| https://www.next-finance.net/en | |

|

Opinion

|

A more dovish Fed? Taking stock with US dividends

As expected, the Federal Open Market Committee (Fed) kept official rates at their current levels when it met on 10 March. Despite inflationary pressure building, the Fed lowered its projections for the pace of future rate hikes given ongoing concerns about the global economy...

As expected, the Federal Open Market Committee (Fed) kept official rates at their current levels when it met on 10 March. Despite inflationary pressure building, the Fed lowered its projections for the pace of future rate hikes given ongoing concerns about the global economy.

While growth forecasts have been downgraded, it’s not all bad news for the US. We expect the US economy to grow by between 2.0% and 2.5% this year; not exactly a stellar performance but not in recessionary territory either. Overall, this backdrop is suggestive of a lower-for-longer environment, where investors’ search for yield will continue.

Arguably, markets have recovered from their jitters earlier this year but the outlook continues to warrant cautious optimism. In our view, these conditions favour stocks with the potential for dividend growth as a more balanced approach to obtaining yield than investing in the potential high yielders.

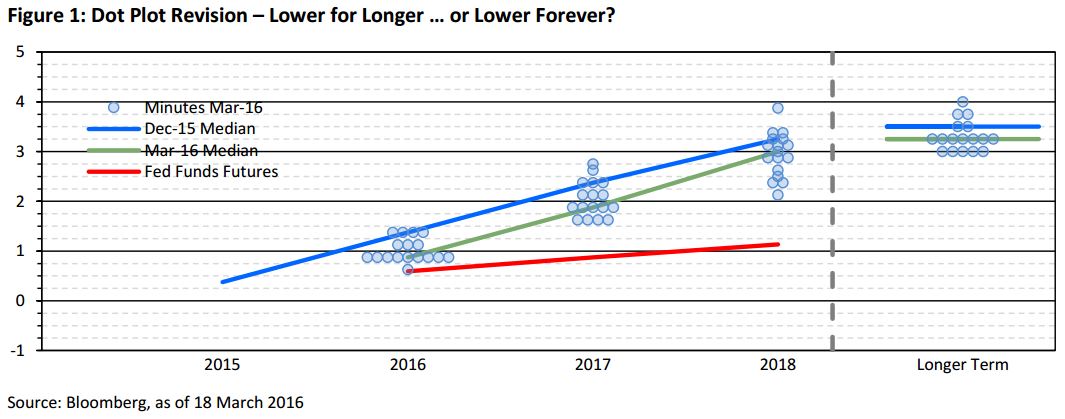

Lower for longer: downgrading the dot plot

After the European Central Bank’s policy announcement last week, the Fed had been expected to view conditions as improving. Yet lowered its projection for the pace of future rate hikes despite higher-than-expected core inflation reaching a four-year high of 2.3%.

As illustrated in Figure 1 below, Fed Funds Futures now imply fewer than two hikes this year, which is at odds with the FOMC’s medium-term projections. The dots show each individual governor’s expectations of where the Fed Fund rates could be at different time horizons. Meanwhile the red line shows what the financial market participants expect through the futures market levels, clearly lower than the median FOMC projections.

What does this mean for investors?

Ten-year Treasury yields fell following the meeting and have remained below 2% since 27 January this year, reflecting weaker economic growth expectations over the longer run and a very cautious outlook, despite relatively healthy inflation and job data.

Recent investor polls point to expectations of a slowdown in the US between the end of 2016 and 2018. With 24 consecutive quarters of positive growth [1] , the current cycle, one of the longest streaks of positive GDP growth since World War Two, may be nearing a turning point. This type of economic environment tends to be supportive of ‘longerduration’ sectors, which are generally overweighted in indices such as the S&P US Dividend Aristrocrats Index. For example, in the year to 17 March, while the S&P 500 returned a meagre 0.20%, Gas Utilities returned 7.4%, Industrial Machinery was up 6.5%, REITs rose 4.7%) and Multi-Utilities returned 3.9%.

With growth expectations having rolled over, dividend strategies - which tend to offer more stable yield - may present investors with an alternative source of income amid the low-yield backdrop.

However, it’s important to differentiate high yield from dividend growth. Whilst an above-average yield is an important component of total return, a company’s ability to consistently raise its dividends is more important over the long term.

Even if modest interest rate rises are expected in the US, consistent dividend growth rather than yield alone has historically been more attractive in rising rate environments. In addition, firms with consistent dividend growth have tended to have higher-quality balance sheets and, as a result, may offer downside protection in turbulent markets.

Year to date, equity markets (particularly in the US) have struggled to generate positive performance in an environment of ongoing uncertainty. However, some US equity exposures have achieved a lower drawdown and outperformed traditional large-cap indices. Investors would do well to consider indices, which this exposure, such as the S&P US Dividend Aristocrats Index which returning 8.25% in the year to 17 March versus 0.20% for the S&P500 (in US dollars, net return). The Dividend Aristocrats Index has also outperformed yield-focused indices, for instance, returning 3.7% more than the MSCI USA High Dividend Yield Index.

Antoine Lesné , March 2016

Footnotes

[1] Source: Bloomberg, Bureau of Economic Analysis, as of 31 December 2015

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |