| https://www.next-finance.net/en | |

|

Opinion

|

The end of accomodative policies, a new challenge for asset managers

According to Arnaud Faller, Deputy Managing Director, Chief Investment Officer at CPR AM, in this environment, we shall clearly favour equities over credit investments in developed markets, while leveraging on current opportunities in emerging bond and equity markets.

Article also available in :

English ![]() |

français

|

français ![]()

The 2008 crisis caused a major shock for all developed and emerging economies. However, the stock market crash of 1929 - comparable in scope and nature – provided valuable experience and insight: fast and massive intervention from governments and central banks helped to avert the worst.

After bringing key rates down in all developed countries, central banks set exceptional monetary policy actions into motion. Stepping way beyond their traditional role as a lender of last resort, they flooded capital markets with liquidity, using increasingly daring mechanisms, before deploying asset purchase programmes in most countries. The volumes involved were unheard of: central banks owned over 20% of GDP in the U.S., over 30% in the Eurozone, and over 90% in Japan (of which a significant amount in ETFs).

Furthermore, the way central banks communicate evolved, as they moved towards “forward guidance”, providing information on the upcoming policy as early as possible, at least in broad terms even if details cannot be disclosed.

This largely contributed to stabilising shortterm, and therefore long-term, rate forecasts. However the most successful form of communication came from Mr Draghi, Chairman of the ECB, when he publically stated that he would do “whatever it takes” to save the Eurozone, and probably did in the process.

Central bank communication is now scrutinised in its finest detail - every six weeks when the scheduled meetings take place, but also whenever one of the members makes a statement.

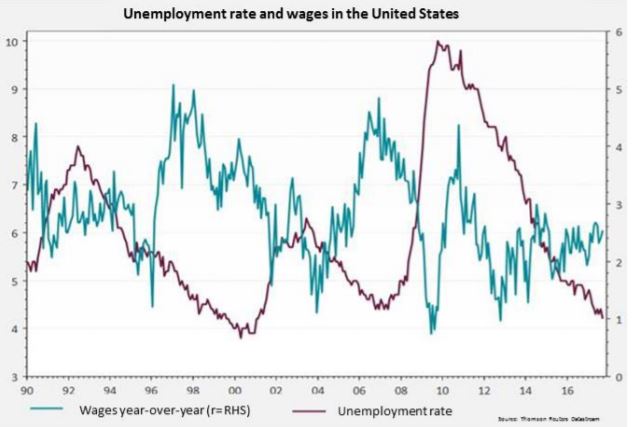

The end of these extraordinary monetary policy measures is now in sight, with the disappearance of deflationary risks. However inflation has still not returned - “a mystery” to quote Janet Yellen. Is the technological disruption, which is driving long-term changes in consumer behaviour, causing durable disruption to inflation models? More recently, timid wage growth has continued to raise questions, considering the current stage of the cycle.

To decipher this lack of inflationary pressure, it will be important to make a clear distinction between structural (demographic for instance) and environment-related factors (such as the return of long-term unemployment).

We firmly believe that the environmentrelated factors will wane, enabling inflation to rise beyond 2%, even if structural factors mean that the scenario of run-away inflation cannot materialise.

The fact remains that central banks will not wait until their inflation targets are reached before they start to normalise monetary policy. In this respect, the Federal Reserve has already, very gradually, upped its interest rate and has started not to reinvest some of the proceeds from maturing bonds. The ECB is planning to make further cuts to the volume of asset purchases in 2018.

The presence of central banks across the entire yield curve, but also in the corporate bond market, has disrupted the normal running of capital markets.

Volatility collapsed in the corporate bond market; this made sense, but also indirectly affected the equity market. Furthermore, these low volatility levels stem from the huge sector dispersion observed across markets today. This is particularly true in the United States, where technology and real estate stocks have rallied by over 30% in 12 months and have more than offset the losses posted by the energy or food retail industries (-20%). Volatility then spread to currencies, a perfect example of which would be the exceptional performance of the dollar in recent weeks. Investors will also need to keep a close watch on credit valuations as several records have been broken: last summer, several high yield corporate bonds in the Eurozone yielded less than 10-year U.S. Treasury bills!

This normalisation process will take time and in all likelihood, the target level for key rates will be much lower than it was in the past. It will also be very gradual: central bankers are perfectly aware of their important role in driving capital markets and now pay great attention to “preparation” - as they do when managing the probability of a Fed fund hike ahead of each meeting. Currency market volatility has created an additional challenge for central bankers. Officially, they do not have forex objectives; however markets sometimes react violently depending on the decisions they make. The interaction between “driving markets”/ “market over-reactions” to the statements made/measures taken by central bankers is particularly challenging.

The structure of the market has also undergone durable change, driven by the numerous and diversified regulatory measures impacting banks, insurance companies and asset managers. As a result, deals between final investors have grown significantly (intermediation). Questions remain over the real and effective liquidity that will be available in crises to come. Some market observers have rightly pointed out that liquidity is available when investors have little need for it, and then disappears when they require it. Measuring liquidity objectively is an extremely difficult task in markets operated by market makers, who have no interest at all in being transparent over their capacity for position-taking.

‘‘Regulation impacts liquidity as a whole and this will be a major challenge when central banks leave the scene’’

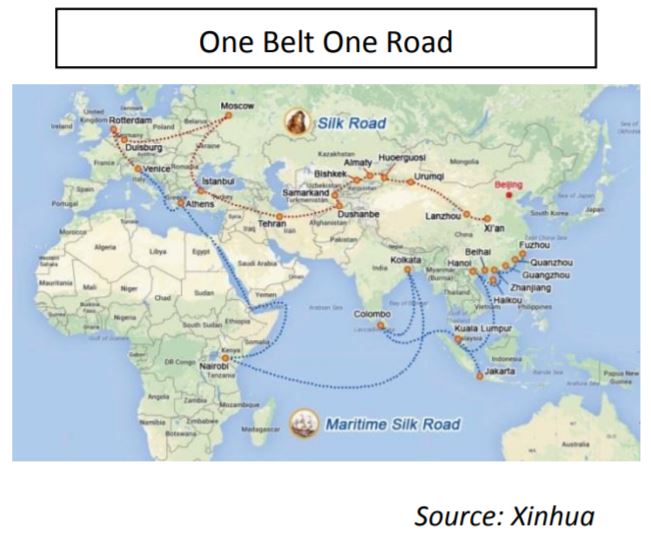

Events of recent weeks have shown how political developments can cause disruption to financial markets. First in line is U.S. domestic policy, with President Trump’s unpredictable behaviour and the procrastination over the project for fiscal reform. In Europe, the impact of Brexit – both on the British economy and capital markets, including international – has not been truly factored in. Furthermore, developments in the emerging world often tend to be overlooked when analysing market changes. Yet China is undergoing considerable transformation; the government is determined to bring about change and to create a service-driven country based on a sustainable economic model. This transformation implies major investment in renewable and all-electric energy, but also abroad, via the “One Belt, One Road” programme designed to bring China closer to Europe via the Middle East.

Clearly, this major crisis has caused deep changes to the global economic environment and to the way capital markets operate. These upheavals that are currently at play are still difficult to grasp; and in any event, they cannot be measured effectively using available statistical tools. However, in the short-term, some areas of certainty remain, such as the controls exerted by central banks on fixed income markets.

As no one expects inflation to accelerate sharply, the control from central banks does help to limit the risk of a crash on bond markets.

Nonetheless, it is true that a badlyorchestrated rise in interest rates can trigger a severe correction in equity markets. We are also convinced that the credit market will be subject to the ECB’s tapering policy sooner or later.

In this environment, we shall clearly favour equities over credit investments in developed markets, while leveraging on current opportunities in emerging markets (both bonds and equities). This new market environment is not as favourable as it once was to contrarian position-taking; markets are momentum-driven at the moment and due to regulatory changes, banks have invested less of their own equity in the market.

Nevertheless, according to financial theory, the “momentum approach” has not shown a clear ability to outperform a “contrarian approach” in the context of asset allocation.

It will therefore be important to use diversification as a performance driver (always useful as long as the “true” correlations between assets are estimated – hence the importance of a multi-scenario approach); fund managers will also have to demonstrate a high degree of flexibility in order to adapt to the various shifts in market regime that are bound to occur.

Arnaud Faller , November 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |