| https://www.next-finance.net/en | |

|

Strategy

|

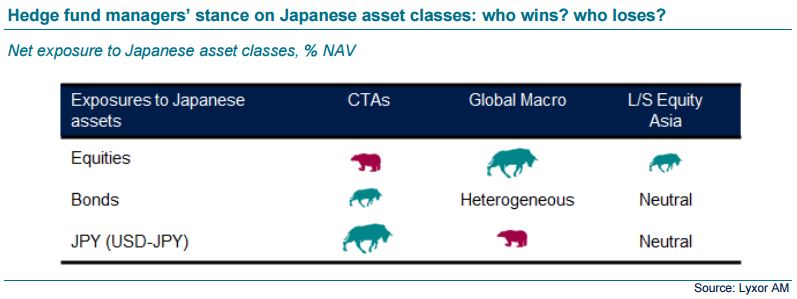

JPY at risk of reversal: who wins? who loses?

JPY and Japanese equities were the outcast of the rally, in diffidence of Abenomics’ and BoJ’s chances of success. They bear a risk of a reversal ahead of the coming BoJ meetings (April 28 & June 16) and the July Upper House election.

Risky assets kept on heading north. Chinese data are evidencing that the monetary and fiscal stimuli are passing through in the real economy. The EPS season is starting better than feared. Moreover, the (dovish) Fed is keeping pressure on the dollar, while capping any higher yields attempts. All of these were good ingredients for greater risk appetite, or rather, for lesser risk aversion.

Indeed, subdued trading volumes in most regions emphasized a continued reluctance to join in the rally, as has been the case since mid-February. Investors remain confused, sorting out whether they gave in to unjustified fears in January, or whether they avoided a vicious circle, courtesy of central banks, weaker USD, and recovering oil prices.

Forced in the rally, investors remained on the cautious side, which could give ammunitions for further market inflows. However, unlocking them will likely require more fundamental evidence, in particular regarding: the Fed’s timeline that is central for many assets, the sustainability of the pick-up in Chinese activity, the US consumers and EPS resilience, the credit impulse in Europe, and prospect for further BoJ easing.

JPY and Japanese equities were the outcast of the rally, in diffidence of Abenomics’ and BoJ’s chances of success. They bear a risk of a reversal ahead of the coming BoJ meetings (April 28 & June 16) and the July Upper House election.

Hedge funds continued to progress last week. The longest bias strategies captured the bulk of the gains: the long bias L/S Equity and Special Situation funds outperformed. The Merger Arbitrage funds continued to display limited contagion from the recent inversion stress. Global Macro funds benefitted from their long equity exposures.

CTAs recorded mild losses on bonds, partially offset by gains in equities. The violent short covering in financials and resources sectors unsettled the market neutral funds, as well as some variable funds.

Lyxor Research , April 2016

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |