Macro funds’ patience on Fed and Brexit pays off

Nervousness rose last week as investors continued to prepare for a December Fed hike - increasingly likely - and ahead of the US elections. US rates, the dollar and breakevens progressed, while equities dropped slightly.

Article also available in :

English ![]() |

français

|

français ![]()

Nervousness rose last week as investors continued to prepare for a December Fed hike - increasingly likely - and ahead of the US elections. US rates, the dollar and breakevens progressed, while equities dropped slightly. Meanwhile, markets are waiting for a confirmation that the ECB, BoJ and BoE actually shifted to a less dovish stance and pushed back NIRP (negative interest rate policy). In that context, trading volumes remained low, and rotations in and out of rate sensitive sectors were frequent.

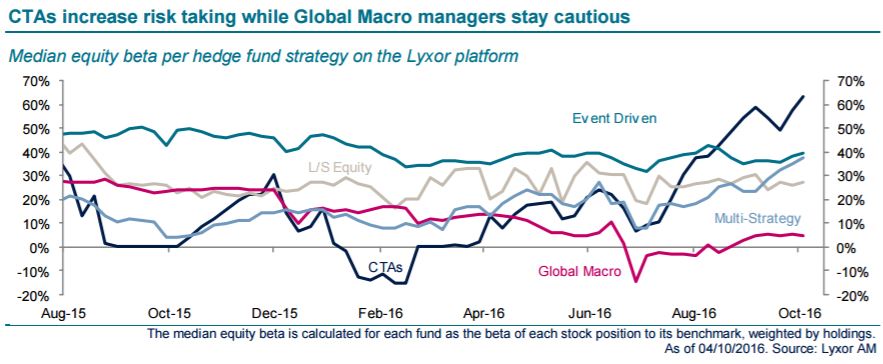

Hedge funds were boosted by the strong performance of Global Macro funds. Their short on the pound positioning was a major boost, which was further helped by their short stance on the Euro and US bonds.

By contrast CTAs underperformed on their long bond positions. Sector rotations hit L/S Equity Market Neutral funds negatively. The stress on equities eroded the longest bias funds’ returns.

Doubts regarding the benefits of quantitative easing are intensifying. Meanwhile developed markets’ central banks seem to be shifting toward a less dovish stance. Evidence of this shift in the coming monetary meetings would be a strong positive for hedge funds. Their alpha generation actually suffered from QE and the prevalence of speculative drivers.

With that perspective in mind, we are prepared to reweight more firmly the whole Global Macro group. Fewer monetary-driven sector rotations also make us more comfortable with our slight overweight on L/S Equity neutral funds.

For now, we remain neutral on CTAs. The trend-following environment hasn’t recovered yet from the shifts in rates. We wait for a stabilization in these markets.

We also maintain our neutral stance on L/S Credit funds, which are constrained on both their beta and alpha. However we still favor Multi-Credit Arbitrage. Finally, we reiterate our preference for Merger over Special Situations and distressed funds. The former face higher risks, but attractive spreads.

Lyxor Research , October 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |