| https://www.next-finance.net/en | |

|

Strategy

|

A smart selection process for ETFs

Logic might suggest that all ETFs replicating the same market index are themselves the same. And yet, you do not have to be an experienced ETF investor to know that this is clearly a misconception. In practice, performance can vary. It is necessary to know which objective criteria to use when selecting an ETF.

Until recently, there was no satisfactory scientific answer to this question, but Lyxor’s research teams have changed all that.

Traditional selection tools are not suited to ETFs

Institutional investors, such as pension funds, insurance companies and balanced fund managers who rely heavily on trackers, have to bear this in mind when choosing the best ETFs for their portfolio.

They face a major challenge. The analysis tools traditionally employed for active fund selection are not suited to selecting ETFs. In its simplest expression, active fund selection is based on one fundamental criterion: the information ratio. This indicator measures a fund’s return relative to its benchmark index, taking into account the relative risk taken compared with said index. However, using the information ratio to compare ETFs has a limitation which totally invalidates the analysis.

As a reminder, the information ratio is the ratio of outperformance (alpha) to tracking error (TE) volatility. In the case of ETFs, which replicate the index, the outperformance and TE figures are very low and the information ratios are therefore extremely sensitive, making traditional analysis irrelevant. Moreover, a product with a very low tracking error could easily be mistakenly ruled out on account of a weak information ratio, despite excellent index replication. Lastly, a product underperforming very slightly and with a very low TE will be ruled out on account of its negative information ratio, whereas a product with marginal outperformance will be retained even with a high TE.

ETFs have attracted a growing numbers of providers to the market, leaving investors faced with a difficult question: how to select the most efficient ETF? Lyxor has developed an “ETF Efficiency Indicator”, wich is a comprehensive solution used to compare and evaluate all ETFs

Thierry Roncalli, Head of Quantitative Research, Lyxor Asset Management

Thierry Roncalli, Head of Quantitative Research, Lyxor Asset Management

A new framework for measuring ETF efficiency...

Basically, from an investor’s point of view, a good ETF should maximise the chances of replicating index returns. The fund must also display a low bid-ask spread in order to preserve the profit on the trade. In fact, a suitable analysis framework for ETF selection derives from three fundamental parameters: an estimate of the performance gap between the fund and its benchmark (i.e. the tracking difference); the volatility of this performance gap (i.e. the tracking error); and the difference between the buy and sell prices (i.e. the bid-ask spread or “liquidity spread”). By applying Value at Risk (VaR) – now the most widely used measurement of risk – to these three parameters, it is possible to accurately measure the efficiency of an ETF.

In concrete terms, by using a one-year Gaussian VaR at

a 95% confidence level, this efficiency measurement is

expressed as follows:

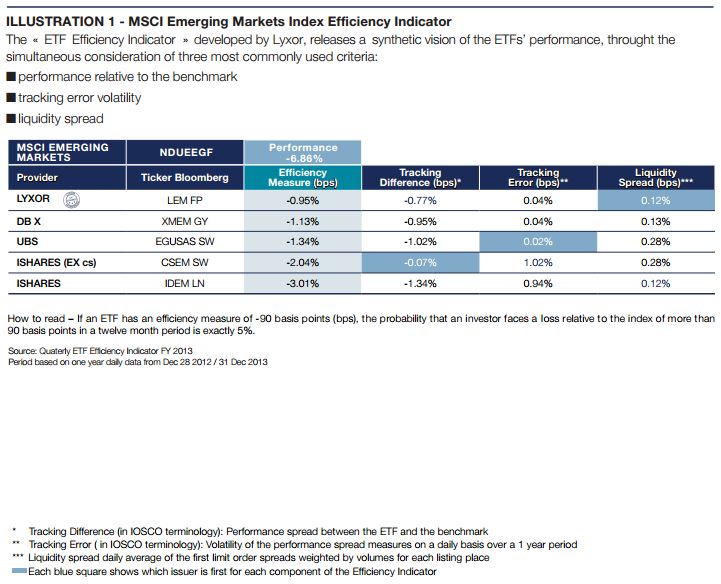

Efficiency = Tracking Difference – Liquidity Spread – 1.65 x Tracking Error

For instance, if the efficiency of the ETF is equal to -50 bps, the probability that the investor faces a relative loss with respect to the index larger than 50 bps is exactly equal to 5%.

Using this risk measurement therefore makes it easy to compare the efficiency of two ETFs. This model, which is described in detail in a research article available online at http://ssrn.com/abstract=2212596, and which was also published in Journal of Index Investing, works as follows. The higher the outperformance of an ETF, the better its efficiency, while a wider bid-ask spread makes it less efficient. Equally, higher tracking-error volatility increases uncertainty and thus makes the ETF less efficient. It is interesting to note that comparing ETFs by efficiency rather than by individual criteria available to investors (such as outperformance, daily spreads or volatility) produces different results. Therein lies the strength of this synthetic indicator.

ILLUSTRATION 1 - MSCI Emerging Markets Index Efficiency Indicator

...taking account of institutional concerns

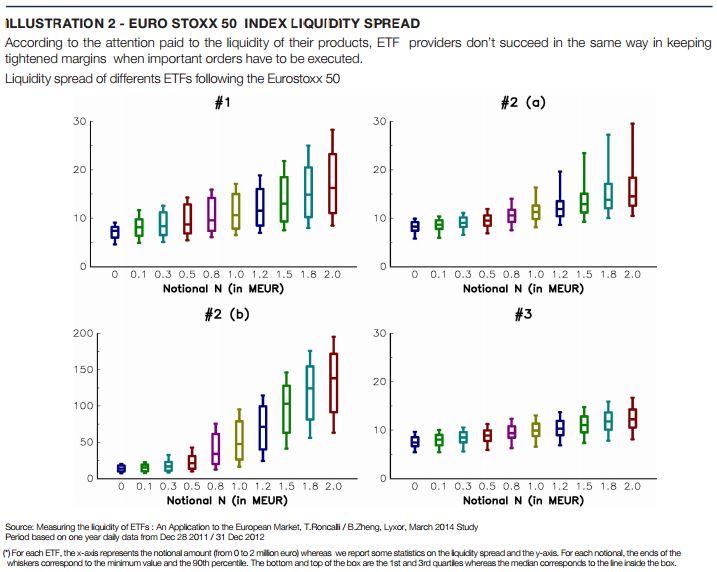

In the basic calculation for the efficiency indicator, we are using the best limit order spread for the liquidity spread. Yet, efficiency measurements can be refined in order to better reflect the daily realities of institutional investors. Such investors’ orders can involve amounts running into tens of millions of euro. Even when split, they generally cannot be executed at the best limit. Based on order-book historical data, it nevertheless remains possible to measure the average bid-ask spread at which a given notional amount will be executed. This “liquidity spread” can then be reintroduced into the calculation of the indicator. Interestingly, depending on whether the analysis uses a notional amount of 100,000, 1 million or 2 million euro, the efficiency measurement pinpoints different ETF providers for the same index. This highlights the importance of ETF liquidity for investors.

ETF providers eager to bring the highest level of service to their investors must endeavour to improve the liquidity of their products in order to minimise the bid-ask spread. Having a large number of market makers is important for ETF liquidity. At Lyxor, everything is done to ensure that each fund is followed on average by nine market makers. In addition, in order to allow each investor to use the model presented in this article and select ETFs efficiently, it is essential that ETF providers publish material on the tracking-error volatility of their funds, in line with recommendations provided by the European Securities Market Association (ESMA), and that stockbrokers develop suitable statistical measures for understanding ETF liquidity spread.

ILLUSTRATION 2 - Euro STOXX 50 Index Liquidity Spread

Thierry Roncalli , November 2014

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |