Swiss Re’s insurance outlook for 2015 sees growth opportunities for insurers in a difficult environment

The global economy is expected to strengthen modestly next year, according to Swiss Re’s latest publication, "Global insurance review 2014 and outlook 2015/16". Non-life insurance premiums are expected to grow 2.8% in 2015, supported by strong economic activity in emerging markets...

The global economy is expected to strengthen modestly next year, according to Swiss Re’s latest publication, "Global insurance review 2014 and outlook 2015/16". Non-life insurance premiums are expected to grow 2.8% in 2015, supported by strong economic activity in emerging markets. The life insurance sector will be notably stronger in both the advanced and emerging markets, and global in-force premiums are forecast to increase by 4.8% this year and by around 4% in 2015 and 2016. The low yield environment remains a profitability challenge, in particular for life insurers.

Economic conditions support modest growth for insurers but investment returns will deteriorate

Global economic activity is expected to improve next year as growth rates increase in the US, the Euro area and many emerging markets. Other countries, such as the UK, Japan and China, will slow.

The US and UK are very likely to tighten monetary policy and raise their policy rates next year. The combination of growth and rising rates will push government bonds higher, particularly in the US and the UK. However, investment returns for re/insurers will continue to weaken because companies are expected to be rolling over maturing fixed income paper into lower yielding, more-recently released bonds.

"Stronger economic activity will improve insurance premium growth, particularly in the emerging markets," says Kurt Karl, Swiss Re Chief Economist. "But profitability will still be challenging because of the low investment yields."

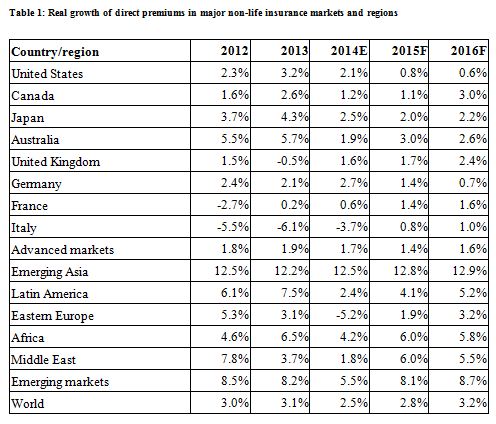

Non-life insurance premium growth driven by emerging markets

Overall emerging market non-life premium growth is forecast to return to around 8% next year and more in 2016, with Emerging Asia in the lead. Advanced markets premium growth slowed to 1.7% this year and will remain near that pace into 2016.

In casualty lines, loss ratio data from the US and UK indicate that reserve releases are unlikely to continue for long. This is a good indicator that pricing prospects are expected to improve over the next couple of years.

For reinsurers, premium growth is expected to be lower than in the primary non-life sector mostly due to reduced reinsurance buying in China and softening property catastrophe reinsurance rates. Catastrophe reinsurance pricing will likely remain under pressure at the 2015 renewals. Thereafter the pace of decreases is expected to slow down. Over the long term, demand for nat cat capacity is expected to continue to increase. For casualty and special lines, significant differences in pricing developments by market and line of business are expected. Aviation rates are expected to improve as the market reacts to recent loss activity.

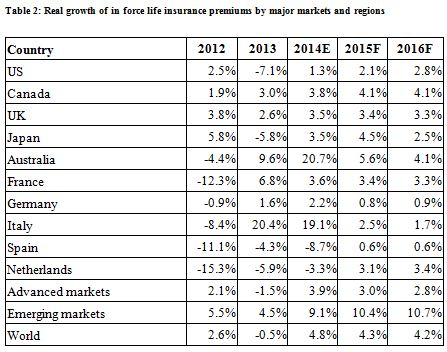

Life premiums recover as insurers find new ways to increase profitability

Premium growth of in-force life premiums in the advanced economies is expected to be nearly 4% this year and about 3% in 2015, rebounding from a 1.5% decline in 2013. Emerging market life premiums are forecast to grow 9% this year and 10% in 2015 after a sluggish 4.5% advance in 2013, driven again by a robust 13% premium growth in Emerging Asia.

Despite low investment returns, life re/insurers have improved profits over the last year with a RoE of about 12% up from 10% last year. This stems from their focus on new products, increased market penetration, improved distribution techniques and cost-cutting.

There have been stronger profits in the UK market, and also a pick up in North America and Continental Europe more recently. A key factor in new business growth in the major markets has been robust sales of savings products. Global real life reinsurance prem iums are expected to grow by less than 1% this year after shrinking 0.3% last year due to weakness in the advanced markets as the market adjusts to changing regulations in the US and UK.

In this environment, life reinsurers will seek non-traditional or less-developed areas of growth in the coming years, including taking over large blocks of business and providing major capital relief solutions. Life reinsurers are also providing solutions to take longevity risk from primary companies with annuity business. Momentum in this market remains strong and a record amount of longevity liabilities were transferred to reinsurers in 2014.

Next Finance , November 2014

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |