| https://www.next-finance.net/en | |

|

Strategy

|

Investors are not complacent in assessing risks

Markets have been remarkably resilient to political shocks, so are investors getting complacent? No, says Jaap Hoek in Robeco’s new five-year outlook.

Article also available in :

English ![]() |

français

|

français ![]()

In fact, he believes both the market and commentators have been “quite on the ball” when it comes to correctly assessing and assimilating risks, though relying on traditional models does not always paint the full picture.

He says risk periods in financial markets tend to move in clusters, where one relatively calm period is often followed by another. Conversely, a highly volatile period like the global financial crisis does not just last for a couple of days: risk remains at elevated levels for a while, before returning to normal.

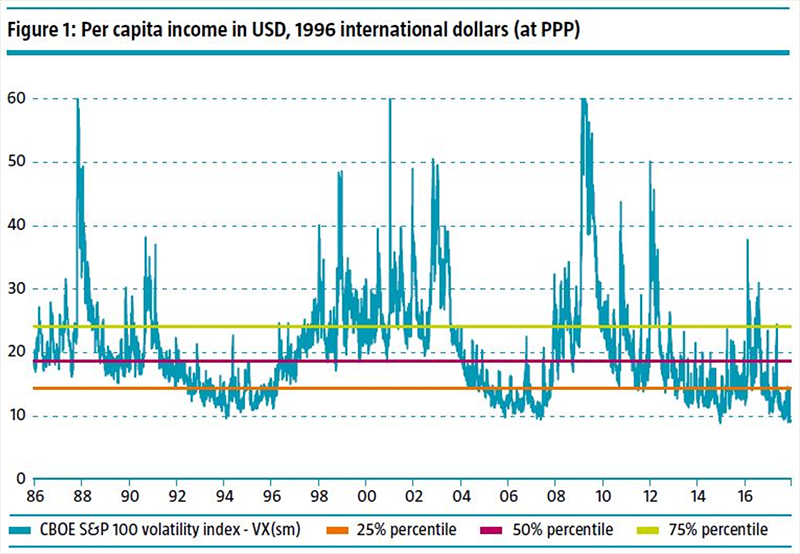

This can be seen in movements in the VXO Index, the predecessor of the well-known VIX Index for volatility, where it is easy to spot the 1987 stock market crash, the 2000 dotcom bubble and the 2008 financial crisis in the chart below. Recent political shocks such as Brexit and Trump in 2016 have been relatively minor by comparison

Risk prediction models

To predict likely future risk, investors can use the Autoregressive Conditional Heteroscedasticity (ARCH) model, where risk is assessed by looking at previous (autoregressive) deviations from the norm. “Of course, the past is not the only factor, since volatility will also change due to information that has become recently available,” says Hoek, a portfolio strategist with Robeco Investment Solutions.

“If we use the model to capture today’s market, it shows that volatility has remained in line with the previous low readings, and that there has been no new information that was sufficiently serious enough to derail it. Brexit and Trump only led to temporary shocks that soon faded out, and markets quickly reverted to their underlying trend.”

“Other models found that ‘in general, historical volatility computed over many past periods provides the most accurate forecasts’. So we don’t need a complex model to make predictions, especially for longer periods like the coming five years: a mod-el using historical volatilities over different periods will be sufficient.”

History on their side

How then to make predictions such as those contained in Expected Returns 2018-2022? “Looking at all the historical lessons, it would be most logical for the market to be expecting higher or more normal volatility than today’s low level, even over a shorter time period than five years,” says Hoek.

“So those commentators who predict a return of volatility have history on their side. But why then is the market so complacent? To answer this question, we must turn to the exceptional role central banks have played since the 2008 financial crisis.”

He says massive quantitative easing programs and historically low (and even negative) interest rates mean central banks have effectively put a floor under volatility. “It is no surprise then that markets expect risk to remain low as long as central banks retain this stance,” he says. “With this in mind, it seems as though the market has been more on the ball than those commentators who predicted a return of risk.”

SKEWing the figures

However, the picture changes if we look at another measure of risk, he says. Market traders use models such as Black-Scholes to assess volatility risk when pricing options. Here, the market often assigns higher probability to tail risks, which can be measured by the SKEW Index. If the SKEW increases, it generally means that more investors feel there is a greater risk that a disaster will occur.

“Over the last seven years, the market has had a higher level of SKEW than it did in the 1990s,” says Hoek. “This is in stark contrast to the downward trend in the VIX level over the same period. Even more surprising is the level of the SKEW in 2017, which is well above the average.”

Overall, it implies that central bank action has proved to be a powerful tool in reducing volatility, but the market does not believe that central banks can halt the next crisis. “In short, the market, commentators and regulators all agree that we would be wise to keep an eye on the tail risks,” Hoek concludes.

Jaap HoeK , November 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |