| https://www.next-finance.net/en | |

|

Opinion

|

Interest rates: Brexit and term premiums

Since the announcement of the vote for Brexit at the UK referendum, long-term interest rates have plunged to record lows across all major currencies. The US 10-year interest rate hit an all-time low of 1.32% on July 6, before rebounding to 1.47% on July 12. But are these levels sustainable?

Article also available in :

English ![]() |

français

|

français ![]()

Since the announcement of the vote for Brexit at the UK referendum, long-term interest rates have plunged to record lows across all major currencies. The US 10-year interest rate hit an all-time low of 1.32% on July 6, before rebounding to 1.47% on July 12. But are these levels sustainable?

It is instructive to analyze long-term interest rates movements by breaking them down to identify three factors: expected real short-term interest rate, inflation expectations and the term premium.

A long-term bond can be arbitraged for a short-term deposit that is rolled over for the bond’s entire maturity, so the nominal long-term interest rate can be analyzed as the expected short-term interest rate discounted over the long term. Accordingly, the 10-year interest rate appears as the average value of the expected overnight interest rate over the next 10 years, plus a risk premium that takes into account the fact that the capital invested in the case of a long-term bond can be released onto the market before maturity only at the cost of a potential discount – the price of the long-term bond in the secondary market is subject to interest rate risk. On the bond market, this risk premium is known as the term premium. This average expected short-term interest rate can itself be broken down into a real short-term interest rate and projected future inflation, according to Fisher’s equation. These three factors, expected real short-term interest rate, inflation expectations and the term premium, are presented in the chart below for the US 10-year interest rate. We use the calculations of economists Kim and Wright, as published by the US Federal Reserve, for the term premium and the expected nominal short-term interest rate. The calculation of the term premium is derived from a modelling process that extracts the information on expectations of future short-term interest rates across the entire yield curve.

Breakdown of US long-term interest rates

This breakdown indicates that the fall in long-term interest rates can primarily be attributed to the drop in the expected real short-term interest rate and in the term premium, while 10-year expected inflation, which is approximated by the 10-year inflation swap in this case, remains virtually stable.

The market is actually pricing in a scenario whereby a normalization of the Fed’s interest rates is impossible, even in the long term. The expected average real shortterm interest rate has fallen to 0.36%. By way of comparison, the Fed’s median scenario ("Summary of Economic projections" of June 15) expects a long-term equilibrium value of the Fed Funds rate at 3%. If we take into account its medium-term inflation target of 2%, this is therefore equivalent to a real short-term interest rate of 1%. Admittedly, the interest rate that the Fed expects has fallen markedly since these projections started in 2012, but it still remains well above the figure that the market now expects. The market is therefore showing the Fed that it is set to fail in its efforts: investors expect that monetary policy normalization will turn out to be impossible.

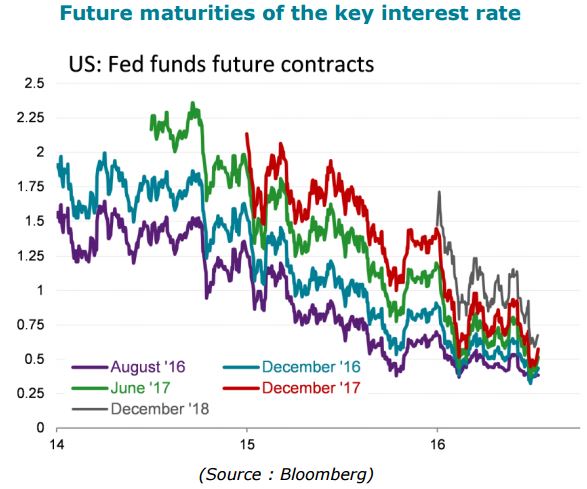

Future maturities of the key interest rate

According to our estimates, the term premium stands at -0.6%. As shown by the chart below, this term premium is not yet at its historical low, which was reached during the Fed’s quantitative easing programs in 2012. However, our term premium modelling approach indicates that this extremely negative figure is justified by several factors: the degree of political uncertainty, as measured by the Baker, Bloom & Davis indicator; the flight to quality, as assessed by the valuation of other safe havens such as the Swiss franc and precious metals; the level of excess dollar supply, as reflected by US banks’ excess reserves; and the pressure on the market for long-term financing in dollars (EUR/USD basis swaps).

US: 10 years term premium

Beyond the increase in the post-Brexit political uncertainty, this shock has prompted a slight downward revision of expectations for global growth, but the most salient point in our opinion is that it has revealed market complacency in its assessment of political risks. The obvious failure of political analysts, pollsters and online betting sites to accurately forecast the result of the UK referendum showed that the markets largely underestimated the cost of political uncertainty. This "repricing" should now affect all forthcoming election results, in Europe as well as in the United States.

Furthermore, we would also add another factor that is set to put downward pressure on the term premium, i.e. the increasingly negative impact of long-term interest rates in Europe (Germany, Switzerland, etc.) and in Japan. This trend is forcing domestic institutional investors to search for yield in markets that are still liquid and provide positive yields, such as the US Treasuries market. In this more uncertain post-Brexit world, capital that is fleeing risk will continue to find a safe haven in the liquidity of US bonds. We therefore continue to favor this market in our asset allocation to hedge our positions on global equities.

Raphaël Gallardo , July 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |