European ETF Market flows increased in November 2016.

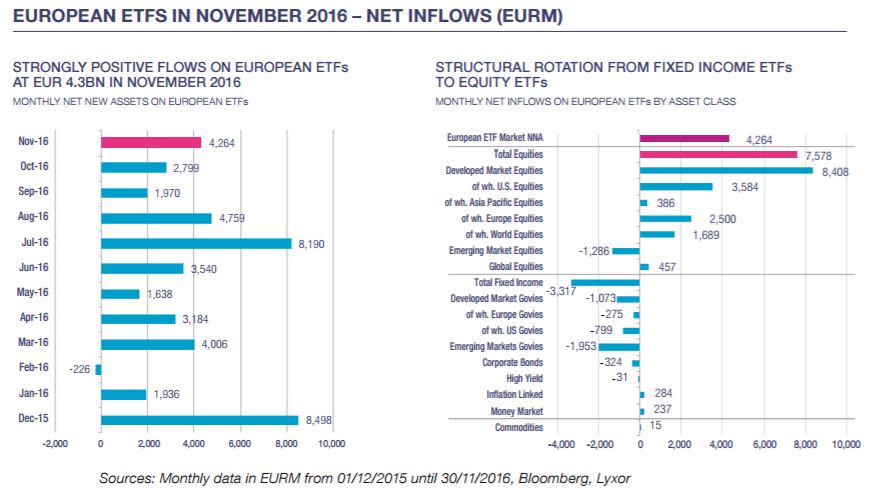

Net New Assets (NNA) during this month amounted to EUR4.3bn, above the year to date average of EUR3.7bn. Total Assets under Management are up 10% vs. the end of 2015, reaching EUR497bn, and including a limited market impact (+2.2%).

Article also available in :

English ![]() |

français

|

français ![]()

Net New Assets (NNA) during this month amounted to EUR4.3bn, above the year to date average of EUR3.7bn. Total Assets under Management are up 10% vs. the end of 2015, reaching EUR497bn, and including a limited market impact (+2.2%). ETF flows experienced a great rotation from fixed income to equities and from emerging to developed equities. The pick up in developed equities was mainly focused on US and European underlyings, following Trump’s election.

- Equity ETFs saw 11-month record high inflows at EUR7.6bn. US equity ETF flows

accelerated at EUR3.6bn, mainly during the days following the US election. European ETFs

saw a significant trend reversal at EUR 2.5bn, though they still haven’t made up forthe huge

outflows observed earlier in the year. Global developed equities also benefited from increased

investor confidence with EUR1.7bn of inflows. The confirmation from the Fed of the next interest rate

increase triggered some outflows from emerging markets at EUR1.3bn, mainly on broad and Asian

ETFs.

Within Smart Beta, the value style continued to see high interest with EUR621M of inflows together with some flows on the low vol factor, while Minimum Volatility ETFs continued to see outflows in this more risk-on environment.

Overall, Smart Beta flows reached EUR614M this month.

- Fixed income flows saw a trend reversal with outflows of EUR3.3bn following 16 months

of inflows. These outflows mainly concerned government bonds from both developed and emerging

countries at -EUR1.3bn and -EUR1.9bn respectively, having been negatively impacted by changes in

interest rate expectations following the US election.

Flows on investment grade corporate bonds also saw a halt with EUR319M of outflows following 9 months of positive flows, and a one year average of EUR1.2bn, likely reflecting investor doubts on a QE extension.

On the other hand, due to increased inflation fears in the market after the US election, inflation-linked ETFs continued to see inflows at EUR284M, mainly on US TIPS. Inverse strategy ETFs which benefit from interest rate increases (double short bund or UST) also saw significant interest with inflows of EUR248M, a one year record high as both US and European interest rates rebounded on expectations of a rate hike by the Fed and a change in US fiscal policy.

- Commodities ETFs [1] saw virtually no flows in November, but year to date flows are positive at EUR2.5bn.

Lyxor Research , December 2016

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] including also non UCITS eligible/compliant ETFs

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |