| https://www.next-finance.net/en | |

|

Opinion

|

On debt watch: why China can’t save the world

As China faces up to its debt problems investors should be poised for turbulence and opportunity, writes Robin Parbrook, Head of Asia (ex Japan) Equities.

Article also available in :

English ![]() |

français

|

français ![]()

When European leaders appeared to go ‘cap in hand’ to China to help fund the eurozone bail-out, it marked a meaningful moment in world politics and further consolidated the shift in economic power from west to east.

While China may be the only country with sufficient cash reserves to help the eurozone out of its crisis, the world’s second largest economy has a debt problem of its own brewing and more than a few skeletons in its economic closet that put it in no fit state to save the world.

Having followed the Chinese economy for twenty years, I like to call its financial system the fifth dimension. The sector is veiled in such secrecy that no one knows the genuine state of China’s banks. In fact, analysts have largely come to accept that imagination must play a part in their valuation model! Aside from saving the world, China is itself at an economic crossroads that could serve to dismantle some of the systems that got the country into this mess.

In recent months, markets have finally woken up to the truth of the Fitch report on local government investment vehicles (LGIV). These are investment corporations set up by local governments which cannot borrow in their own name. During the course of the credit crunch, Chinese banks were encouraged to lend to these entities and these loans were used to fund the building boom that has left the country strewn with half-built bridges, unused buildings, broken railways, and tracts of land miles from anywhere. In addition, many of the loans have turned so bad they threaten the balance-sheets of the banks that made them.

Beijing has previously said that LGIVs have piled up to ¥10.7 trillion, ($1.6 trillion) as of the end of 2010, in debt. While our own estimates put this figure even higher, ¥10.7 trillion is still a lot of debt for the banking sector to bear. The government will almost certainly have to step in. Meanwhile, the market is also realising the scale of off-balance sheet lending in China.

Although cautious on China overall, we are still building positions in strong, transparent companies as the country’s long-term growth story hasn’t gone away”

Robin Parbrook

Robin Parbrook

It is clear that almost half of credit creation in China is off-balance sheet. The cause of this boom in shadow finance is

simple:

![]() strict on-balance sheet loan quotas

strict on-balance sheet loan quotas

![]() very negative deposit rates

very negative deposit rates

![]() very strong demand for credit

very strong demand for credit

![]() the banking sector’s desire for profit growth (fee income) at all costs

the banking sector’s desire for profit growth (fee income) at all costs

![]() and loose regulation

and loose regulation

All these have proved to be the perfect environment for-off balance sheet credit creation.

As the detail emerges – showing the extent of such lending; the practices involved; and the calibre of end borrowers (property companies, struggling Wenzhou SMEs etc.) – the horror stories have also started to come through. These have included questionable practices on the part of end borrowers. Local media is full of reports of financial scandal and skullduggery: tales of Wenzhou entrepreneurs disappearing into thin air with recently acquired loans. This comes alongside evidence of the extent of the LGIV defaults. For example, the Liaoning province in northeast China is reported (in the Xinhua Press) to have 156 out of its 184 LGIVs already in default due to lack of cash flow

Estimating an 80% loss rate, we predict a potential black hole in the banking system equivalent to 25% of GDP. Scary numbers but, fortunately, China can afford it given its low starting government-debt-to-GDP levels, and the fact that losses are likely to be spread over many years – through a process of forbearance and denial!

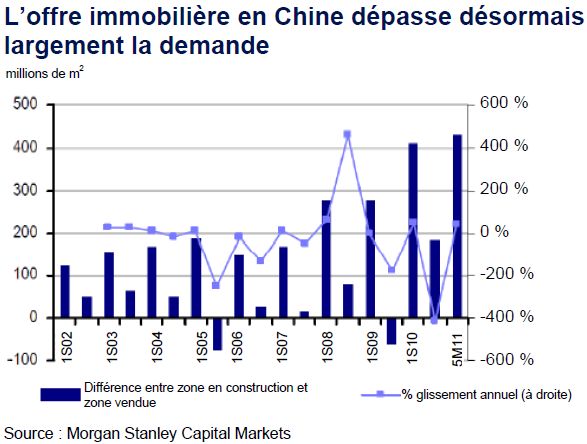

However, even as the first property companies begin to go bust, the outlook isn’t all bad. The Chinese authorities appear to have woken up to the problem and the country’s markets fell 30% in the third quarter of this year. In our view, this is positive, and signals that the market recognises the problem. As good a start as this may be, debts are pretty stubborn things, and we are braced for things to get a lot worse. Chinese property is particularly vulnerable at the moment, due to large-scale oversupply, extended affordability and rampant speculation (Chart 1 shows negative deposit rates and capital controls mean property is the main avenue of saving for the Chinese middle classes).

We are also very worried about corporate cash flow. It has been clear that monetary policy and credit creation in China was not tightening as claimed. Instead, what drove the price of credit in the underground markets up to sky high levels was the extraordinary demand for credit. This appears to have been the result of very high levels of corporate capital expenditure despite deteriorating cash flows.

It is evident that across all segments – government related (LGIVs), state-owned enterprises (one of the main lenders into the shadow-banking system), corporates (high gearing, weak cashflow), property (yuck!) – the country is facing significant debt problems. We think the situation could unravel fairly quickly over the next three to six months (as financial crises are apt to do). In particular, off-balance sheet lending is effectively a chain that, when broken, tends to trigger a cascade of defaults.

Having said this, there may be light at the end of the tunnel for China. The problems within the financial sector could prove the first stages of the dismantling of the old model of government-directed lending and loan quotas. We could start to see a move towards market-driven interest rates, the proper pricing and rationing of credit, and realistic rates for deposits. This would be a huge step forward in the rebalancing process that the market has been calling for for some time, and could help shift China away from a fixed-asset investment economy to a more consumer-orientated economy.

Either way, what happens next in China will be fascinating for observers, but nerve-racking for investors. Some “creative destruction” (kicking out the crooks and the favoured few) is likely to be the end result of this crisis. But progress isn’t inevitable. We could, instead, see a panic move back to the same old policies of 2008/09 (i.e. a bankdirected fixed asset investment program), which would be deeply damaging for the Chinese stockmarket, long term.

The next step for investors?

We think the noise surrounding China’s banks and the problems in the financial system have the potential over the coming months to give us a crisis-level buying opportunity in Asia. However, we don’t think the current problems, although serious, will lead either to a complete collapse in China’s growth rate or a full-blown financial crisis.

The event does, however, have serious implications for what you might want to buy in China and related sectors in Asia. We think fixed-asset investment has now peaked as a percentage of GDP, and will slow sharply or contract from now on. Soaring cement consumption gives us a good idea of just how crazy China’s investment bubble has been. No country has ever consumed cement at a faster rate per capita than China and, as seen in Spain, this number can come off sharply as the cycle turns. Given these concerns, we are avoiding all construction, property, material, infrastructure-related names in China and any companies across the region that are heavily exposed to this sector (Korean and Taiwanese industrials and cyclicals, as well as commodity names).

We also see little merit in trying to ‘bottom fish’ in Chinese property names. Balance sheets across the board in this sector are very weak and accounting practices in many companies are questionable. The sector has always been opaque and we think it is best to follow the clever money here. We were recently told by one of Hong Kong’s largest and best-connected conglomerates that it has no interest in acquiring bankrupt Chinese property companies (or buying their land directly) as titles and practices are questionable, and the real value of assets remains impossible to verify.

As the crisis unfolds we are likely to see some attractive opportunities to bolster our stance in China. On the back of recent weakness, we have already begun nibbling on a few quality names that were bombed out by the Q3 sell off. In particular, we are interested in the strongest consumer and internet names, however, we still think it is too early and valuations are too high. Although cautious on China overall, we are still building positions in transparent companies with solid business franchises, strong managements and a good track record because, despite the problems on the horizon, China’s long-term growth story hasn’t gone away.

Robin Parbrook , November 2011

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |