| https://www.next-finance.net/en | |

|

Opinion

|

Rethinking the role of Treasuries

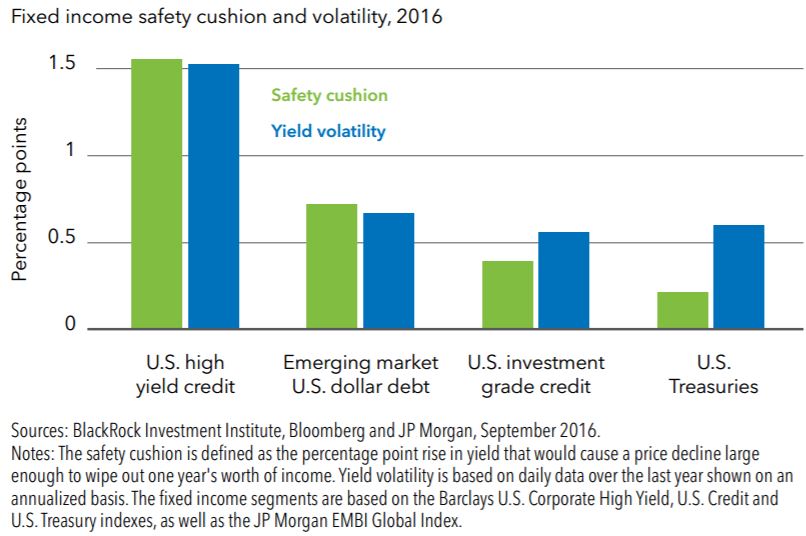

According to Richard Turnill, BlackRock’s Global Chief Investment Strategist, it’s time to rethink the role of U.S. Treasuries in portfolios, and specifically to be cautious of long-duration Treasuries. The risk-reward landscape for longduration Treasuries is shifting.

Depressed yields mean there is currently little safety cushion for holders of

U.S. government bonds. Just a 0.2 percentage point increase in Treasury

yields could wipe out a whole year’s worth of yield income.

Other fixed income sectors such as U.S. investment grade corporate bonds and emerging market dollar debt offer thicker safety cushions – with similar yield volatility in the past year. See the green and blue bars in the chart above.

Other fixed income sectors such as U.S. investment grade corporate bonds and emerging market dollar debt offer thicker safety cushions – with similar yield volatility in the past year. See the green and blue bars in the chart above.

A higher price for long-term insurance

The collapsing cushion comes as long-term yields are starting to rise. We see a steeper yield curve ahead amid a gradual pivot toward fiscal expansion globally, although central banks still have the ability to limit any unwanted yield rises. Major central banks are displaying a tolerance for letting inflation run hotter, and the Fed has adopted a go-slow approach to raising rates. Central banks appear to be approaching limits in the effectiveness of extraordinary monetary easing, as was evident in the BoJ’s shift last week to policy tools that steepen the local yield curve.

U.S. Treasuries are becoming less attractive to non-U.S. investors, as the increased cost of currency hedging is wiping out the extra yield Treasuries offer. Finally, bonds tend to have higher correlations to stocks during periods when markets are concerned about Fed tightening, damaging their traditional role as portfolio diversifiers. This is a risk as the central bank’s December meeting approaches.

Longer-maturity U.S. government bonds still have a role to play — and should buffer portfolios in any flights to safety. But investors today are paying a lot for this diversification benefit. We prefer shorter-term corporate and municipal bonds, whose yields have temporarily spiked ahead of U.S. money market reforms in October. Overall, we favor credit markets and see a role for other portfolio diversifiers such as gold.

Richard Turnill , October 2016

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |