| https://www.next-finance.net/en | |

|

Opinion

|

A Dovish Fed is Set to Support CTA and Macro Managers

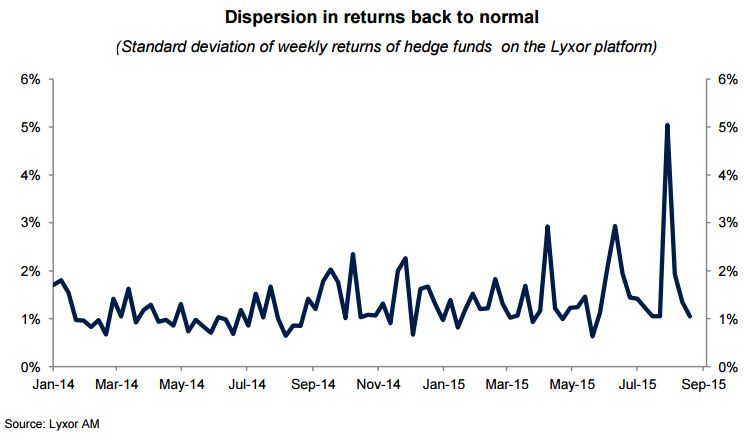

Markets were on standby mode ahead of the Fed’s meeting last week. Hedge funds were flat and there was little dispersion in returns across the managers (see chart). Event-Driven outperformed as equity volatility edged lower. Meanwhile, Fixed Income strategies underperformed as sovereign bond yields moved higher.

Since the FOMC meeting on September 17th, the Fed’s indecisive attitude has been met with mixed responses from the markets. A lack of guidance has not been welcomed by risk assets, bonds have rallied and the USD has eased against major currencies. It is likely that this will fuel Global Macro and CTA managers in particular.

Systematic funds are adequately positioned, being neutral equities and long fixed income. These funds also cut their long USD positions (especially against the EUR) during the summer. There are nonetheless discrepancies between the positioning of short term and long term CTAs. The former have less directionality in FX and commodity markets and appear to be better suited to capture any benefits from the new market regime. In fact, long term CTAs are still long USD and short commodities. The Fed’s stance is likely to put downward pressure on the USD and some upward pressure on commodities.

Meanwhile, discretionary Macro managers are also long fixed income and are set to benefit from the ease in bond yields following the downward revision of both the economic projections and the “Dot Plot” .

Finally, the Fed’s lack of guidance over future interest rate moves could result in higher risk aversion despite this dovish stance. In the L/S Equity space, we maintain our strong preference for market neutral and variable bias strategies. Some managers in that space have delivered double-digit returns year to date and we expect this trend to continue.

Philippe Ferreira , September 2015

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |