Gilt wobbles fuel Global Macro strategies

Mounting signals that the latest leg of the bond market rally has started to reverse fueled hedge fund strategies last week. Most recent inflation prints outpaced expectations both in the U.S. and the U.K., as consumer prices rose +1.9% and +2.9% year-over-year in August, respectively.

Article also available in :

English ![]() |

français

|

français ![]()

Mounting signals that the latest leg of the bond market rally has started to reverse fueled hedge fund strategies last week. Most recent inflation prints outpaced expectations both in the U.S. and the U.K., as consumer prices rose +1.9% and +2.9% year-over-year in August, respectively. Sovereign bond yields rose in developed markets, in particular in the U.K, and yield curves steepened somewhat. Meanwhile, equity markets extended their winning streak both in developed and emerging markets.

Such developments have been largely supportive for hedge funds, with all strategies in positive territory last week. Fixed income arbitrage strategies outperformed, which is in line with our expectations in a rising yield environment.

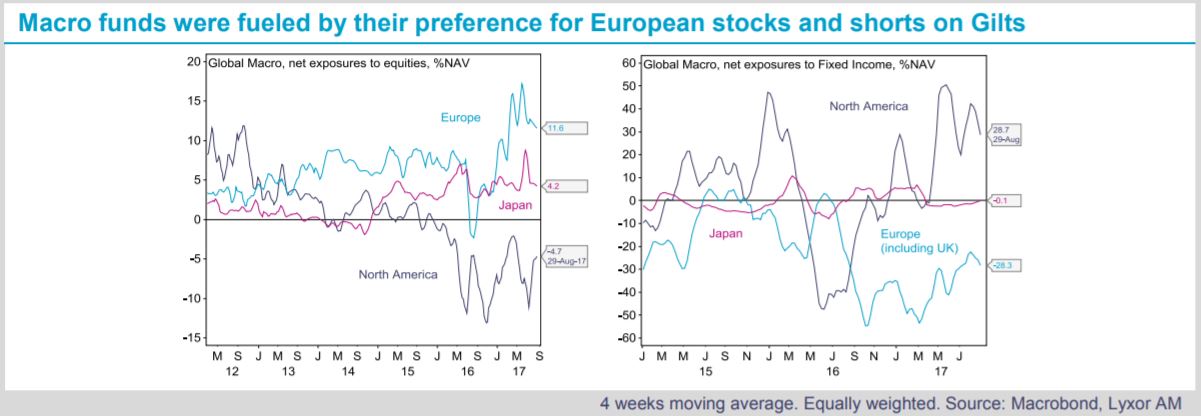

Global Macro managers delivered upbeat returns from their short Gilt allocations, despite the mild loss occurred from short GBPUSD positions.

Macro managers were also fueled by their preference for European stocks vs. U.S. stocks.

Going forward, we anticipate bond yields to edge higher, amid buoyant macro data releases and expectations that the Federal Reserve will start shrinking its balance sheet in the coming weeks. Additionally, we expect the U.S. administration to move forward with tax reforms, which would contribute to lift Treasury yields. Implications for hedge funds strategies loom large.

Fixed income arbitrage is attractive in our view (overweight) but we are cautious on directional L/S Credit funds (underweight). CTAs (neutral) would be vulnerable if trend reversals in FX and Fixed Income do occur.

However, the strategy is currently a good diversifier if our scenario on bond yields does not materialize. We maintain Event Driven at overweight, a strategy that we prefer to L/S Equity (neutral). In particular, we are defensive on L/S Equity market neutral funds (underweight) on the back of expectations of sector rotations triggered by rises in bond yields. Finally, within the Global Macro space, we maintain a preference for multi-asset and EM funds compared to discretionary Fixed Income/ FX specialists. Both asset classes are likely to remain challenging to navigate as central banks remove accommodation.

Lyxor Research , September 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |