| https://www.next-finance.net/en | |

|

Opinion

|

So long, bond bull market

According to Jim Cielinski, Global Head of Fixed Income, Columbia Threadneedle, Key drivers shaping bond markets have changed. Keeping a global perspective and knowing which macro signals to watch for can help you prepare for changes in bond yields...

Article also available in :

English ![]() |

français

|

français ![]()

During an unprecedented period of political change across the globe, from the UK referendum on EU membership to the election of Donald Trump and the Italian Referendum, 2016 was a year where the key drivers shaping markets irrevocably changed.

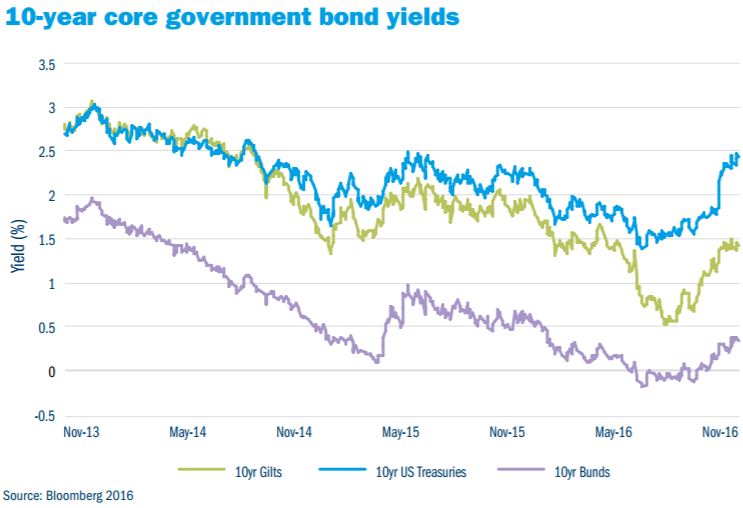

It was a year of two halves. The bond rally in the beginning of the year was bigger than expected, with deflationary pulses continuing to hit the market, reminding investors that geo-political risk was alive and well. This led to an impressive rally where, capped off by Brexit, ten-year gilt yields rallied from 2% at the beginning of the year to nearly 0.5% in July, before moving back to 1.5% at year-end.

In hindsight, the extra dose of post-Brexit quantitative easing looks increasingly like the last hurrah for monetary policy. The odds are high that the sell-off in the latter half of the year was an inflection point that marked the end of the long-running bull market in bonds, triggered by a combination of extreme over-valuations colliding with the expectation that the rules going forward will be different.

In our view, the bond-bubble was likely to burst, not because of a sudden acceleration in growth or inflation, but because a change in policy would change the rules and shatter the complacency. The world is slowly adjusting to the idea that monetary policy will transition to stimulative fiscal policy. Trump’s victory appeared an unlikely place for this trend to start, but it has set down a marker that will be difficult to contain.

The disenfranchised middle-class has voted – negative rates and quantitative easing are inadequate ways of raising their living standards. They want a new rule book. And if the current political establishment is unwilling to rewrite the rules, they will soon be voted out of office in favour of someone who will. For some time, markets have become accustomed to thinking that any disappointing data on growth and inflation would be met by lower rates or quantitative easing.

But these tools have been increasingly used as last-ditch efforts to spark economic growth. As we reach the end-game for monetary policy, there is now an acknowledgement that central banks soaking up a dwindling supply of bonds has a number of detrimental side effects. More spending and tax cuts appear to be the way forward, yet fiscal stimulus is inflationary. This would be negative for bonds in a normal environment. Coming from a bubble-like starting point, it’s even more ominous.

With the collapse of long-dated interest rates in mid-2016, bond markets had been pricing in little inflation risk for at least the next decade. But with the rule change we expect, term premia is likely to normalise and the idea that investors should price-in permanent disinflation will fade into obscurity. In that environment, a continued sell-off in bonds is likely.

The bond bubble is bursting. How spectacular will it be? That remains to be seen, as there are many deflationary forces still bubbling just beneath the surface.

If all of Trump’s agenda becomes law, the bear market will have much further to run. With this in mind, we believe investors should look out for three key signals that might tell us just how far bond yields might rise.

One: Inflation expectations

If fiscal stimulus becomes the policy lever of choice, we would expect an inflationary reaction. ‘Fiscal’ means more spending, which should boost growth as well as increasing deficits. Growth and inflation, if combined with deregulation (which we expect with a Trump presidency), spurs corporates to spend more and that can create a virtuous circle that’s very bond-negative. But inflationary expectations are also a function of wage pressures and trade protectionism. We’re at close to full employment in the US, and wage gains could start to push higher given that labour markets are tight and a high number of people that have left the workforce are not coming back. Wage pressures, along with fiscal stimulus and a more protectionist agenda (which is itself inflationary through trade tariffs and immigration), will see inflation expectations continue to rise from what are still depressed levels.

Two: China

China should be watched very closely. Longdated global rates reflect a decade-long series of capital outflows from China. The central bank has purchased hundreds of billions of foreign bonds. This bond-buying programme is a function of years of over-investment in plants and equipment, which itself led to overproduction and excess capacity. China’s capital outflows put immense downward pressure on global real rates and term premia.

China’s economy has been slowing. A savings glut, sluggish business investment and worries over potential devaluation in the yuan have all provided the impetus to move money offshore. But if the Chinese economy were to merely stabilise, it would provide yet another catalyst for bonds to sell off. A surprise reacceleration in China would force foreign flows to rapidly recede, leaving global government bonds without a key source of demand. Somewhat worrying is that there are some signs that this is happening, just as Donald Trump is set to enact some of his policy proposals, though this is something of a coincidence.

If fiscal stimulus becomes the policy lever of choice, we would expect an inflationary reaction.

Three: Europe and geo-politics

What happens in Europe, from a geo-political point of view, will be critical. In 2016, we have already seen the UK vote to leave the EU and the electorate reject the Italian prime minister Matteo Renzi’s referendum proposal. In 2017 we have elections in France and Germany, not to mention Article 50 being invoked.

A continued political shift to the right would imply that more populist policies will continue to be enacted. There are limits in Europe as to the scale of any tax cuts and increases in spending that can be delivered, because fiscal policy is limited by the Maastricht Treaty, which caps member state government deficits to 3% of GDP (and public debt levels to 60%). However, if populist parties who claim they will breach these rules are elected, this raises the risks surrounding the eurozone project. Ironically, in Europe, this is a recipe for higher rates overall, rather than lower rates.

Conclusion

The bond bubble is bursting. How spectacular will the sell-off be? That remains to be seen, as there are many deflationary forces still bubbling just beneath the surface, and a plethora of policy uncertainties. Trump will almost certainly succeed in getting tax cuts through and a scaled down version of his defence and infrastructure spending package passed. China is stabilising and with it comes less of a reliance on their easy monetary policy. Capital outflows will likely diminish as the yuan reprices and the powerful force of central bank buying – either through investment or QE channels – will recede. With respect to Europe, it is very difficult to forecast, but it would be wrong to extrapolate what happened in the UK with Brexit (as well as the election of Donald Trump and the Italian referendum). Nonetheless, the previously unthinkable is now possible.

We believe inflation expectations will continue to rise from what are still depressed levels. The US economy is near-full employment. Wage inflation coupled with even modest protectionism and the prolonged recovery should create elevated inflation expectations.

We envisage policy rates staying lower for some time in Europe as there is still enough uncertainty – not just geo-political risk, but also concerns over the strength of some economies in the region – for central banks to continue with a ‘lower for longer‘ policy. Rate rises are also unlikely in Japan, which leaves the US as something of a focal point. On the back of increasing wage pressures and fiscal spend, we expect rate hikes in 2017 to follow the December Fed hike. The tide has turned.

Jim Cielinski , February 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |