| https://www.next-finance.net/en | |

|

Opinion

|

Room to run for reflationary assets

Most reflation trades aren’t crowded or expensive, our research suggests. U.S. stock prices more fully reflect the maturing reflationary cycle, and we see better opportunities in Europe, Japan and EM stocks. We also prefer U.S. credit over government bonds.

“Trump trades” have run out of steam lately, amid growing market skepticism about the likelihood of significant near-term U.S. tax reform and infrastructure spending. Yet we believe the bigger-picture reflation trade has room to run.

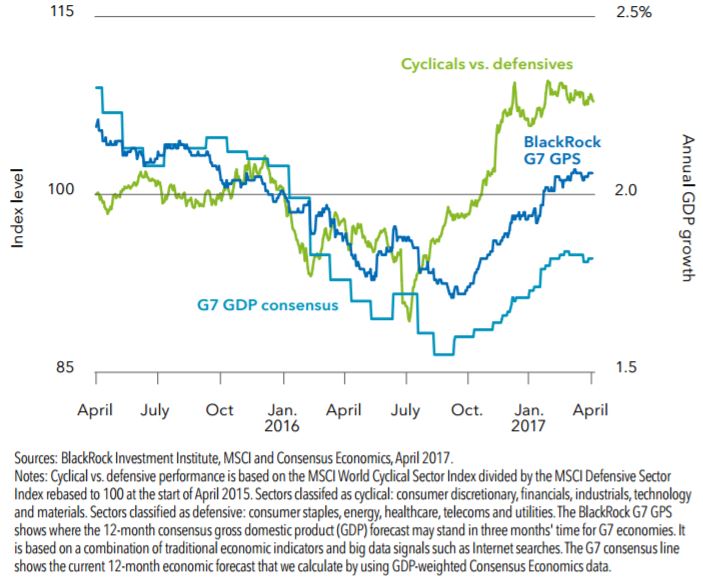

Cyclical vs. defensive equity sector performance and BlackRock GPS, 2015-2017

We are in the early stages of a global reflation cycle that started in mid-2016. The chart shows the better economic growth outlook reflected in our BlackRock GPS economic indicator relative to consensus views. The BlackRock GPS rise has coincided with the outperformance of cyclical shares geared to improving growth.

The big picture

Another sign reflation is going global in 2017: a synchronized pick-up in economic activity and corporate earnings. We define the reflation trade as favoring assets likely to benefit from rising growth and inflation, such as cyclical equities and emerging markets (EM), while limiting exposure to long-term government bonds. The reflation trade is not contingent on looser U.S. fiscal policy, in our view. Rather, tax reform or infrastructure spending could amplify it.

In the U.S., some reflation trades that experienced a post-election run-up as “Trump trades,” such as small caps and bank stocks, have underperformed this year amid waning expectations of a fiscal-boost. Bond market inflation expectations have also fallen lately back to December lows. Meanwhile, market segments with strong fundamentals that initially fell after the election, such as EM equities, have reversed. Political uncertainty may be holding back the reflation trade, but we see the macro environment ultimately mattering more. Consensus growth expectations have scope to rise further, even if the biggest gains may be behind us.

Most reflation trades aren’t crowded or expensive, our research suggests. U.S. stock prices more fully reflect the maturing reflationary cycle, and we see better opportunities in Europe, Japan and EM stocks. We also prefer U.S. credit over government bonds.

Richard Turnill , April 2017

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |