| https://www.next-finance.net/en | |

|

Opinion

|

US yields break 3% threshold for the first time in four years

Yields on10-year US Treasuries temporarily broke through 3% last week to the highest level since early 2014. We expect rising US wage and price pressures, a more assertive Fed and a higher fiscal deficit to help yields ultimately pass this threshold on a more persistent basis.

With tailwinds from yields, the US dollar broke out to the stronger side of a tight trading range. Equities performed well, helped by reassuring earnings and easing tensions on the Korean peninsula. Japanese and European stocks outperformed a flat US market also thanks to the stronger USD.

This week’s Fed meeting will bring no rate change, but will be scrutinized for hawkish tweaks in the FOMC statement. Later on Friday, the US labor market report will likely confirm robust employment and wage growth for April.

Yields on 10-year US Treasuries temporarily broke through 3% mid last week just slightly shy of the 3.04% last seen in early 2014, before easing back towards end of the week. Strong labor market data (US jobless claims falling to a 48-year low) and rising wage pressures (employment costs rising by 2.7%yoy, the strongest pace since Q3 2009) added to concerns about an overheating US economy, even though core capital goods orders slipped 0.1% in March and February data were revised lower.

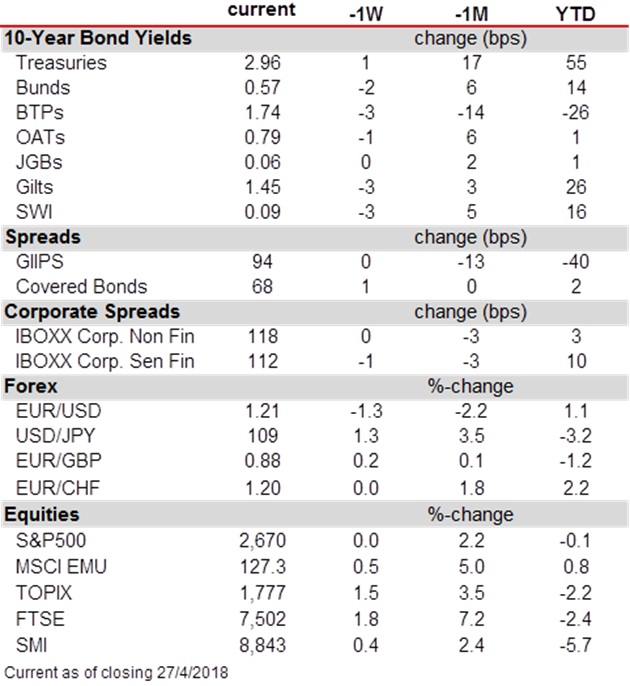

In Europe, Bund yields retreated slightly (10-year: -2bps to 0.57%). The ECB confirmed a ‘wait-and-see’ mode in its meeting last week, with President Draghi expressing some concerns about latest data weakness and risks from protectionism to business confidence. Defying a continued gridlock in Italian politics, the spread on 10-year Italian BTPs over Bunds remained below 120 bps. Benefitting from high US yields amid still stretched short speculative positions, the US dollar broke out to the stronger side of a tight trading range, with the EUR/USD ending the week close to 1.21. The stronger US dollar helped equities in Japan (Topix: +1.5%) and the euro area (MSCI EMU: +0.5%) to outperform a flat US S&P500 amid reassuring Q1 earnings reports and easing tensions on the Korean peninsula.

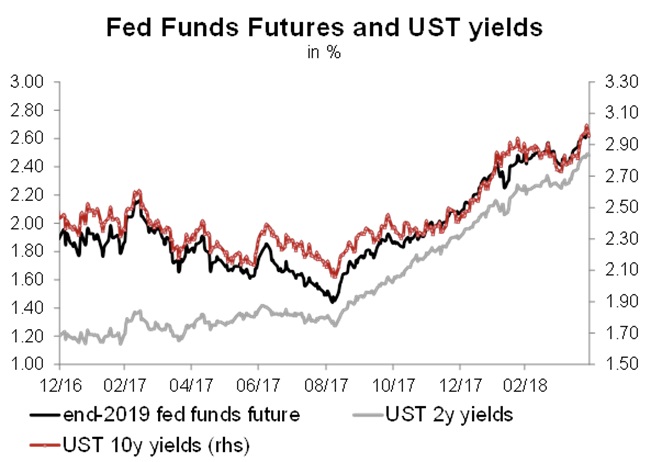

Markets have lifted expectations of Fed rate hikes, pushing up yields all along the curve. But the upside is not exhausted yet. 2-year rates are slightly below 2.50%, close to a 10-year high. Quarterly rate hikes by the Fed over the coming quarters will continue to push rates higher, though. But also yields on longer dated bonds may rise further, albeit moderately so. 10-year yields are closely tied to expectations about the Fed Funds Rate in the medium term (see chart). Markets price the peak in the Fed fund cycle at 2.75%, which is still at least 50bp too low compared to our own expectations. Rising oil prices and mounting wage pressures from a tight labor market will strengthen the case for more assertive monetary policy normalization. And while the Fed continues to gradually unwind its Treasury holdings, the fiscal deficit is set to increase. A more persistent break through the 3% threshold seems thus quite likely over the coming weeks.

This week, the Fed will take center stage. Rates will be left unchanged, but the FOMC statement may reveal a further hawkish twist amid recent evidence of mounting prices pressures. Today’s core PCE estimate for March will likely show an acceleration of the Fed’s preferred inflation gauge to 1.8% yoy. On Friday, we anticipate the labor market report to reveal healthy job gains for April of around 200k. In the euro area, by contrast, GDP estimates for Q1 (Wed) are about to show a growth deceleration to 0.3%qoq from 0.6% in Q4 2017. Flash inflation numbers for April (Thu) are unlikely to exhibit an increase from the 1.3%yoy posted for March, with higher energy prices balancing the effects from lower core inflation (muted activity, timing of Easter).

Thomas Hempell , April 2018

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |