| https://www.next-finance.net/en | |

|

Strategy

|

Which assets will be on a roll until May?

Our recommendations proceed from three factors, which are that macroeconomic risks (US cycle, Chinese cycle, upturn in crude prices to around USD 40/bbl) will subside in the short term, that QE will be ramped up by the ECB (from EUR 60bn to EUR 80bn) and, finally, the risk of a British exit (23 June referendum).

We recommend adopting a tactical positioning until the end of May in favour of the assets most susceptible of benefiting from the first two factors, namely bonds and credit, until the end of May, which is when the ECB’s CSPP will kick in, and ahead of the British referendum (see Multi-asset allocation for Q2 2016).

The EUR 20bn increase in the ECB’s QE should continue to have positive effects on bonds in the short term.

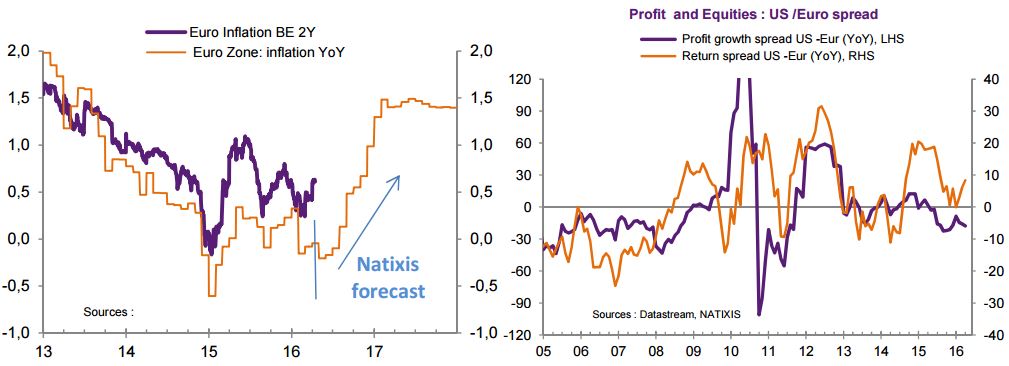

Sovereign and quasi-sovereign bonds will, initially, be the only asset class to benefit from the EUR 20bn increase in monthly purchases by the European Central Bank (ECB), as the universe of eligible bonds will only be expanded in June. The imbalance between supply and demand will therefore intensify, especially since there will be significant redemptions over this period). We are therefore positive on long duration Eurozone bonds for both the core and peripheral segments.

We have also turned positive on bonds indexed to Eurozone inflation: given our scenario for crude prices, with base effects expected to drive up price indices in the Eurozone and with risks tilted on the upside over the medium term, Eurozone short breakevens do seem rather low.

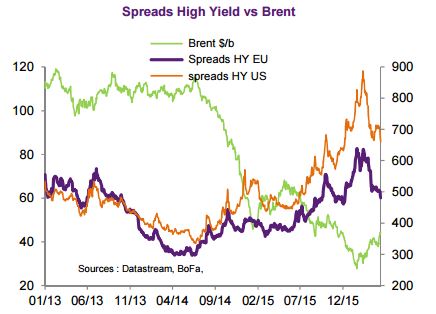

Credit next. On the one hand, the stabilisation of crude prices is positive for US credit, especially for US High Yield. While the US default rate for the US HY may be rising more rapidly than expected (from 2.9% to 3.6% in February, expected to reached 5.4% end-2016 according to Moody’s), this phenomenon remains confined, as yet, to the energy sector. On the other hand, with the ECB’s Corporate Sector Purchase Programme (CSPP) set to get under way at the start of June, this should pave the way for a further tightening of spreads and stimulate the primary market. However, bear in mind that for similar programmes involving purchases of non-sovereign bonds, spreads widened when purchases actually got under way. We are therefore positive on euro and dollar IG and HY until the end of May. By contrast, we are negative on Eurozone financials as we expected them to report disappointing earnings.

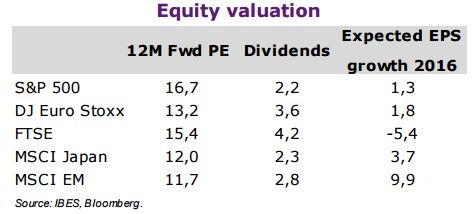

As regards equities, we remain positive on European markets in relation to their US counterparts on several counts: the more favourable monetary cycle (QE extension vs. monetary tightening), the more attractive valuation in P/E terms, the lag in the earnings cycle this side of the Atlantic, and the more generous dividend yields synonymous with a higher carry (see table below).

Further out, the US earnings cycle remains problematic with decreases of 11.5% year-on-year and 7.8% quarter-onquarter recorded by US corporates in Q4 2015. As yet, however, the earnings downturn remains confined to the energy sector, which is reeling from the fall in energy prices, and prospects are that this downturn will lose in intensity given our scenario of an upturn in crude prices. At the same time, the lesser productivity observed in the US will end up affecting margins achieved by US corporates (currently high by past standards) and hence net margins. With dividend yields on low at 2%, significant debt-financed share buybacks, a sharp rise in valuation multiples in recent years and what is expected to be weaker earnings growth going forward, the outlook looks limited as regards returns for US equities. Under these conditions, it does not seem anecdotic that the outperformance by US equities has been timed outside earnings reporting seasons (which started on 11 April for Q1 earnings).

We propose, for tactical reasons, moving back into emerging equities to profit from the favourable momentum in the short term.

As regards commodities, we remain neutral short term on crude, but are overweight industrial metals on account of the economic recovery in China, this country being the largest consumer in the world.

As for gold, the precious metal is expected to underperform in our baseline scenario (notably if there is an interest rate hike in the US), but will offer protection should there be a spike in risk aversion and/or a British exit, so our view is that this asset has its place in a diversified portfolio.

Emilie Tétard , Florent Pochon , Nathalie Dezeure , April 2016

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |