On the impact of Brexit on sterling

As yet, sterling appears not to have reacted to the looming referendum on the UK’s continued membership of the European Union. Over the short to medium term, however, the currency should end up reacting negatively, so great is the fallout for the British economy. In particular, one would expect the volatility displayed by sterling to pick up at the start of 2016, bearing in mind that opinion polls are very tight...

Article also available in :

English ![]() |

français

|

français ![]()

As yet, sterling appears not to have reacted to the looming referendum on the UK’s continued membership of the European Union. Over the short to medium term, however, the currency should end up reacting negatively, so great is the fallout for the British economy. In particular, one would expect the volatility displayed by sterling to pick up at the start of 2016, bearing in mind that opinion polls are very tight. Before considering the effects of the referendum on the British currency, we set out the context, the reforms proposed by the British government, key dates, and, especially, the possible impact on the British economy.

In reaction to the emergence of the UK Independence Party (UKIP), David Cameron decided in January 2013 to hold an In/Out Referendum to preserve the unity of the Conservative Party. Since the creation of the European Union, the UK has been a rather reluctant partner, opting out of the single currency and the Schengen agreement. The sovereign debt crisis and the influx of migrants have revived the debate over the UK’s continued EU membership. A referendum should be held before the end of 2017. It is very likely that it will be held in Q3 2016, not in 2017 as there are general elections in France and Germany.

So far, David Cameron has written a letter to the European Council President setting out proposed reforms requiring the EU to change its founding treaties. If there is agreement over the proposed reforms, the British Prime Minister indicated in the letter that he was ready to campaign for continued EU membership.

There are four main areas where the UK is seeking reform:

1. Economic governance: David Cameron wants recognition that the EU has more than one currency. He also wants Euro-outs to have a say in developments within the Eurozone that affect all Member States, so as to preserve the positions of Euro-outs within the EU.

2. Competitiveness: the British Prime Minister is seeking a scaling back of unnecessary legislation to improve the competitiveness of EU Member States. He also proposes adopting a new trade strategy, including unfettered trade deals with the US, China, Japan and ASEAN.

3. Sovereignty: David Cameron wants to end the UK’s obligation to work towards an “ever closer union” as set out in the Rome Treaty. He wants to enhance the role of national parliaments, notably with a new arrangement whereby groups of national parliaments, acting together, can stop unwanted legislative proposals at EU level.

4. Immigration: the Prime Minister’s priority is to introduce a 4-year restriction on access to in-work benefits in the case of people coming to the UK from the EU.

Following the announcement of these proposals, a number of members of the European Commission have already said that certain reforms were “highly problematic”, which suggests that negotiations will be tough at the December meeting of the European Council.

Key dates and timetable:

The cost of a British exit on the British economy is still uncertain. The risk is that foreign investors and British enterprises would face a prolonged period of uncertainty, which could be very costly. An erosion in investor and business confidence would lead to a significant fall in investment. The impact on trade exchanges would be considerable. The European Union is the UK’s biggest trade partner, accounting for 45% of exports and 53% of imports. If the Out campaign prevails, the country would be excluded from the trade agreement with the EU. The WTO could impose customs duties on British goods and services, significantly increasing cost of trade. At employment level, a British exit would make the UK less attractive for migrants. The UK labour market would therefore be deprived of a significant source of labour supply. The existence of an abundant workforce because of the migrants has contributed to holding back wage growth and inflation. This situation has checked the rise in salaries in recent years, hence in inflation.

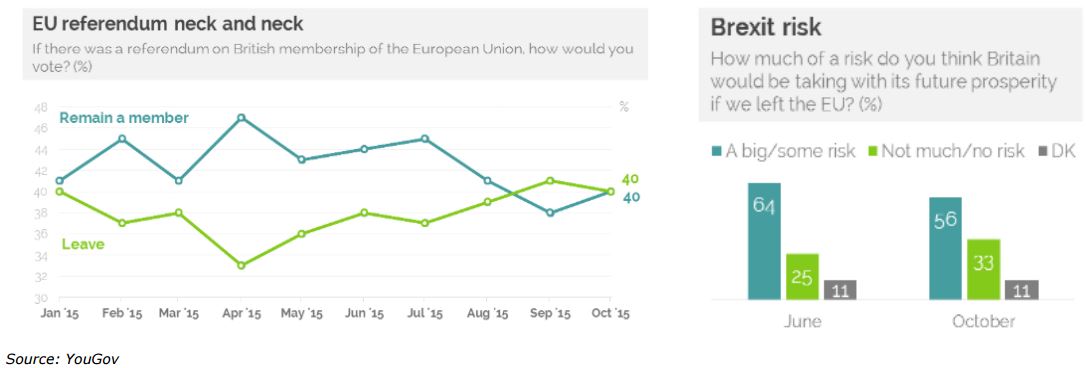

Since September, the probability of a UK exit from the European Union has increased according to

opinion polls, but without this having a significant impact on sterling.

Whatever the outcome of the referendum, it will affect sterling. If there is a British exit, there will follow a period of uncertainty for investors (impact on 1-year volatility). Although not entirely similar, the referendum on Scottish independence saw sterling slump by 4%, but not before the fortnight preceding the vote. This time, however, the effects will be felt far earlier when it comes to the British economy and currency as fallouts would be greater, possibly leading to a breakup of the UK, if Scotland opts to stay in the European Union.

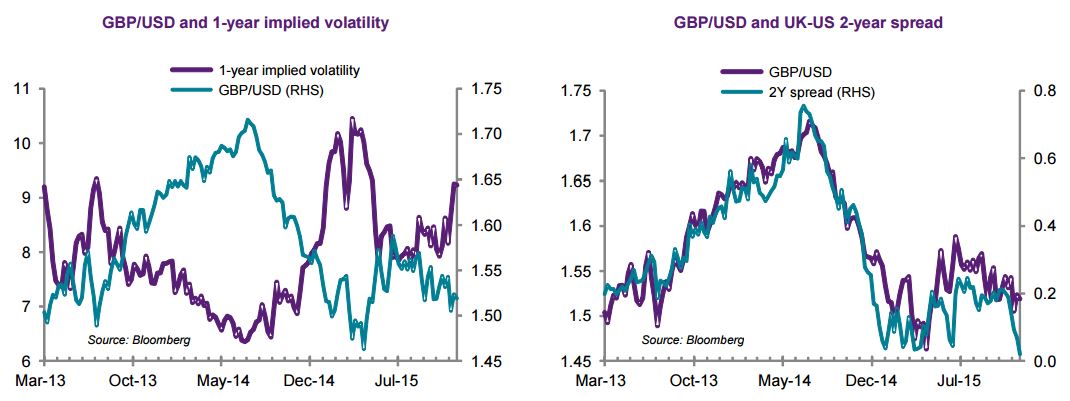

Our view is that the UK will vote to remain in the European Union. However, sterling will be under pressure throughout H1 2016, particularly if the polls remain tight, as this would stoke uncertainties, hence capital outflows. The GBP/USD could correct to 1.46 in H1 2016, which suggests that 1-year RR 25D also have downside potential in the short term.

They currently stand at -1.69 compared with -2.89 in March 2015. Sterling will not recover until the end of 2016, heading towards 1.52 post-referendum, with the help of the Bank of England, which can be expected to kick start its monetary tightening in reaction to the expected rebound in inflation (disappearance of base effects). In coming months, we expect 1- and 2-year implied volatility to pick up because of the uncertainties over the outcome of the In/Out referendum that could be held end-2016, or possibly in 2017.

If voters reject a British exit by a large majority, the GBP/USD’s rebound will be more substantial, the pair heading towards 1.55, inasmuch as this would strengthen the UK’s position in the European Union and amongst investors. If the vote is for a British exit, the GBP/USD will correct further given uncertainties over trade relations as well as at economic and political levels. If this scenario unfolds, the GBP/USD could pull back post-referendum towards 1.40 at the end of 2016.

Nordine Naam , Victoire Rougnon , November 2015

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |