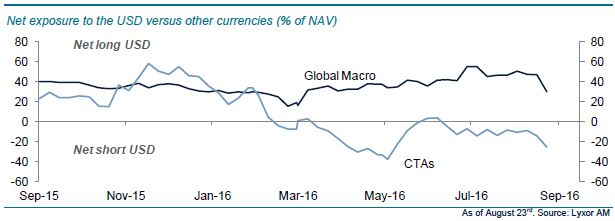

Dollar upswing lifts Global Macro managers

Market movements related to the new Fed guidance had a differentiated impact on hedge fund strategies. CTAs underperformed last week as a result of their long fixed income and short USD positions. Meanwhile, Global Macro managers outperformed.

Article also available in :

English ![]() |

français

|

français ![]()

Over the recent weeks, the Federal Reserve has signaled its willingness to move ahead with a second rate hike. Such a move would follow the December 2015 decision to raise policy rates. Statements from Yellen and Fisher left opened the possibility of a rate hike as soon as September 21st, when the FOMC will meet next. However, the decision is not straightforward considering the disappointing US GDP growth figures in H1-16 and the associated falling labor productivity. Financial markets remain somewhat unconvinced but at the same time they cannot ignore the Fed guidance. As a result, short dated Treasury yields moved higher and the USD appreciated against major currencies.

Market movements related to the new Fed guidance had a differentiated impact on hedge fund strategies. CTAs underperformed last week as a result of their long fixed income and short USD positions. Meanwhile, Global Macro managers outperformed. They benefitted from their long USD positions, a stance they have maintained for some time on the back of the growth divergence thesis between the US and the rest of the world.

Interestingly, most funds within each strategy share the same stance on the USD (i.e. most CTAs in our sample are short USD and most Global Macro are long USD). But there is a much wider disagreement across Global Macro managers on US fixed income. The aggregate exposure of Macro managers on the asset class is close to zero, but at the fund level we see approximately half of the managers being long US bonds and another half being short. That reflects the conflicting signals on the US economy. A vibrant job market has fuelled household consumption but this is not reflected in GDP numbers. Economic expansion was actually pulled back in H1-16 by declining capex as companies are not investing to expand production capacities.

All in all, we tend to be rather in favor of the CTA stance. We believe that the Fed is unlikely to move as soon as September. There are simply too many uncertainties regarding the strength of the US economy to act now. The Fed will probably err on the side of caution in our view and the USD upward pressure may abate, a support for CTAs over Macro funds.

Contrasted views on the US Dollar between Global Macro and CTAs

Lyxor Research , September 2016

Article also available in :

English ![]() |

français

|

français ![]()

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |