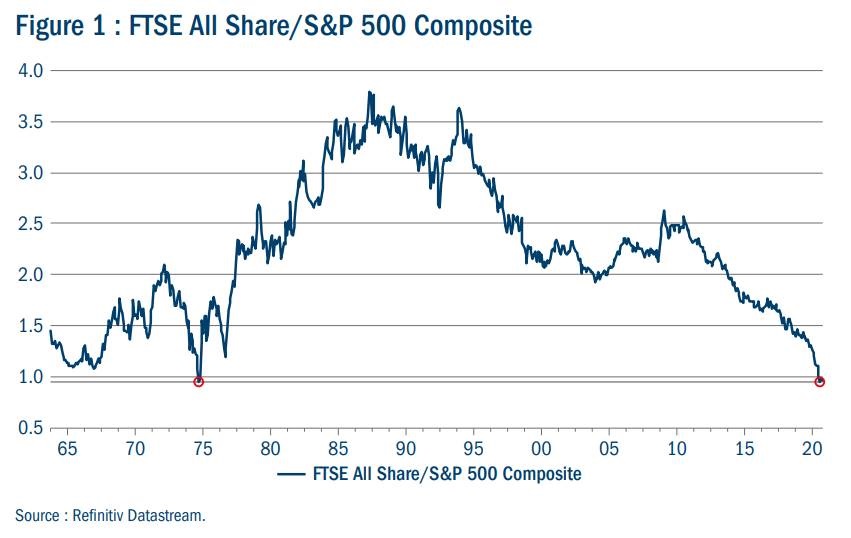

- The UK remains very much out of favour, with only Russia and Brazil performing worse year-to-date, and asset allocators still reluctant to look at UK equities, which are even cheaper than they were a year ago. International companies listed in the UK, pound-for-pound are on double discounts versus if they were quoted in Europe or the US, and an average of a 40% discount to the World MSCI.

- That the UK remains so unloved typifies the high levels of consensus thinking in markets. We continue to firmly believe in the UK, but trends often go on for longer than predicted. This creates the opportunity we see today, as it amplifies the impact when the switch in momentum finally occurs.

- Brexit has finally been determined and the late, thin deal provides some certainty, as would a reasonable recovery in 2021. Given this, a lot of the short positions against UK equities are likely to be closed. Although Brexit will still result in some short-term frictional trade costs, this deal is a good outcome, removing a large part of the uncertainty that has weighed on UK equities in recent years.

- Dividends have a critical role in pensions, savings and the income of the British public. The unprecedented nature of the pandemic, and the consequential need for companies to restore their liquidity, led to a contraction in dividend payments in April and May which was one of the quickest, sharpest and broadest ever encountered. This is a process which comes at close of every cycle, but Covid-19 meant it was condensed into just three weeks. However since then, as conditions have stabilised, the tide has turned and 60 companies have already reinstated dividends. More will follow.

- Looking ahead we expect more prudent policies and better cover, and even in the worst-case scenario the UK market should still offer a healthy yield premium to bonds by next year. For now, however, balance sheets and liquidity are paramount.

If the UK equity market was out of favour at the beginning of 2020, it’s even more so now. Until the arrival of three vaccines prompted a wave of market exuberance towards the end of the year, UK equities had fallen approximately 20%. The only two worse-performing equity markets were Russia and Brazil and asset allocators remain reluctant to look at UK equities, [1] which are now even cheaper than they were a year ago.

In previous market crashes, the stocks that led the markets higher in the earlier peak years have suffered most in the shakeout. Logically, that would mean US technology or China stocks being this year’s laggards; yet in 2020 they stand out as the brightest stars in global markets. Meanwhile international companies listed in the UK, pound for pound are on double discounts versus if they were quoted in Europe or the US. An average of a 40% discount to the World MSCI! [2]

Bipolar marketplace

Equity markets have become bipolar, with the five big US tech stocks – Facebook, Apple, Alphabet, Amazon and Microsoft – accounting for most of the US equity market’s strong performance. But there are twists and turns to come. As UK chancellor, Rishi Sunak, said in the November Spending Review, the country’s 11.3% contraction in GDP for 2020 is the biggest for 300 years. [3] Although the economy is forecast to recover in 2021 and 2022 we still have a boneshaker ride ahead.

"We continue to firmly believe in the UK, but trends often go on for longer than predicted. This creates the opportunity we see today, as it amplifies the impact when the switch in momentum finally occurs"

Consider how quickly the UK equity market rotated after Pfizer and BioNTech announced their successful Covid-19 vaccine data in mid-November. Many months of outperformance by growth stocks was erased in a single day, revealing that many investors have similar positions. The proliferation of quantitative investors, ETFs and factor-based investing has made the market unbalanced and typifies the high levels of consensus thinking.

We continue to firmly believe in the UK, but trends often go on for longer than predicted. This creates the opportunity we see today, as it amplifies the impact when the switch in momentum finally occurs.

Beware the closing window

However, the window on unlocking this potential value is closing. While sentiment about the UK economy has been hurt by both Covid-19 and Brexit, the equity market does not need a great recovery to perform better.

Brexit has finally been determined and the late, thin deal provides some certainty, as would a reasonable recovery in 2021. Given this, a lot of the short positions against UK equities are likely to be closed. Although Brexit will still result in some short-term frictional trade costs, this deal is a good outcome, removing a large part of the uncertainty that has weighed on UK equities in recent years.

By the end of 2021 investment should be building up and businesses getting back on their feet. Sadly, there will be more insolvencies than there were after the global financial crisis, because banks have more capital today and can afford to call in their bad debts, and unemployment may reach similar levels to the 1980s, when three million people were out of work.

But the UK stock market is coming off very depressed valuations. Hence why mergers and acquisitions remain high and are accelerating, because there is a lot of appetite to ignore the short-term noise and focus on valuations – not from market practitioners, but rather private equity and US corporates. They see time is running out. The former remain too timid to exploit this valuation arbitrage, but waiting much longer for the certainty with which to act may see the opportunity lost.

Dividends are coming back

Dividends have a critical role in pensions, savings and the income of the British public. The unprecedented nature of the pandemic, and the consequential need for companies to restore their liquidity, led to a contraction in dividend payments in April and May which was one of the quickest, sharpest and broadest ever encountered. This is a process which comes at close of every cycle, but Covid-19 meant it was condensed into just three weeks. However since then, as conditions have stabilised, the tide has turned and 60 companies have already reinstated dividends. [4] More will follow.

But looking ahead we expect more prudent policies and better cover, and even in the worst-case scenario the UK market should still offer a healthy yield premium to bonds by next year. For now, however, balance sheets and liquidity are paramount.

The best opportunities for a decade

As the UK’s double discount starts to narrow, following the greater clarity that Brexit should bring and as vaccines progress, 2021 and into 2022 could be exciting for the UK equity market. Even the UK’s quality growth companies like Unilever are a lot cheaper than their rivals globally. We believe it’s not just one or two areas of the UK market that are cheap; the whole market is cheap!

"As the UK’s double discount starts to narrow, following the greater clarity that Brexit should bring and as vaccines progress, 2021 and into 2022 could be exciting for the UK equity market"

The best time to invest is when it feels uncomfortable. For sure, the UK remains out of favour, but three quarters of UK companies’ profits come from international markets, so the market should be driven by global GDP.

As active managers we are excited about the UK market. We see some of the best opportunities in distressed stocks for a decade. While quantitative investing and factor investing focuses on which buckets stocks are in – a form of paint by numbers – active management logically relates the value offered by a stock to its price. We look forward to a levelling up for the UK market and its unloved companies.

Richard Colwell , January 2021

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] Bloomberg, Morgan Stanley, as at 30 September 2020.

[2] Morgan Stanley, as at 30 September 2020.

[3] FT.com, Sunak warns of ‘economic emergency’ as borrowing hits record £394bn, 25 November 2020.

[4] Badon Hill Asset Management/Columbia Threadneedle, November 2020.

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |