Why the ECB asset quality review, stress test raise longer term questions

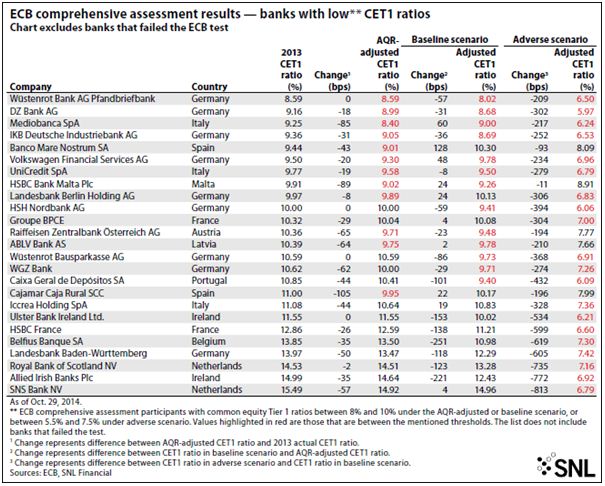

Although "only" 25 banks failed the ECB test, the central bank’s health check shows that others have reasons to be concerned. SNL data sheds light on some of the implications of the exercise, not only for the failed banks, but also the "near misses."

SNL’s tables showing the asset quality of the failed banks indicates that they could require more capital than the ECB has demanded. Few show an AQR-adjusted coverage ratio higher than 50% with several having figures below 30%. Moreover, the coverage ratios of the loans newly-classified as nonperforming are typically lower than extant NPLs in the corporate book.

The AQR, however, saw coverage ratios rise in general due to adjustments based on the credit file sampling and projections as well as model differences. It particularly reflects collateral revaluation. In the list of the failed banks, this resulted in significant improvements in their coverage and thus important reductions in their stated or potential capital shortfalls.

Overall, while soured loans rose, their coverage did so too. Unsurprisingly, the AQR adjustments for NPEs particularly affected Austrian, Greek, Italian, Irish and Spanish lenders.

Next Finance , November 2014

See online : SNL Financial: Stress test raises longer term questions

Focus

Note EURO STOXX 50® Index implied repo trading at Eurex

This research paper focuses on the inseparable relationship between implied repo rates and equity index total return swaps. Written by Stuart Heath, Director Equity & Index R&D at Eurex, it covers the various aspects and calculations of both repo rates and the (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |