| https://www.next-finance.net/en | |

|

Strategy

|

Who is still bullish on equities?

After a glorious and rather calm summer, characterised by a broad-based rally by risky assets, range trading by govies and declines in risk perception and volatility, which we examined last week, we now propose to run through the exposure of the main categories of institutional investors. Did they surf on the August wave?

Article also available in :

English ![]() |

français

|

français ![]()

After a glorious and rather calm summer, characterised by a broad-based rally by risky assets, range trading by govies and declines in risk perception and volatility, which we examined last week, we now propose to run through the exposure of the main categories of institutional investors. Did they surf on the August wave?

As before, we consider below the positioning of the main categories of institutional investors:

- Flexible funds (i.e. long-only mutual funds), whose strategy is based on allocations between equities, bond and credit. We use a sample composed of the largest US funds.

- Hedge funds (long/short with leverage), for which we use as a proxy investable indices bringing together the most liquid hedge funds (in most cases available through managed accounts or in the form of UCITS). Rather than the HFRX Global index, we opted for the Long Short Equities and Event Driven indices, as these two strategies are essentially invested in equities with variable long biases and account for over half the hedge fund universe.

- Risk parity funds are long-only diversified funds for which asset allocation is defined systematically to divide the risk equally across the entire investment portfolio. These strategies use leverage. For this category, we use a sample of the largest funds.

- CTA funds, which are trend followers, invest nearly exclusively in futures in all markets (money market instruments, bonds, equities, forex, commodities) and seek to capture price trends for these assets. We use as a proxy of their performance an investable index, the HFRX Systematic Diversified CTA, which brings together funds with systematic long/short strategies moving average type, etc.

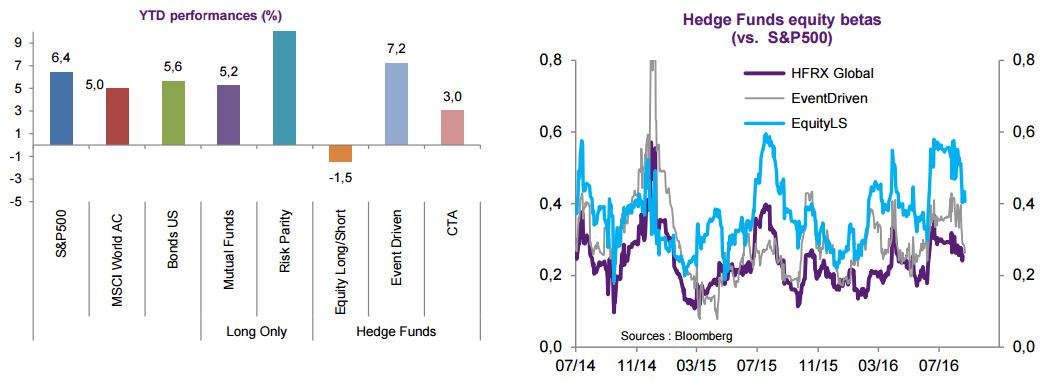

We consider first the performance of hedge funds, which once again was disappointing (+1.1% for the HFRX Global index, -1.5% for long short equity strategies). The chart below shows that Long Short Equities and Event Driven strategies (around 50% of hedge funds) started increasing their exposure to equities at the start of June, i.e. pre-Brexit, and that they did not reduce their risk exposure post-Brexit.

In fact, risk exposures by Long Short Equities and Event Driven strategies even set two-year highs during August, with equity betas of almost 0.6 and 0.4, respectively. Since mid-August, however, equity exposures have been trimmed, but they nonetheless remain significant.

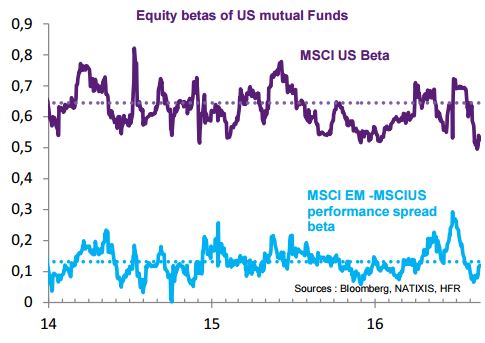

As regards flexible funds, the momentum has been different, denoted by a markedly more cautious behaviour. The funds in our sample started to trim their exposure back in mid-July, which has now declined significantly below its long-run average (0.5 compared with 0.65 on average).

It will also be observed that exposure to emerging indices has been lower. Their follows that the sensitivity to fluctuations in the performances of emerging equities and US equities (proxy for their exposure to emerging markets) have reverted to being neutral after peaking just before the British referendum on 22 June.

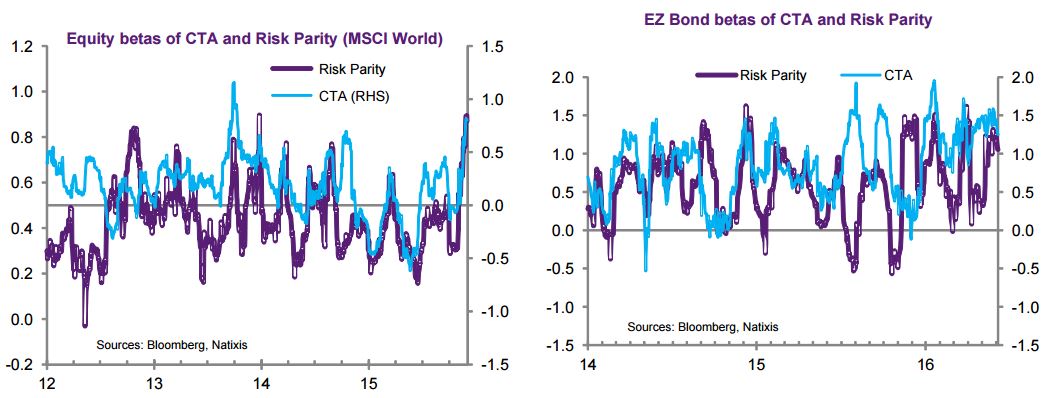

Finally, Risk Parity and CTA funds have increased their equity exposures since the start of July.

This is perfectly understandable in the case of CTA funds since equity indices have trended upward over the period. Likewise for Risk Parity funds, but because volatility displayed by equity indices has subsided: given their systematic (or well-nigh systematic) investment rules, these funds tend to increase (decrease) their exposure to assets when risks (volatility) decrease (increase). There remains that for both these categories of funds, the level of their exposure appears high by past standards based on our estimates. Much the same can be said of the exposure of these investors to Eurozone bonds, which are also near more than two-year highs.

All in all therefore, investor behaviours have been mixed. Systematic funds, which are naturally gamma positive, have logically surfed on the upward wave enjoyed by equities (and Eurozone bonds) and now have significant exposure. Hedge funds, whose performances have trailed since the start of the year, seem to be running after the market, hardly reducing their exposures. By contrast, the behaviour of flexible funds has been far more cautious.

With risk perception at a very low ebb and significant exposures by past standards for certain institutional investors, this means that the risk of a correction in the near term cannot be ruled out. In other words, the return to work could be eventful!

Florent Pochon , August 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |