Hedge Funds Hold their Nerves and Hedges ahead of the French Elections

The Lyxor Hedge Fund Index was marginally down last week. Lower oil prices and a weaker dollar contributed to the underperformance of Macro funds. However, they limited damages after building-up substantial long EM FX positions prior to the FOMC (as a result, their net overall USD exposure dropped by a third)...

Article also available in :

English ![]() |

français

|

français ![]()

Markets were well prepared by the Fed for a March hike. U.S. treasury yields were up 10bps before giving back all of their gains after the FOMC. There were limited alterations to the Fed’s economic projections and the median dot still projected three hikes for 2017, which Yellen qualified as “gradual.” Along with rates, the dollar weakened offering a sweet spot for most risk assets. Equities progressed as well as metals, EM assets, and commodity FX.

Oil was the odd man out. Prices reverted back to the lower bound of their trading range. Doubts regarding the timing of the market rebalancing resumed amid persisting excess stock and increasing U.S. production.

The Lyxor Hedge Fund Index was marginally down last week. Lower oil prices and a weaker dollar contributed to the underperformance of Macro funds. However, they limited damages after building-up substantial long EM FX positions prior to the FOMC (as a result, their net overall USD exposure dropped by a third). Merger funds also lagged last week due to non-M&A energy positions. Additionally, Credit funds’ returns eroded on wider energy spreads.

Alternatively, the strategies most exposed to risk assets benefitted from encouraging global growth and hope from Trump’s reflation coupled with limited U.S. rates and dollar headwinds for now. A large majority of L/S Equity funds were up, led by those focusing on EM markets. CTAs’ aggressive exposure on equities also paid off.

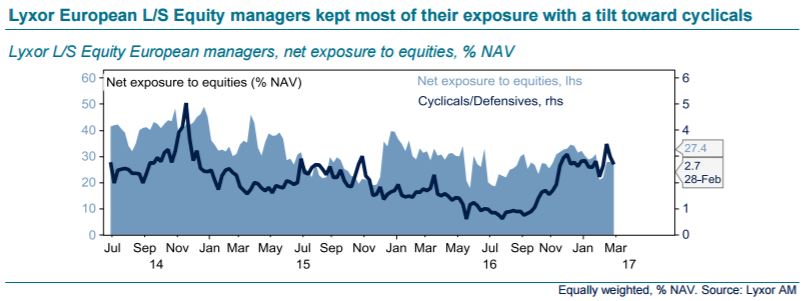

The success of the moderates in the Netherlands only had a marginal impact on the Eurozone risk premium. Spreads in French, Italian and periphery govies barely changed, just like banks’ credit spreads. Hedge fund managers are not expecting a disruptive change in the French political chessboard (and hence in Europe).

They are keeping most of their long exposures. Meanwhile, they maintain hedges through lower exposure to financials, index shorts, Euro shorts, and/or a relative preference for Northern European assets. In other words, while keeping tail-risk protection, most managers remain positioned for a valuation catch-up once the French (and Italian) political uncertainty has faded.

Lyxor Research , March 2017

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |