Hedge funds: The CTAs drift

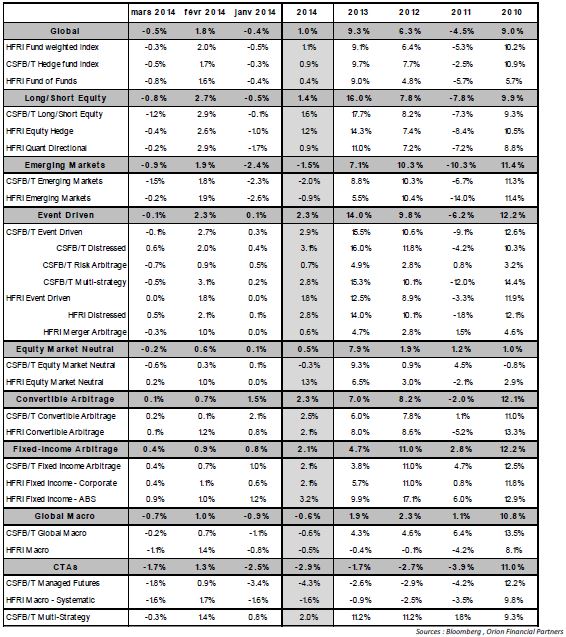

Since mid-2011, CTAs cumulative loss is between -10.6% (HFRI macro systematic index) and -16.8% (Credit Suisse Managed Futures Index). For the first quarter of this year, CTAs show a drawdown of about 3% which is expected to increase in April (-0.66% for HFRX CTA index) ...

Article also available in :

English ![]() |

français

|

français ![]()

Since mid-2011, CTAs cumulative loss is between -10.6% (HFRI macro systematic index) and -16.8% (Credit Suisse Managed Futures Index). For the first quarter of this year, CTAs show a drawdown of about 3% (tab 1) which is expected to increase in April (-0.66% for HFRX CTA index).

What are the reasons for that?

We usually decompose the performance of hedge funds in three components:

• beta, namely performance from passive exposure to systematic risk (market);

• alpha generated by stock picking and arbitrage;

• market timing, from the manager ability to anticipate major market trends.

Unlike arbitrage strategies, the CTA mandate is not necessarily to generate alpha, but to benefit from upward and downward trends (market timing) in major asset classes (equities, fixed income, currencies and commodities).

Chart 1 summarizes the results of a quantitative analysis regarding the HFRX Macro Systematic CTA index performance since May 2013 [1].

Firstly, we find that the average exposures to market risk (bêta) have generated a significant performance in 2013, but more since the beginning of the year. Moreover, alpha generated by fund managers is negative. This point is not problematic, as many academic studies show that systematically negative alpha is part of the genesis of CTAs performance [2]. These recurring losses could be seen as "opportunity costs" induced by successive positions when trends are not strong enough or when stop-losses are triggered on a short term basis (intraday). The acceleration of "opportunity costs" (losses due to alpha) since the beginning of the year, is worrying.

The second point is the fact that CTAs have, on average, not generated market timing over the same period of time.

How to explain the absence of market timing? From a theoretical point of view, the market timing takes advantage of the market momentum, ie the strength generated by recent price changes for investor expectations, regardless of fundamental changes.

This is a field of behavioral finance [3], describing endogenous market phenomena. For example, in the case of a bullish momentum, the price increase fuels investor demand, which in turn makes the price rise ... In the absence of exogenous shocks, such a spiral can lead to favorable trends for CTAs.

But today, unconventional monetary policies in the United States (Quantitative easing and Tappering) and more recently in Japan (Abenomics) have a significant impact on stock prices (highly reactive to liquidity injected by central banks), interest rates (direct impact on the yield curve, especially in the U.S market) and currencies (world currency war). If we add to that the impact of the economic slowdown in emerging countries on commodity prices and the drying up of the " rate vector", we understand that the current market environment significantly penalizes CTAs.

Guillaume Monarcha , July 2014

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] Analyse multifactorielle dynamique (filtre de Kalman) des performances de quotidiennes de l’indice.

[2] Fung et Hsieh [2001] assimilent par exemple l’alpha négatif des CTAs à une prime payée pour accéder à un payoff de type loockback straddle.

[3] Champ d’étude visant notamment à décrypter les comportements moutonniers, la création et l’éclatement des bulles spéculatives.

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |