Rating Agencies

The American case during August 2011 and that of France in January shows that the loss of an AAA rating does not necessarily lead to a higher interest rate adjustment.

Article also available in :

English ![]() |

français

|

français ![]()

After deciding to drop France?s rating from AAA to AA+, the agency Standard & Poor have reopened the debate on the role of rating agencies and their methods. This lead to a reconsideration of France?s financial situation and their budgetary perspectives. The lack of reaction from markets show that the rating as a formal exercise is of less importance to investors that suggests the debate on this question.

THE REASON FOR RATING AGENCIES

Rating agencies originated at the development of capital markets in the nineteenth century, due to a need for reliable information on investors when faced with company risk. There was a need to formalise and classify risk levels and agencies offered a solution to institutional investors. The same steps were taken with sovereign risks (States, local authorities) and later, with financial products (investment funds) as well as all types of financial instruments (commercial paper, structured products).

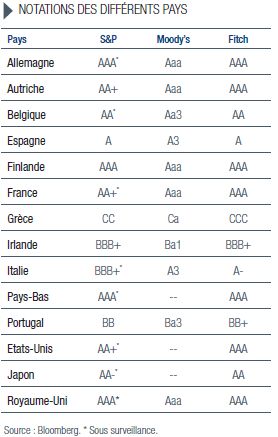

- Notations des différents pays

Today, there are big three western agencies: Standard & Poor?s (S&P), Moody?s and Fitch. S&P (McGraw-Hill group) is historically the first rating agency to have existed. Apart from its rating agency activities, the company also developed other products, namely exchange indexes (the S&P 500 index from 1941 to 1943). Moody?s was created in 1990 and Fitch Ratings in 1913 (owned by both the french company Fimalac and by Hearst). More recently (1994), China established the agency Dagong, with a formally private status. Specialised in quality evalutaion of Chinese borrowers (companies, local authorities), it developed its own methods in foreign sovereign credit. Besides long term ratings, the agencies provide an evaluation of perspectives (positive, stable or negative) on these ratings.

RECENT EVOLUTION OF AGENCIES IN EUROPE

For two years, agencies have lowered ratings of many countries of the eurozone. Not all were as significant as S&P (16 countries in January, by two or three points) and the different agency ratings are not regular. For example, neither Moody nor Fitch Ratings degraded the French rating, even if it was placed in a negative light by Moody?s. After these adjustments, at least on behalf of S&P, the last AAA signatures in the eurozone belonged to Germany, the Netherlands, Finland and Luxembourg. Outside the eurozone, Denmark, United Kingdom and Sweden conserve their AAA rating, Sweden?s case being entirely justified (no public deficit), but more disputed in that of the United Kingdom. The European Investment Bank also benefits from this rating. Apart from the States and international institutions (the EFSF lost its AAA), the European banks were the object of several rating downgrades.

THE MARKET HAS ITS OWN MODEL

Rating agencies sell their services to issuers but investors buy the securities and take the risk that they represent, thereby representing an asymmetrical situation. An insurer cannot neglect the opinion of the agencies, but his interest is to carry out his own risk evaluation and to do a critical work on the analyses of agencies. Those made for undeniable progress: their models are available and they have made communication efforts.

For a long time, investors showed that they generally do not await the conclusions of the agencies. However, inside the eurozone, the differentiation between the risk levels of the various States is definitely more recent. Until 2007, the existence of the single currency undoubtedly contributed to concealing the divergence of economic and financial evolutions. Variation regarding the compensation of German debt was practically non-existent.

Bond markets assure the financing of deficits, which is what the states depend upon. However, maintaining a certain rating would not waiver an objective in its own rights. An economic policy can turn to choices different from the precepts that agencies defend and instead, can stick to conventional financial principles. The current financial situation shows that the maximum rating is not a necessity for financing at a low rate: The United States, Japan and France prove this fact. The degradation of their rating to AA + (AA-for Japan) does not prevent them from benefiting from a weak debt cost.

AGENCIES HORIZON : A PROBLEM OF COHERENCE

If the main goal of agencies is to measure the risk of non-reimbursement of a bond, is it based on a vision and an analysis that favours mainly short term data?

The anticipation capacities of quantitative models raise questions of principle and method. Indeed, past cases show a weak degree of reliability in the forecast. For example, numerous ratings of the American financial instruments which integrated a mortgage credit as underlying instument (CDO, Collaterized Debt Obligations) were still at the maximum level while the real estate market already showed signs of weakening. The later adjustment of these ratings is not a particularly positive testimony of the analysis qualities of agencies and their reactivity. Furthermore, issuers of these instruments in question compensate agencies for their services. The risk of conflicts of interests often fell away. From the point of view of sovereign risk, the legitimacy of agencies hypotheses also stirs up numerous questions concerning their method. Apart from some conventional financial principles that are indisputable, the logic of the economic mechanisms is restricted because it seems dominated by immediate variables. The quantitative approach has its limits, already widely demonstrated in microeconomic material, and this includes the case of rating agencies. To measure the cash flow of a company, to analyze the evolution of a balance sheet, to apply ratios of diverse natures (operational, structural) in a projected perspective, already represent a complex and difficult task, but the modeling of the economic situation of a country in its dynamic nature is a complexity of another level. In the case of the drop in the United States rating in August, 2011, S&P especially called upon the genuine paralysis of the political process, to justify its decision. Concerning the market and investors, agencies have a double responsibility. Making a decision on a long-term reality which includes very heterogeneous variables (financial, economic, political, social) causes numerous difficulties. Despite their financial means, institutions as prestigious as the IMF or OECD have difficulty in correctly anticipating the economic evolution.

SOVEREIGN DEBT: THE PRINCIPLE ROLE AND THE CONTRADICTORY REQUIREMENTS OF AGENCIES

The decisions of agencies can be questionable, and are certainly disputed, but the justifications offered and the variation in arguments can too cause difficulties. For example, the successive judgments expressed by Moody?s on Spain alternated between an analysis centered on the budgetary questions and the necessary reduction of deficit; stating that economic growth was insufficient. It escapes nobody that the peripheral countries of the eurozone are confronted with the problem of supplying a budgetary effort which does not excessively penalize economic growth. The considerations can also be of an exclusively qualitative nature, as those of S&P in January when doubts on the efficiency of the European Central Bank policy were evoked. Here, opinion replaces quantitative analysis.

The decisions of agencies are problematic as they play an amplifying role: the degradation of Italy?s rating repeatedly caused an increase in interest rates, every time worsening the country?s situation because of its heavy debt responsibility.

THE AMBIGUOUS POSITION OF THE REGULATOR

It is reassuring for a regulator to have an analysis source outside institutions that are in charge of fund investment. Whether it?s investment in insurance or about careful rules applying to pension funds, the idea to subcontract the work of objectively estimating the most important risk (namely non-reimbursement) to independent specialists, is attractive. It is just as attractive for a central Bank when it comes to its own rules of bond repurchase.

By legitimizing the judgment of agencies, the regulator relinquished a central role in the functioning of the management. After a rating change, the prudential maximums established by the regulatory authority, for certain debt categories, are forced to be sold due to an overtaking. Reference elements of management and bond indications also contribute to these mechanisms because they are based on the coherence of the quality of the represented debts. The degradation of just one of them causes it to be excluded from the index and urges the investors to withdraw.

The theoretical advantage is therefore the practical compensation of increasing market evolution. Every time there is a drop in the ratings (for minimum quality thresholds defined by the regulator, a second rating can be required), it feeds the sales of holders. It worsens the pressure in the increase of rates on the market and makes the situation more difficult. Moreover, the traditional investors (insurers, pension funds, funds) are not the only players on the bond market; they were joined by hedge funds. Intervention techniques also widened: futures and Credit Default Swaps (CDS) are hedging instruments, which can both worsen and accelerate exchange rate movements. The debates around agencies in Europe lead to the suggestion of restricting their activity. The European Commission considers this suggestion but still has not given a ruling on new methods. Agencies need specific approval but the question concerns more the nature of their interventions. The possibility of a European agency was evoked, intended to compensate for the dominant presence of the Anglo-Saxon agencies. The know-how exists in Europe but the ECB dismissed such a possibility. A private initiative, a foundation (paid by the investors and not by the issuers) is the present focus of study.

FRANCE?S SITUATION

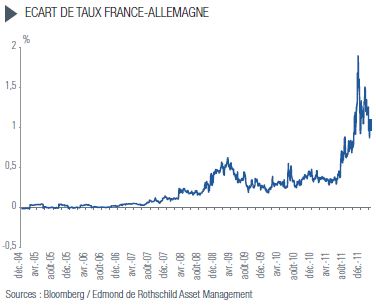

Strictly speaking, the drop in the French rating was not unexpected and the evolution of the bond market showed a growing difference between German rates and French rate. In terms of basis points, the difference in compensation amounted to 40 points in June 2011 and gradually tightened to peak at about 200 in November. It came down again in February, 2012 below 100. Nevertheless France has very favorable financing conditions (3,0 % in 10 years). In terms of GDP percentage, the budget deficit (close to 5,5 %) as well as France?s debt (90 % estimated at end of 2012) no longer deserved a triple A rating. In a way, the loss of the triple A can cause a healthy shock and encourage a real recovery effort of French public finances. Budget management was the object of criticism for a long time on behalf of the revenue court. The core of the criticism was the fact that public spending represented a strong proportion of the GDP (45 %, France being classified second after Denmark) and that the need for financing by the debt was the compensation of operational expenses. Budgetary orthodoxy can allow a deficit in accordance with public investments, but this was not the case in France.

The deterioration of public finances is long established but it worsened during the crisis of 2007-2008 due to the drop in activity (reduction in fiscal receipts) and state interventions. Progress was already made in 2011 (1,6 percentage point reduction in terms of GDP compared to the 7,1 % deficit of 2010) but this should be maintained. In spite of the State?s levy rate on the GDP, improvement is especially a question of political courage. The investors will judge the consistency shown by French authorities in the implementation of a plausible program, which would combine public spending cuts and an increase in taxes.

- Ecart de Taux France-Allemagne

CONCLUSION

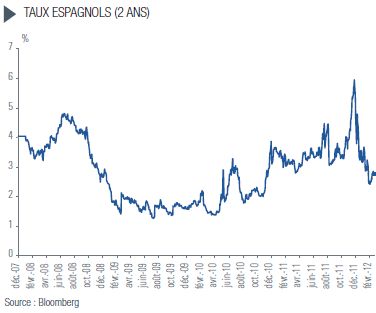

The American example of August 2011 shows, as that of France in January, that the loss of a AAA rating does necessarily lead to a higher interest rate adjustment. For the United States, the long-term rates even fell in the weeks following S&P?s decision and they remain low. For Europe, the downgrading of ratings decided by S&P in mid-January did not stop the the Spanish debt rate nor the Italian debt rate to fall considerably (both degraded by two points, to A and to BBB + respectively), than it is about rates in ten years or, especially, about rates in two years (fallen from more than 6 % to 3 % for Spain).

- Taux Espagnols 2 ans

These movements are as much the consequence of the past pessimism as they are decisions of the ECB in liquidity and in direct support for the banking financing. Both medium-term operations of the ECB (LTRO of 36 months) allow the banks to face their next failures resulting from past actions. The systematic risk is therefore, considerably reduced in Europe. The relaxation of the interest rates also reflects the awareness that real progress is being made from the point of view of the budgetary policies in the eurozone. However, the sovereign debt crisis in eurozone has not yet come to an end. The problem of the Greek debt has not yet been solved either. Portugal and Ireland also remain in great difficulty. Nevertheless, there is increased awareness from the government and genuine programs are in the progress of development. Institutions intended to help countries in trouble, after many deadlines can finally be implemented from an operational point of view. The European Stability Mechanism planned in 2013 must come into force on July 1st 2012, this comes with indisputable advantages regarding the EFSF, which to this day, cannot fulfill its intended role. The ESM is a European institution with a capital of 80 billion euros (comparable to the EIB) of which only a certain part will be used initially. It is able to to carry out distributions on the market (it has a 500 billion euro envelope). The European budgetary coherence will be strengthened by the agreement to come in March 2012, the financial aid plan to help the eurozone will be confirmed by the treaty, complementing the European institutions. These stages will not be without political will and certain consent is far from being obtained (only 12 accords are necessary) but they will bring about stability and credibility.

Pierre Ciret , March 2012

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |