| https://www.next-finance.net/en | |

|

Strategy

|

Quality, the positive factor

Quality is positive: it is about good companies that are efficient at managing their businesses profitably, creating shareholder value and being rewarded with above average returns. Yet, quality is not always easy to recognise or measure. Here are a few pointers for avoiding some common misconceptions and mistakes.

Article also available in :

English ![]() |

français

|

français ![]()

Quality is positive: it is about good companies that are efficient at managing their businesses profitably, creating shareholder value and being rewarded with above average returns. Yet, quality is not always easy to recognise or measure. Here are a few pointers for avoiding some common misconceptions and mistakes.

Quality is about how healthy and competitive a given company is relative to others

Quality companies typically have competitive advantages, market dominance or simply manage their businesses more efficiently, which translates into higher profitability. And, of course, quality companies will have in place competent and honest management teams which make sure that the profits are passed on to the shareholders rather than being used to pursue more self-servicing interests.

Measures of profitability are based on the fundamental data of the company

The typical measures of profitability are Return on Capital or Return on Equity. Return on Equity (RoE) has become a preferred basis for many CEOs in deciding their strategy, because it measures how efficiently the company uses its shareholders’ money. Recent free cash flow or gross margin are good proxies for this underlying idea that the company is ‘increasing its freedom’ to invest or to buy competitors in order to increase its profitability. Of course this is rather more ‘nowcasting’ than actual ‘forecasting’.

Another measure that relates to quality emerged in the 90s in academic research: that of accruals

Accruals measure the capacity of a company to be paid sooner rather than later for the products or services it has provided. A company with low accruals – money billed out that it is waiting to receive – is one that generally either has a sounder balance sheet or, alternatively, a better-than-average bargaining power, being able to borrow from its suppliers and clients by charging first and paying later.

Just as for value, which is also a fundamental factor, the performance of the quality factor can be explained by the behavioural fact that investors under-estimate the importance of financial data analysis, compared to the stories told by the senior managers of companies.

The trouble with quality is that can be slightly over-optimistic. The truth is that efficiently managed and more profitable companies are not always rewarded.

Etienne Vincent, Head of Global Quantitative Management, THEAM

Etienne Vincent, Head of Global Quantitative Management, THEAM

The trouble with quality is that can be slightly over-optimistic. The truth is that efficiently managed and more profitable companies are not always rewarded – sometimes they can be hit by external changes in the economy, and sometimes by the fact that financial market professionals simply overlook fundamental data when stock picking. Quality has been a favourable investment style in the last few years. One risk is that an increasing number of fund managers investing in quality stocks will lead to overcrowding and potential underperformance of the style. Nevertheless we remain supportive the approach of thinking positively and investing in quality.

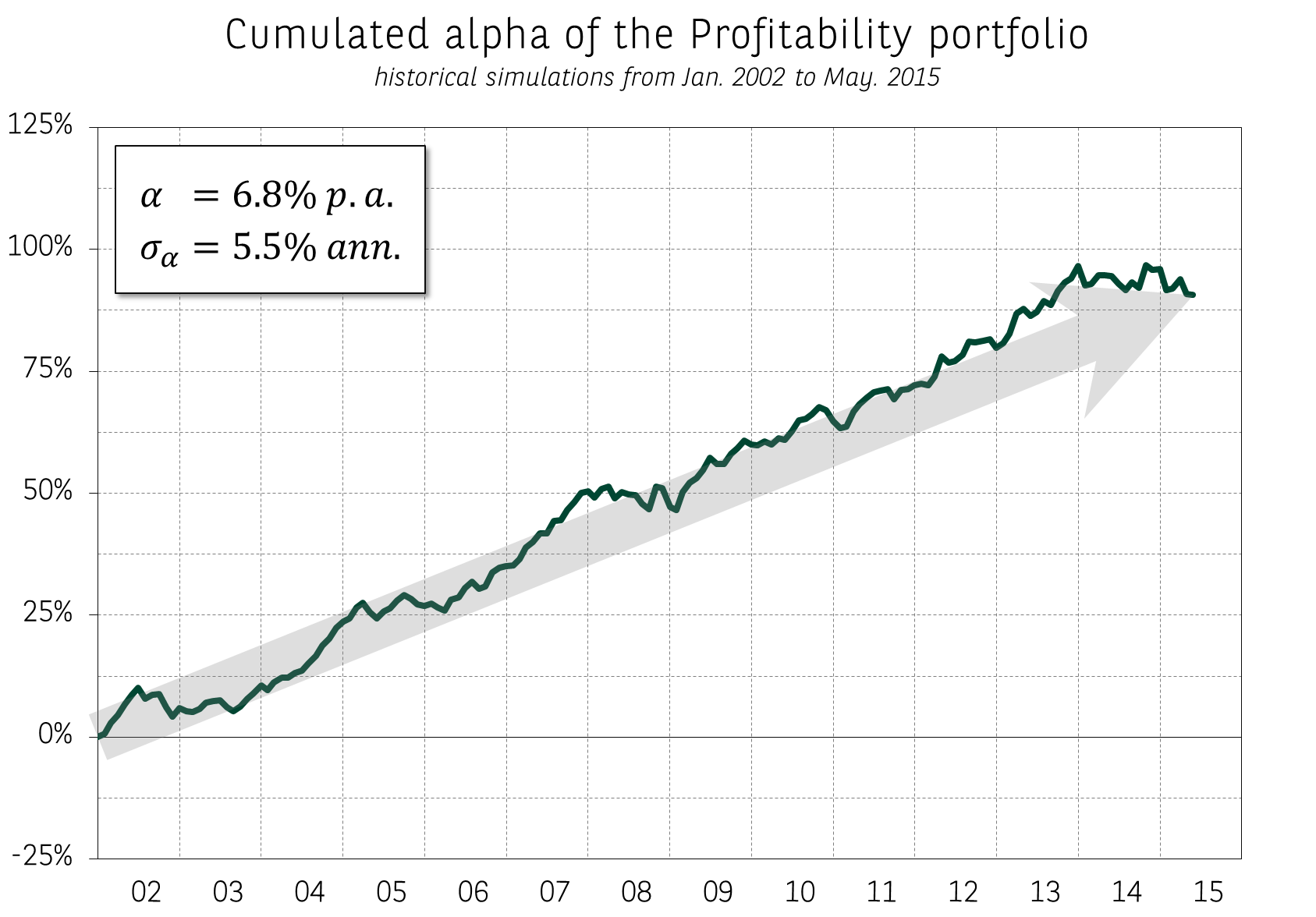

Exhibit 1: Historical simulations of a long-short portfolio based on MSCI World Universe

- Source: MSCI, Exshare

Etienne Vincent , April 2017

Article also available in :

English ![]() |

français

|

français ![]()

See online : Quality, the positive factor

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |