US dividend growth slows to post-crisis low

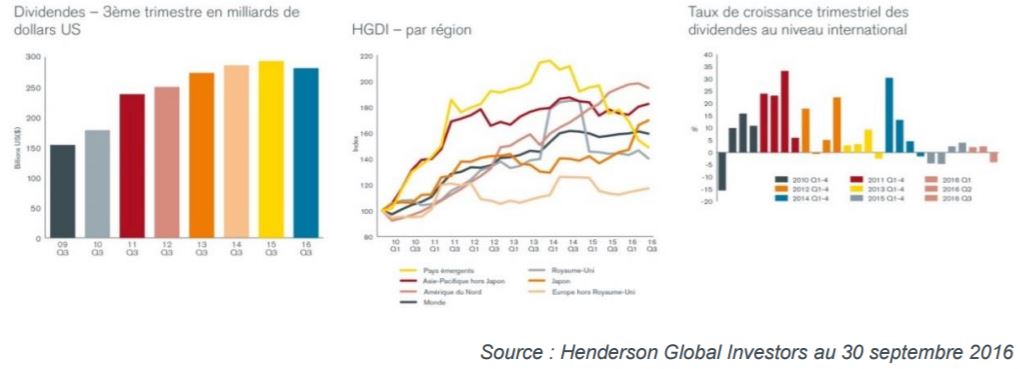

Global dividends fell to $281.7bn in the third quarter, down 4.0% year-on-year, according to the Henderson Global Dividend Index. Lower US special dividends made a significant impact to the headline rate, but underlying US dividend growth has also slowed...

Article also available in :

English ![]() |

français

|

français ![]()

This was the weakest performance since the second quarter of 2015. Three main factors are behind the decline. First, special payouts were lower, particularly in the US. Secondly, the third quarter sees a seasonal peak from areas of the world that currently have weaker dividend growth such as emerging markets, Australia, and the UK. And finally, dividend growth in the US has slowed. As the largest contributor to dividends, a slowdown here makes a significant impact. On an underlying basis, which adjusts for exchange rates, special dividends and other factors, the global total was 0.3% lower.

Key highlights

- Global dividends fell 4.0% in Q3 to $281.7bn, weakest performance since Q2 2015

- Lower US special dividends made a significant impact to the headline rate, but underlying US dividend growth has also slowed

- Seasonal shift to weaker areas of the world – China, Australia and UK

- On an underlying basis (adjusting for special dividends, exchange rates and other factors), dividends were 0.3% lower

- Henderson has slightly reduced 2016 dividend growth forecast to 0.9% in headline terms, and 1.0% in underlying terms

- Total global dividends for 2016 expected to be $1.16 trillion.

The US accounts for two fifths of global dividends, so trends here have a major impact. Payouts fell 7.0% to $100.4bn in Q3, mainly because very large special dividends paid in Q3 last year were not repeated. Even so, on an underlying basis, growth was just 3.0%, the slowest rate of US growth since the financial crisis, continuing a deceleration that began a little over a year ago. The slowdown follows more subdued profit growth in the US partly thanks to the strong dollar, but it also reflects higher indebtedness by US corporates, leading to greater caution about the deployment of cash flow.

Q3’s weakness also reflects seasonal peaks in areas of the world where dividend growth is currently weaker than elsewhere. These are Australia, China and other emerging markets, and the UK.

Australian companies pay the most dividends in Asia-Pacific ex Japan, and over two fifths of the country’s annual total lands in Q3. It was the weakest performer in the region, with the $18.2bn total down 6.9% in headline terms, despite a stronger currency. On an underlying basis Australian payouts declined 10.2% as BHP Billiton, the mining conglomerate, slashed its Q3 payout by over $2bn, with its smaller rival Rio Tinto following suit. Financials meanwhile are Australia’s largest dividend paying sector, accounting for three fifths of annual dividends. Bank dividends have so far been maintained despite concerns about the country’s extended credit boom and the possibility of further regulatory scrutiny on capital requirements. ANZ proved to be the exception with the new CEO making a modest dividend cut to help protect the bank’s capital ratios.

Emerging market dividends fell for the third consecutive quarter. At $42.9bn, they were 7.1% lower in headline terms, and 7.7% lower on an underlying basis. China is by far the largest emerging market payer, and dividends there are under pressure. 2016 is set to see the second consecutive annual Chinese decline. Chinese companies are reducing payout ratios, especially in the banking sector, which is seeking to protect balance sheets vulnerable to rising bad loans. For example, China Construction Bank, easily the world’s largest payer in the third quarter, sliced its dividend by $1.8bn to $10.0bn this year. Together, banks account for over 80% of Chinese dividends, explaining why the overall Chinese total was down 4.5% in headline terms to $24.6bn, a fall of 10.8% on an underlying basis.

Meanwhile, global investors in UK equities saw dividends decline 13.9% year-on-year in Q3 to $26.3bn, the steep fall mainly reflecting the devaluation of the pound following the UK vote to leave the European Union. In underlying terms, however, UK dividends were still down 2.9%, owing to deep cuts at large mining companies listed in the UK, such as Glencore, and from Rolls Royce. For a sterling based investor however, sterling weakness has provided a welcome boost to the level of UK dividend payments (given around 40% of UK dividends are paid in US dollars), helping to offset the impact of some of the cuts mentioned above.

Q3 is seasonally unimportant in Japan and Europe. The former saw continued rapid headline increases owing to the strong yen, but slow underlying growth as corporate profits were subdued. Europe remains on course for a strong year. Spain dominates Q3, and dividends there are weaker than among its European neighbours, so this disguised the continued strength elsewhere in the region.

Henderson has trimmed its forecast slightly for the full year, now expecting headline growth of 0.9% year-onyear, equivalent to underlying growth of 1.0%. It expects global dividends to total $1.16trillion.

Alex Crooke, Head of Global Equity Income at Henderson Global Investors said: “Global dividend growth has been lacklustre this year. The most significant trend is the reduction in US dividend growth, now at its slowest since the index started in 2009. However, we do not see this as a major cause for concern as US dividend growth had to return to a more sustainable rate after a couple of years of double-digit expansion. The United States has been the engine of global dividends in the last two years, so the slowdown here helps explain the loss of momentum in growth at the global level. A strong performance in Europe means underlying growth there may now exceed North America this year, although this has not been enough to offset greater-than-expected weakness elsewhere in the world, for example in China, Australia and the UK.”

“Our research shows just how dependent investors in some parts of the world are on a very narrow range of sectors, or on a small group of big companies, for their income. Moreover, exchange rate movements have been volatile lately. Consequently, taking a global approach to income reduces this risk and broadens the opportunities available, allowing investors to access stocks with attractive dividend growth prospects that may not be available in their local markets Past performance is no guarantee of future results. International investing involves certain risks and increased volatility not associated with investing solely in the UK. These risks included currency fluctuations, economic or financial instability, lack of timely or reliable financial information or unfavourable political or legal developments.”

Next Finance , November 2016

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |