| https://www.next-finance.net/en | |

|

Strategy

|

Negative real rates likely to be a lasting feature in the Eurozone

According to René Defossez, Strategist at Natixis, it seems reasonable to assume that, to begin with, the European Central Bank will endeavour to keep the 10-year nominal swap as low as possible, which means that the breakeven swap will remain deep in negative territory. However, it is also likely that the breakeven swap will remain very volatile, maybe more so, given the change in the global environment...

Article also available in :

English ![]() |

français

|

français ![]()

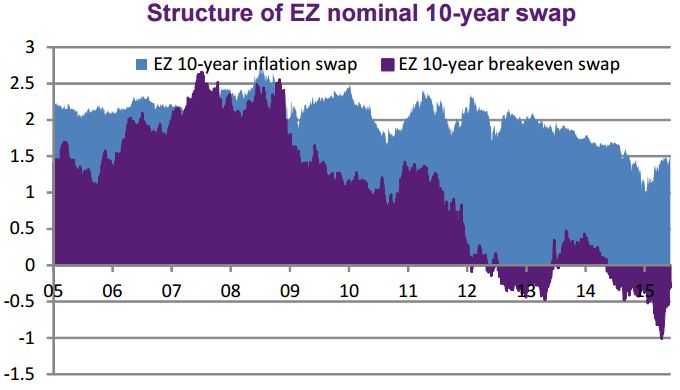

To anticipate the future behaviour of the Eurozone 10-year swap rate, it may be useful to consider separately its two components, namely the breakeven swap (in fact the real rate) and the inflation swap.

Pre-crisis, as highlighted in the chart above, the inflation swap hovered between 2% and 2.5% on the view that the European Central Bank anti-inflation credibility was rock solid. The crisis led to much greater volatility to begin with, but it was not until 2013, when the deflation risk started to loom high, that the inflation swap subsided sharply. However, prospects that the ECB would resort to quantitative easing and then the launch of the PSPP did enable the inflation swap to pick up slightly later on.

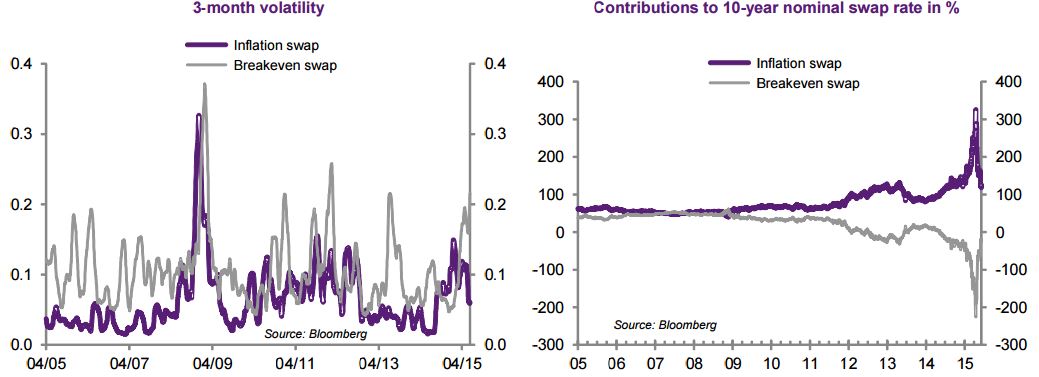

The real component of the nominal swap (i.e. the breakeven swap) displayed far greater volatility over the period than the inflation premium (standard deviations of 0.92 and 0.3, respectively, over the period). Even when standard deviations are calculated over shorter period (3 months in the chart below), the breakeven swap nearly always displayed greater volatility than the inflation swap.

Pre-crisis, the breakeven swap hovered between 1.5% and 2.5%. It collapsed immediately after the onset of the crisis and, especially, sunk into negative territory from 2013 onwards, where it remains to this day.

When contributions are expressed in percentage terms, this reveals that, pre-crisis, the breakeven swap and inflation swap contributed just about equally to the formation of the nominal swap rate (see right-hand chart above). In the wake of the crisis, however, the contribution by the breakeven swap tended toward zero percent, then became significantly less than zero percent, given that real rates moved into negative territory.

The current situation is therefore far removed from normality such as it was pre-crisis (fifty-fifty contributions by the

inflation premium and real rate). This raises a number of questions:

1. Will there be a return to the normality of old?

2. Will the inflation swap and breakeven swap end up once again making 50% contributions, i.e. 200bp each?

3. How long will this normalisation take?

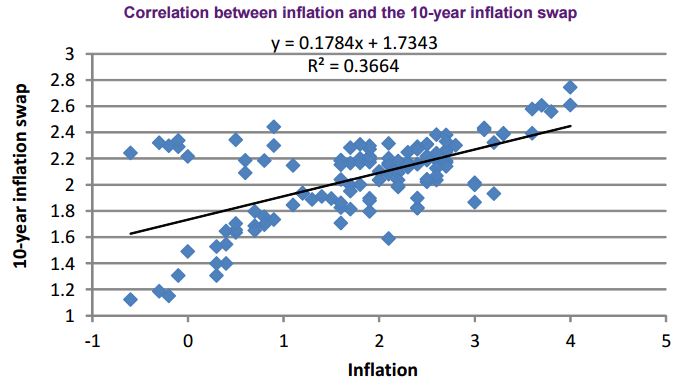

The inflation swap could continue to rise, but rather more on account of the evolution in crude oil prices (over which the ECB has no say) than monetary policy measures. Come the end of the year, assuming crude oil prices stabilise, Eurozone inflation could reach around 1.5%. Based on the correlation between inflation and the inflation swap since 2005, this suggests that the 10-year inflation swap could reach 2%, up 60bp from current levels, and nearer its average level pre-crisis.

If the breakeven swap is stable over this same period, this signifies that the 10-year nominal swap could clamber by a further 60bp or so by the year-end, back to around 1.80%. It seems reasonable to assume that, to begin with, the European Central Bank will endeavour to keep the 10-year nominal swap as low as possible, which means that the breakeven swap will remain deep in negative territory. However, it is also likely that the breakeven swap will remain very volatile, maybe more so, given the change in the global environment (the Federal Reserve being likely to raise its rates before the end of the year) and anticipations that there will be an early tapering of asset purchases by the European Central Bank, which the latter will struggle to dispel.

René Defossez , June 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |