Long Short Credit resilience defies investors’concerns

Since early December, Merger Arbitrage and L/S Equity Market Neutral has outperformed, while L/S Equity remains under pressure. Relative Value Arbitrage was resilient. Based on a peer group of 28 onshore L/S Credit strategies, the median performance was -0.3% month-to-date (up until December 12th) and -1.3% quarter-to-date.

Article also available in :

English ![]() |

français

|

français ![]()

Risk aversion continues to prevail so far in Q4, despite lower equity valuations and wider credit spreads. Expectations of a year-end rally in risk assets have faded, as concerns over Brexit remain acute and the probability of a recession in the U.S. keeps rising, albeit at a low level. The growth divergence between the U.S. and Europe has further widened in Q4, pushing the U.S. Dollar index to record highs this year in a context of multiple headwinds, according to the ECB at its latest monetary policy meeting.

These market conditions continue to favor low beta hedge fund strategies. Since early December, Merger Arbitrage and L/S Equity Market Neutral has outperformed, while L/S Equity remains under pressure. Relative Value Arbitrage was resilient. Based on a peer group of 28 onshore L/S Credit strategies, the median performance was -0.3% month-to-date (up until December 12th) and -1.3% quarter-to-date. Yet, liquidity concerns have investors in L/S Credit strategies in defensive mode.

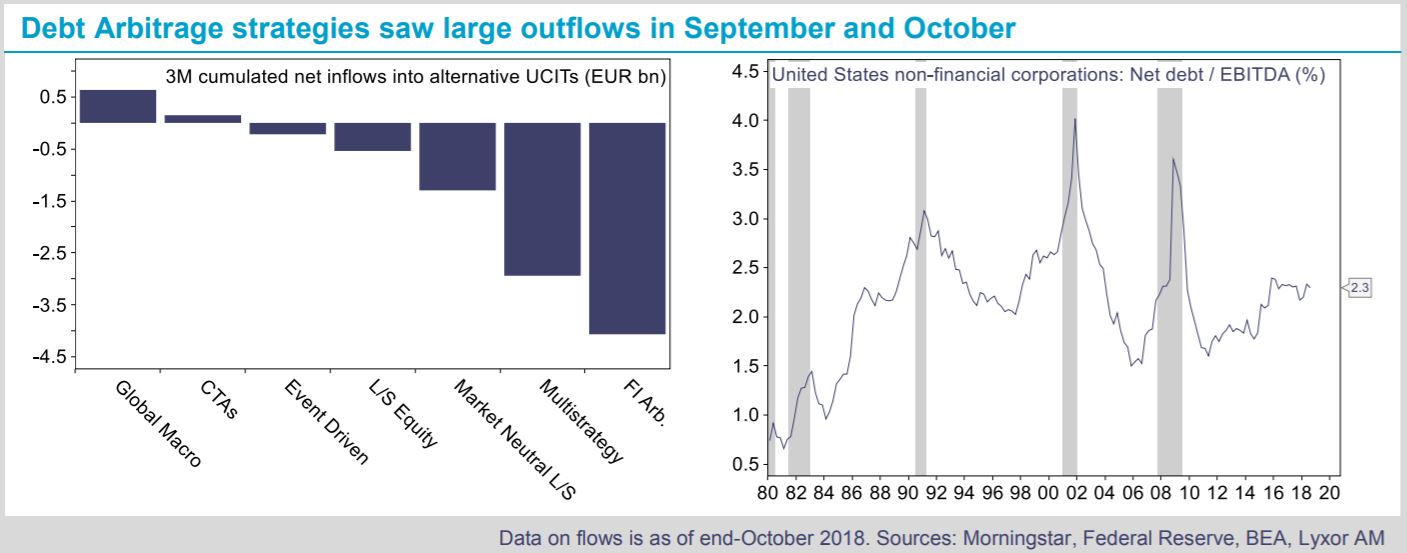

According to Morningstar data, onshore Fixed Income strategies experienced large outflows in September and October.

Going forward, we note that U.S. corporate leverage has stabilized since 2015 at levels that prevailed in the run-up to the Global Financial Crisis. High-yield default rates forecasted by rating agencies in twelve months remain nonetheless benign for Europe and the U.S. These are expected to remain below 2.5% against an average of 2.7% and 3.4%, respectively, over the past five years. Yet, liquidity tensions could flare up rapidly in current market conditions and cause wide fluctuations in asset prices. We ourselves are bearish on credit. We expect wider spreads across regions due to softer macro data, the end of Quantitative Easing in the euro area and asset reallocation out of credit in favor of Treasuries. Investors are thus probably right to be concerned. Yet, L/S Credit managers are defensive in their positioning as illustrated by resilience in Q4.

In our view, the above supports a Neutral stance on L/S Credit strategies and a preference for strategies with lower market directionality. Such strategies could take advantage of higher dispersion in credit markets and generate performance from their short books.

Lyxor Research , December 2018

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |