| https://www.next-finance.net/en | |

|

Strategy

|

Trumpflation : what now for investors?

Here we go again. As we saw post the UK’s EU Referendum result, financial markets sold off following Trump’s election win, with risk assets being the main casualty; however, by the end of Wednesday US equities were back in the black and investors took solace in Trump’s statesmanlike acceptance speech.

It’s only the beginning of the process and, like the Brexit vote, nothing has yet been set in motion from a policy standpoint. We were operating on the basis of ‘known unknowns’ and we are now moving to new ones. Nevertheless, the difference is that after the initial disturbance of the Brexit vote the result was local, while this shock is global and has wider ramifications.

It Has Been a Long Week – I’m Feeling TIPSY

A surprise outcome and a full Congress sweep for the Republicans mean that President-elect Donald Trump is more likely to deliver on some of his promises, starting with fiscal stimulus.

Inflation Take

After the overnight sell-off of break-evens (or inflation expectations) in sympathy with S&P500 Futures, break-evens rallied strongly on 9 November (Figure 1). As we wrote in early November, inflation is coming back, not roaring for sure, but it has pushed higher as 2015’s oil price declines are disappearing from the year-on-year figures. The move on 9 November pushed break-evens above the 2% non-binding inflation target of the US Federal Reserve.

We believe inflationary risk is more centred on the US than the Euro market currently, and investors may want to look at treasury inflation-protected exposures (TIPs).

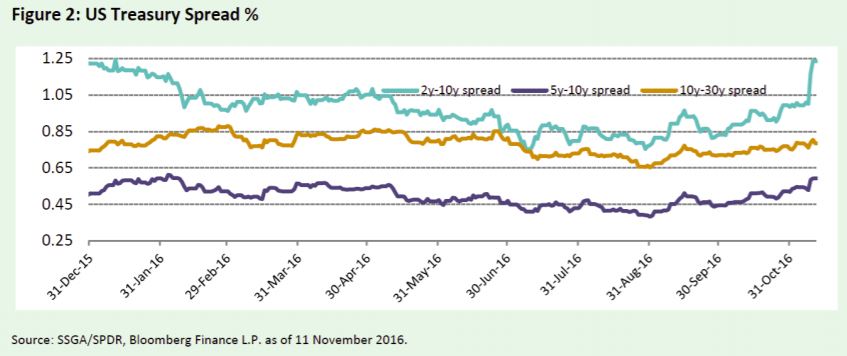

US Curve Implications: 2016 Reset

Implications for the US Treasury curve are yet to completely unfold, but are clearly impacted by the potential inflationary policies. The longer end of the curve has steepened sharply since the election outcome, with yields reaching 2.12% intraday on 10 November from 1.85% two days before.

Will this rebound above the 2% mark make it attractive for international investors to find longerterm entry points? As with every sharp move, it may be wise to let the dust settle. Nevertheless, with so much uncertainty, the sell-off may be limited, offering opportunities to position on steeper parts of the curves while managing duration risk.

Within nominal bonds, positioning on the steeper part of the curve – with either 5-7 or 7-10 year US Treasuries – would be an option. Meanwhile, as credit spreads remained well behaved and in line with the risk-on rotation, the 3-10 year part of the curve continues to be an area to analyse for a controlled carry and roll strategy.

Playing it with Sectors

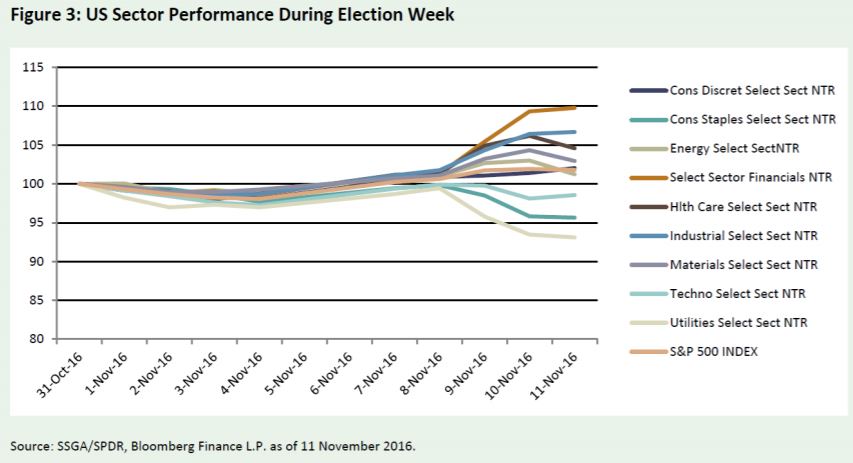

Sector investing has become more popular, as highlighted during the recent SPDR Sector Roadshows, and investors immediately wanted to pick between the sectors on the Trump news. This is what we’ve seen so far, with Health Care benefiting the most, as the market re-priced the discount in the sector that was based on a Clinton win. Beyond this initial move the sectors that bode well for an environment of fiscal expansion and reflation are Materials, Energy and Financials.

Materials are benefiting and should continue to do so, based on an increasing commodity price outlook and a pick-up in analysts’ earnings upgrades. The sector tends to pass through price increases, which is ideal in an inflationary environment.

The Energy sector has benefited from improved crude oil prices and industry self-help measures. Spending discipline has led to more astute investment decisions and fewer projects coming onstream; both these effects will help the oil market to come into balance with a better cost structure.

Within Financials, the funding and asset position of the banks are rate sensitive, and this slight steepening of the curve in the US benefits the sector. The banks have cut expenses aggressively in line with falling net interest margins whilst building up capital; this has led to high leverage to increased interest rates, which could improve profitability.

Being Smart About Our Beta

Going into the US Presidential Election, many investors had taken their bets off of the table and reduced equity exposure. The resulting cash balances are destined to come back into the market, and we have already seen significant flows into equities just over a couple of days.

The simplest way for investors to buy equity exposure remains via basic beta funds.

Our preference in US equities is outside of the mega caps. In particular, those with large overweight positions in Industrials versus the S&P 500 breakdown, and also attractive exposure to domestic earners.

Meanwhile, Smart Beta investing has been an enduring trend in recent years, and demand for strategies that do not rely on market capitalisation weighting, but focus on factors instead, should continue unabated despite the change of US political leadership.

Smart Beta investing offers a rules-based, transparent methodology that is reassuring in turbulent markets. On the whole, factors have shown better risk-adjusted returns over the long term, and in many cases offer downside protection and lower volatility. Factors will remain drivers in the highly correlated markets that investors are witnessing now.

US rate expectations are not remarkably different from before the Trump victory, with high probability of a Fed hike in December and another one or two rises next year, but no change to assumptions that globally the environment is still lower for longer. The search for sustainable income will persist.

Multi-factor strategies have been increasing in popularity, especially those with a ‘balanced yield’, offering Quality and Yield as well as an element of Lower Volatility.

Antoine Lesné , Tapiwa Ngwena , November 2016

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |