| https://www.next-finance.net/en | |

|

Strategy

|

Bank of Japan: stupor or fear?

Since the 2008 crisis, central banks have had a major influence on financial market trends. The Bank of Japan (BoJ) in particular has orchestrated a historic rally among Japanese equity markets since announcing its quantitative and qualitative easing strategy (QQE) at the end of 2012.

Article also available in :

English ![]() |

français

|

français ![]()

Since the 2008 crisis, central banks have had a major influence on financial market trends. The Bank of Japan (BoJ) in particular has orchestrated a historic rally among Japanese equity markets since announcing its quantitative and qualitative easing strategy (QQE) at the end of 2012. The implementation of an asset repurchase program reflected the willingness of the government led by Shinzo Abe to defeat deflation, which had prevailed since 1998. After its initial rapid success, this policy reached its limits however, as inflation forecasts stagnated below the 2% target set by the central bank. The BoJ nevertheless kept its monetary policy unchanged at the meeting held on October 30th, which surprised investors. The BoJ’s audacious strategy is now at a technical and political crossroads. The various constraints facing the BoJ provide a clear lesson for the future of unconventional monetary policies in Europe (eurozone, UK, Denmark, Sweden) and the US.

At its monetary policy meeting at the end of October, the Bank of Japan surprised the markets by opting to maintain the status quo. The Japanese economic climate is highly uncertain, although there are clear signs of a slowdown. Household consumer spending is still struggling to overcome the hike in TVA implemented during the spring of 2014, while exports have been hit by the crash in Chinese industrial investment. Corporate confidence has also been undermined by the absence of a snapback in consumer demand. Meanwhile, the leading export market, China, is undergoing an adjustment. Capex is predicted to remain flat this year according to the closely-watched Tankan survey. So how can the Bank of Japan’s cautious stance be justified?

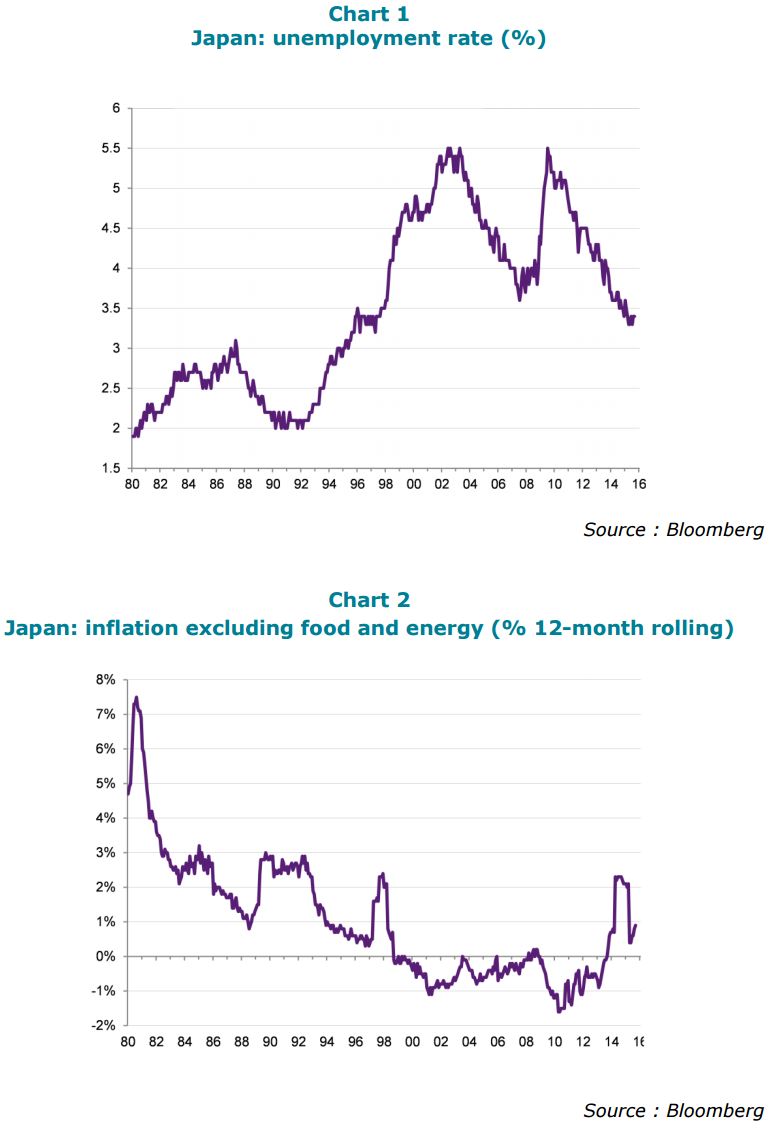

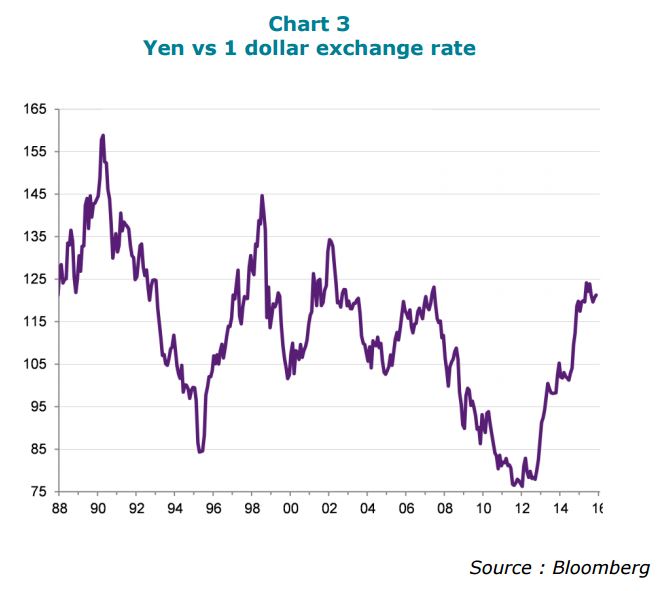

The proximity of other dynamic Asian economies tends to eclipse the fact that an ageing Japan harbors potential annual growth of only 0.3%. The economy does not require spectacular growth in order to approach full capacity utilization, which has been triggered by a series of budgetary stimulus packages initiated by Shinzo Abe since returning to power in 2012. The unemployment rate is at an 18-year low of only 3.4% (chart 1). Core inflation, excluding energy and food, rallied from -1% at the end of 2012 to 0.9% in September, on a rolling 12-month basis (chart 2). In this context, it is understandable that the BoJ considers that the risks incurred by extending its QQE program outweigh the benefits.

Firstly, QQE feeds through to inflation forecasts primarily thanks to weakness in the yen (chart 3). However, the government has faced the bitter experience of collateral damage inflicted by a weak yen. Weakening the currency exchange rate, in an economy which is a heavy importer of commodities (food, energy and industrial input), is equivalent to a hike in consumer VAT and levying an import duty on SMEs. Furthermore, the depreciation of the yen enrichens households which own large equity portfolios, by boosting revenues among major listed exporting companies. The devaluation amplifies wealth inequalities, acting like a negative capital tax. In order to preserve his political capital ahead of the forthcoming senatorial elections (summer 2016), the Prime Minister probably encouraged the BoJ to hold fire this time. Furthermore, with the signature of the TPP currently pending approval by the US Congress, it would be inappropriate for Japan to appear to be involved in a currency war.

Secondly, the BoJ is already buying-up considerable quantities of Japanese government bond securities (JGB) and absorbing 10% of public debt per year. At this rate, the IMF estimates that within one or two years, under certain hypotheses of domestic institutional investors holding JGBs as collateral, or as liquidity or to satisfy regulatory requirements, the BoJ will run out of government bonds to buy. Thus any acceleration in government bond repurchases will exacerbate fears of the program being suddenly halted, once the central bank runs out of purchasable securities. Anticipated fears of this type of withdrawal syndrome could weigh on the economy.

Furthermore, stepping-up the QQE program incurs the risk of overheating the Japanese economy, which is almost at full-employment, if global trade also accelerates. Japan may be at the inflexion point of the Phillips curve, which gauges unemployment vs wage inflation. At the inflexion point, any further fall in unemployment incurs the risk of triggering a steep rise in wages. Higher short-term inflation forecasts would lead to capital outflow among domestic investors seeking shelter against further cuts in real interest rates. This factor would then cause a further depreciation of the yen, which would vindicate the higher inflation forecasts and steepen long-term rates, which could jeopardize the government’s solvency. The BoJ would certainly attempt to calm any tensions in the bond market by stepping in as buyer of last resort, armed with unlimited liquidity. However, in the event of a massive bond market sell-off by domestic institutional investors (banks, pension funds and life-insurers looking to benefit from higher yields in foreign bond markets, while hedging against future yen weakness), the BoJ would be forced to buy enormous quantities of JGBs in the market in order to cap rising interest rates, given that public debt exceeds 200% of GDP. This would imply the creation of colossal liquidity by the central bank. The injection of fresh money into the system, which is already awash with monetary liquidity, would cause a surge in inflation expectations and therefore trigger further capital outflow, which would weigh even more heavily on the yen. The national currency would be caught up in a vicious negative spiral.

It is apparent that when devaluation is the only option remaining open to the central bank to stimulate inflation forecasts, target inflation policy becomes highly risky if public debt represents a significant multiple of the total monetary mass. This risk is even greater once the economy is approaching full employment, which represents a turning point at which wages can become a powerful driver behind an inflationary shock, triggered by lower exchange rates. The BoJ is therefore at a crossroads. Its program implemented to combat deflation was successful, as illustrated by the increase in core inflation towards 1%, but at the cost of currency depreciation, which weighed chiefly on consumers. The 2% target is still a long way off, whereas pursuing the program incurs increasing risks.

The government has now also refrained from putting pressure on the central bank to reach target inflation as quickly as possible. Shinzo Abe is aware of the political cost of the increase in inflation from -1 to +1% via the depreciation of the yen. With public debt yielding largely negative real interest rates and a rapid monetization of the BoJ’s debt reserves, pursuing the 2% inflation target may seem highly theoretical and would have no real political upside. Essentially, the Japanese government’s willingness to overcome modest domestic deflation, which in many ways constitutes a stable economic equilibrium, could be motivated primarily by the public debt situation, i.e. reversing the surge in public finances through monetary intervention, without engaging a long-winded parliamentary debate on budgetary policy. In this sense, it appears vital for the government to maintain the current pace of its QQE program, which ensures rapid monetization of the debt reserves and limited interest payments for the state, without the risk of a bond market crash, or undermining domestic political capital (Japanese electors) or exterior political capital (the US Congress approval of the TPP) through a hazardous depreciation of the yen.

We therefore believe, excluding a sudden downturn in the economic climate, that the BoJ is likely to maintain its current cautious monetary policy, reflecting the high risks incurred by any attempt to overstimulate an economy which is over-indebted, over-monetized and approaching full unemployment. The issues facing the BoJ could soon be shared by the Fed, the Bank of England and the Royal Bank of Sweden, as Japan in many ways represents a test-case for our unconventional monetary policies.

Raphaël Gallardo , November 2015

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |