Merger Arbitrage Expected to Continue Its Climb in Q4

As the third quarter came to an end, it is time to take some perspective. The summer lull fuelled risk assets after a turbulent first half (MSCI World +4.5% in Q3) and hedge funds benefitted from it. Strategies with higher betas outperformed, such as L/S Equity and Event-Driven...

Article also available in :

English ![]() |

français

|

français ![]()

As the third quarter came to an end, it is time to take some perspective. The summer lull fuelled risk assets after a turbulent first half (MSCI World +4.5% in Q3) and hedge funds benefitted from it. Strategies with higher betas outperformed, such as L/S Equity and Event-Driven, while “long volatility” strategies underperformed, such as CTAs and Global Macro. In September, the same trends were at work, though global equities were flat.

Heading into Q4, we believe that market conditions are likely to be less supportive than in Q3. Key political milestones (US elections, Italian referendum), renewed question marks about European banks and the likelihood that the Fed will tighten in December may fuel market uncertainty. This comes on top of rich valuations across the board.

On the back of our cautious stance on risk assets, we have turned more defensive on L/S Equity strategies (downgraded to slight underweight). Our preference goes to managers with low net exposure and rather positioned on quality/low beta stocks. We maintain, nonetheless, Market Neutral Long/Short at slight overweight, as the strategy is usually protective when implied volatility rises.

With regards to Event-Driven, we have Special Situations funds at slight underweight. The strategy has an elevated beta vs. the MSCI World (38%) and is, thus, sensitive to market downturns. It is also exposed to political risk, which has increased for the health care sector in the US as candidates for the US presidency have expressed their willingness to control drug prices. The industry has long been an important sector for Event Driven managers.

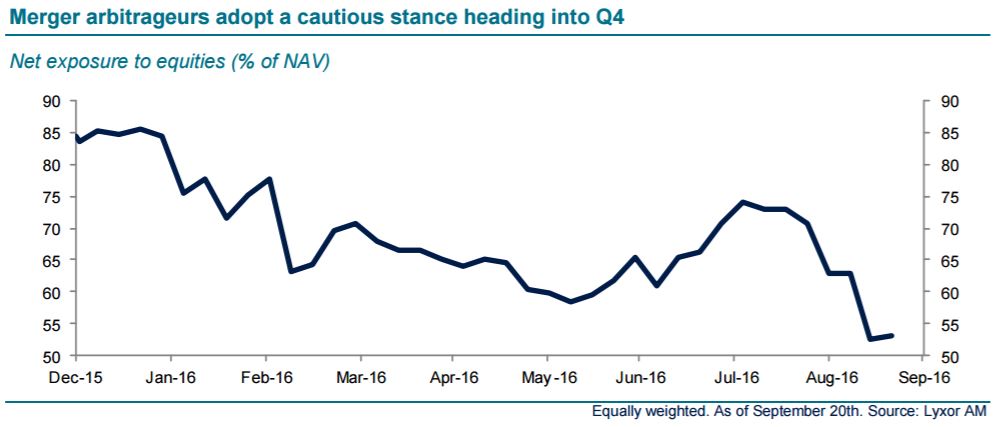

Finally, we reaffirm our stance on merger arbitrage at slight overweight. The strategy has benefitted in September from the completion of several high profile deals in portfolios (EMC Corp. vs. Dell, ARM Holdings vs. Softbank, Medivation vs. Pfizer) and has increased its cash cushion. Net exposure to equities has decreased to 2016 lows (see chart) as managers look for opportunities to deploy capital.

With M&A activity running at full steam in Q3 (volumes reached USD 978bn in Q3 according to Bloomberg), we believe that the opportunity set is large while the risks are manageable (the beta vs the MSCI World is 5%).

Lyxor Research , October 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |