| https://www.next-finance.net/en | |

|

Strategy

|

Fixed Income : The Risk of Safety

The near-record lows now prevailing for sovereign bond yields reflect persistent anxiety about the outlook for growth around the world. Yet the global economy continues to expand — and inflation remains muted in the world’s largest economies. As a result, U.S. Treasuries — widely viewed as the ultimate safe haven — could entail greater embedded risks than many realize...

- That’s because even a modest pick-up in growth and inflation could arguably push sovereign yields higher — and prices lower. And that would have notable ripple effects in portfolios heavily weighted toward sovereign bonds — in particular the many passive strategies tied to the Barclays U.S. Aggregate Bond Index. [1]

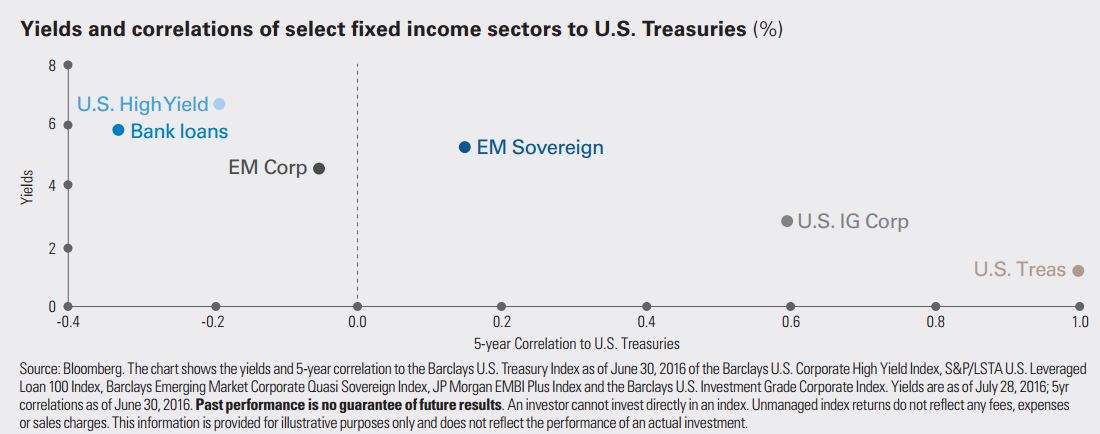

- But by the same token, higher-yielding sectors that have a low correlation to Treasuries could have the potential for further gains if and when growth picks up, and with it, investor confidence. That includes not only investmentgrade credit and emerging markets sovereign debt, but also sectors with a negative correlation to Treasuries, i.e. that have historically moved up when Treasuries move down, including emerging market corporate debt, U.S. high yield and bank loans.

- To be sure, data on the U.S. economy has yet to suggest a huge acceleration in growth. But everything’s relative — and the question is whether there might be enough to be inconsistent with the level of pessimism still priced into Treasuries.

- Consider that core inflation in the U.S. has crept higher to 2.3% [2], matching the highest level in four years — something that a data dependent Federal Reserve will certainly be paying close attention to as it debates the pace of interest rate normalization.

- All this underscores why it could make sense today to look beyond traditional bond benchmarks and their heavy tilt toward Treasuries — to more diversified active strategies, including unconstrained strategies with the flexibility to incorporate higher-yielding sectors of the bond market.

Legg Mason , September 2016

Footnotes

[1] Note: The Barclays U.S. Aggregate Bond Index focuses on large, liquid, fixed-rate investment-grade issues, which have had historically low yields and longer-than-average duration in recent years. That means less income to offset the future impact of rising interest rates (interest rate risk) on bond prices. Treasuries and mortgage-backed securities represent a bigger share of index than before 2008 crisis. The index excludes approximately 65% of the investable fixed-income universe including inflation-linked, below-investment-grade, floating-rate and non-U.S. securities.

[2] 2 Bloomberg, June 2016

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |