| https://www.next-finance.net/en | |

|

Strategy

|

The ETF Inside Out experience

ETFs were designed to allow investors accessing broad indices while only trading into a single security, at low costs and with all protections inherent to collective investments. The reality is probably more complex...Analysis of Jean-René Giraud, founding C.E.O. Koris International

Article also available in :

English ![]() |

français

|

français ![]()

Using Exchange Traded Funds (ETFs) as building blocks for institutional portfolios is a reasonable approach that allows keeping the focus on the factor most determinant to investment returns: the asset allocation.

ETFs were designed to allow investors accessing broad indices while only trading into a single security, at low costs and with all protections inherent to collective investments.

The reality is probably more complex as, like any investment proposition, Exchange Traded Funds vary in shapes and forms, and the end result for the economic beneficiary largely depends on the replication quality delivered by the manager, the operational setup and obviously the costs and other frictions.

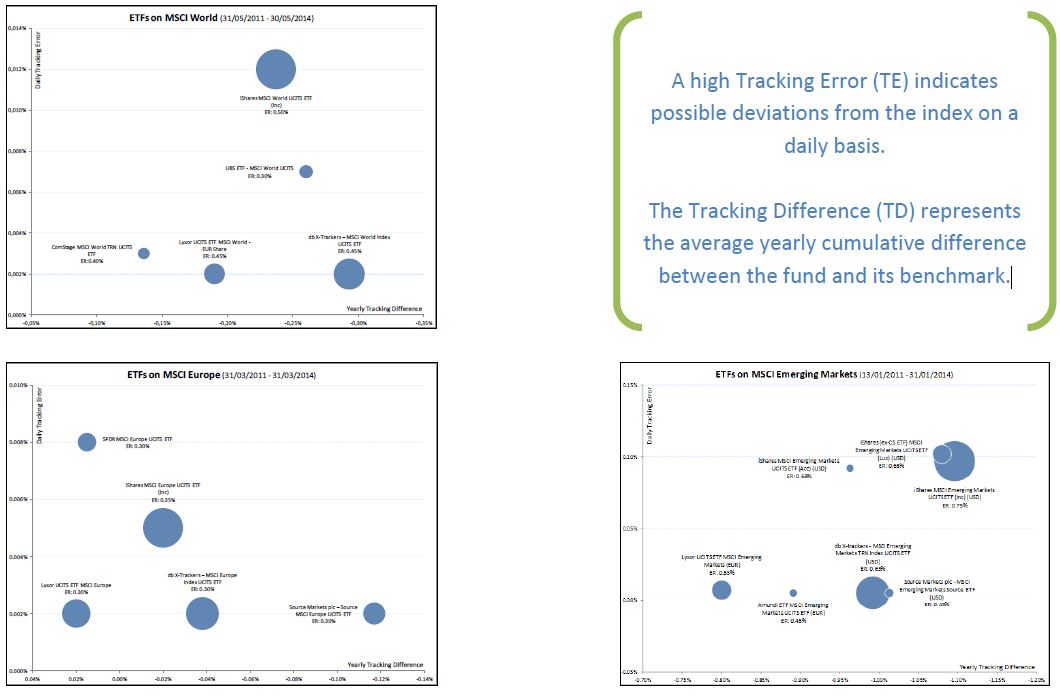

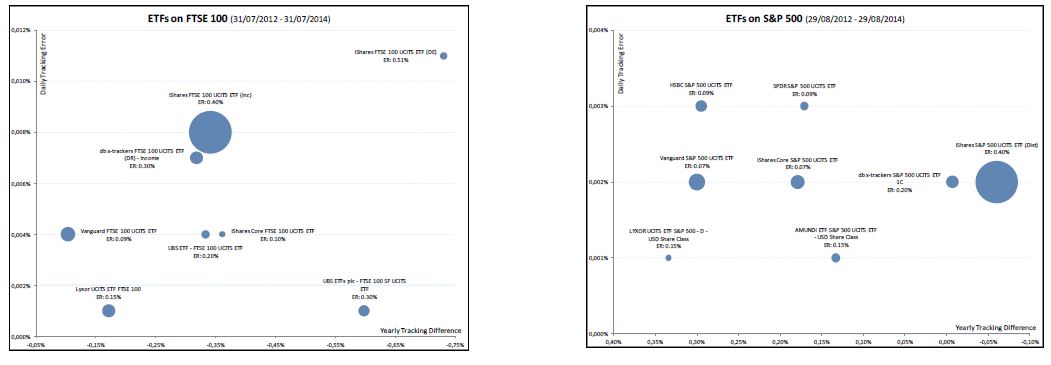

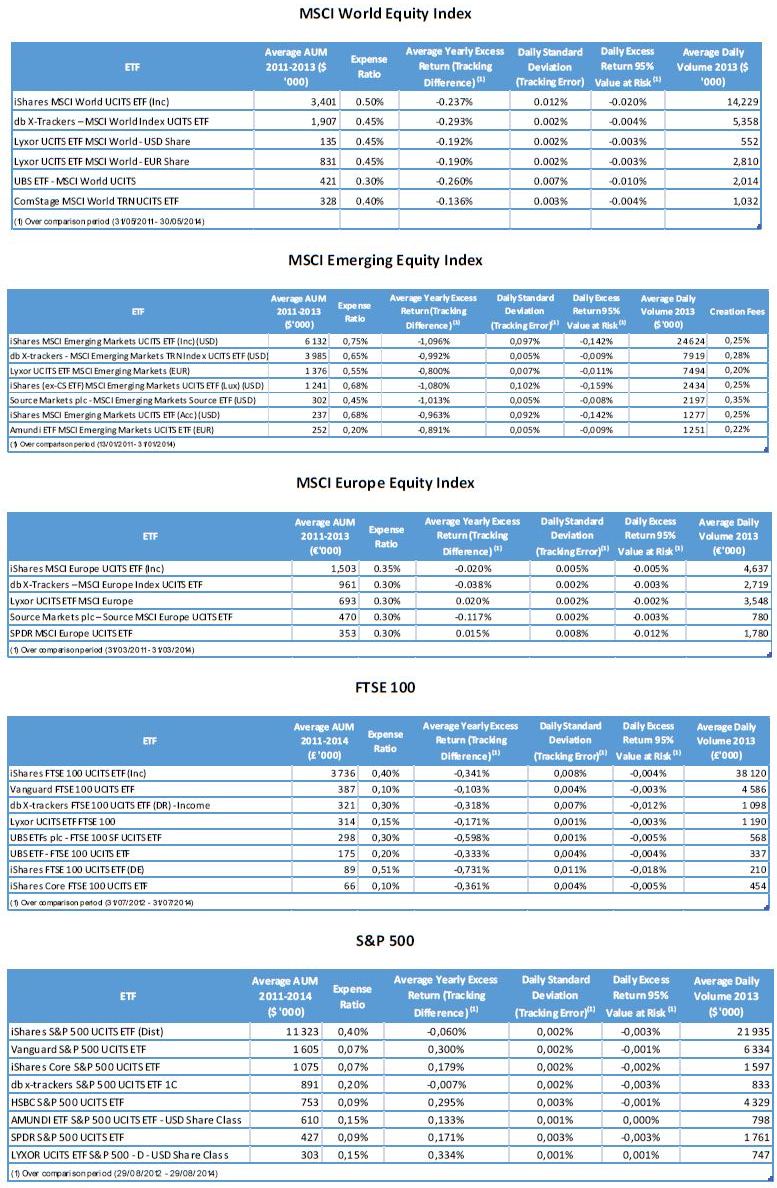

Every month, Koris International produces an in-depth analysis of the largest ETFs tracking a given index; the detailed review is then matched with what ETF providers have to say. The below graphs represent a 30,000 feet analysis over a three-year timeframe for the largest ETFs tracking the MSCI World, Emerging Markets and Europe indices and the two recognized indices S&P 500 and FTSE 100. Full analytical details and figures on other time periods are available on www.koris-intl.com/etf-inside-out for each index.

A high Tracking Error (TE) indicates possible deviations from the index on a daily basis.

The Tracking Difference (TD) represents the average yearly cumulative difference between the fund and its benchmark.

Our investigation in those five diverse equity indices enables us to draw a number of conclusions that institutional investors should carefully factor in when they address index and ETF selection during the portfolio construction phase.

- Know your index: understanding how an index is defined and rebalanced, how it deals with dividend distribution and the associated tax implications is an essential part before deciding to allocate to that universe. The development of smart beta products renders the task even more interesting … and challenging.

- Garbage in, garbage out: once more our team has faced considerable issues when consolidating data and information from publicly available sources, including professional data feeds. Incorrect Net Asset Values and out of date information on fund setup seems to be the norm in the industry which makes the selection process a painful task.

- Tracking difference an essential indicator: the absolute level provides you a very solid indication of the total costs of holding the instrument, while its stability over times will help investor assess the robustness of the investment process. We notice widespread differences amongst providers, and significant variation of the yearly tracking difference over the period of existence of the funds.

- Tracking Error to be looked at: the levels of daily tracking error vary significantly across the different providers and replication approaches, even when data has been thoroughly controlled ; we do however not see TE as an issue for mid and long term investors (which remain the norm in the institutional space). Still too high tracking error levels might induce unwanted risk at the time of trading the funds.

- Forget the physical vs. synthetic war: the reality is that any replication model has intrinsic risks that result in tracking error, tracking difference or counterparty risk. It is the role of the ETF manager to design optimal implementation schemes and organize the elements of precaution and protection to mitigate those risks. Investors should not base their decision on a broad model, rather understand what they buy and how the specific setup results in or mitigate unwanted investment risks.

- Total Expense is irrelevant: once more we did not manage to find any correlation between the level of fees put forward by the provider and the overall quality of the products, investors would be wise not to put any attention to that element as the total cost of ownership is what in the end drives portfolio performance relative to the benchmarks. In addition Total Expense only includes costs that are know ex-ante, while the TD (Tracking Difference) includes the real costs and frictions but can only be accounted for ex-post.

- Secondary market is not for institutions: average daily trading volumes that are seen on organized markets are simply not fit for institutional size-orders. Any investment above a €1mio cannot be absorbed by the market without resulting in adverse market impact, leaving the investor in the hands of authorized market participants in the search for available inventory or to organize a subscription into the ETF against the basket of underlying securities, with friction costs function of the liquidity of the underlying. The European market is in this sense very different from its US counterpart where secondary trading is a relevant and robust source of liquidity in the shares of ETFs.

We strongly believe ETFs are not born equal and investors should seriously assess ETF tracking quality before putting money in a given fund.

The reader may have noticed that no provider manages to consistently deliver in the top-quartile for all equity products, this is even more so when switching to other asset classes. The selection of an ETF should therefore really be based on a detailed analysis of the vehicle itself rather than on the due diligence of the management firm.

We really hope that the transparency brought to institutional investors in a systematic and unbiased way will definitively provide the appropriate incentive to industry participants to improve the replication quality and the overall cost structure imposed upon the end economic beneficiaries. Our experience in advising very large allocators to ETFs also leads us to believe that, beyond the pure performance and risk aspects of the ETFs themselves, more attention should be paid to the market structure in which they are negotiated and the way asset managers handle their execution flow in ETFs.

Here again, lack and inconsistency of data is leaving investors in a stormy fog. We are therefore adopting a very similar approach by aggregating and controlling data, then providing insight to end investors who in the end will base their allocations on tangible information.

Jean-René Giraud , November 2014

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |