| https://www.next-finance.net/en | |

|

Opinion

|

Value in a Post-Brexit World

Richard Turnill, BlackRock’s Global Chief Investment Strategist discusses how the British vote to exit the EU has spurred a flight to safety, potentially creating opportunities. According to its commentary, with most asset valuations looking fair to expensive, however, it’s important to focus on relative valuations.

Key points

- Indiscriminate selling after the U.K. Brexit vote may create opportunities in assets with positive fundamentals and relative value (such as quality and dividend-growth stocks).

- The U.K.’s shock decision pummeled global risk assets and the British pound, and buoyed safe-haven assets.

- We expect economic data this week to show poor U.S. jobs growth in May wasn’t a harbinger of a U.S. recession.

A British vote to exit the European Union (EU) has spurred a flight to safety, potentially creating opportunities. With most asset valuations looking fair to expensive, however, it’s important to focus on relative valuations.

Chart of the week

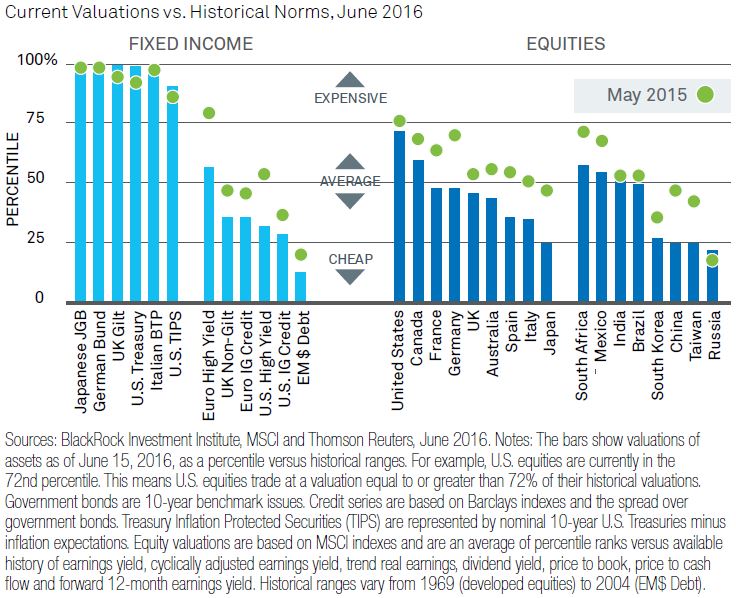

Prior to Brexit, there was a wide range of valuations but few cheap assets

globally, as shown above. Modest economic growth, low inflation expectations

and easy central bank policies have sent yields lower, intensifying flows into

income-oriented assets. This partly explains acute valuation differences

between equities and government bonds. Political concerns in Europe have

exacerbated other extreme differences.

Prior to Brexit, there was a wide range of valuations but few cheap assets

globally, as shown above. Modest economic growth, low inflation expectations

and easy central bank policies have sent yields lower, intensifying flows into

income-oriented assets. This partly explains acute valuation differences

between equities and government bonds. Political concerns in Europe have

exacerbated other extreme differences.

Selectivity and caution are key

Valuations tell us little about short-term returns but can potentially shed light on medium-term returns. Starting valuations explain roughly 10% of U.S. equity market returns over the following year but 87% of returns over the next 10 years, according to our analysis back to 1998.

Valuations also show the risk of owning bonds (and bond proxies) could rise further, as market uncertainty and easy monetary policy potentially drive valuations of interest-rate-sensitive assets higher. Some assets may be cheap for a reason, reflecting structurally challenged businesses for instance.

The big takeaway for those seeking to buy into market weakness: Be wary of notionally cheap assets that face challenges (e.g., domestically focused European assets like U.K. real estate and European banks), and instead focus on assets with relatively attractive valuations and positive fundamental drivers, such as quality stocks, dividend-growth stocks and investment-grade bonds. Indiscriminate selling of risk assets could translate into buying opportunities in these assets, including in U.K.-listed stocks that benefit from pound depreciation (72% of FTSE 100 revenues are earned abroad). Bottom line: Post-Brexit, selectivity and caution are key.

Richard Turnill , June 2016

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |